Debt Management Program (DMP): What It Is, How It Works, and Key Considerations

A Debt Management Program (DMP) is a structured repayment plan established by a non-profit credit counseling agency to help individuals pay off unsecured debts, usually at lower interest rates and with a single monthly payment.

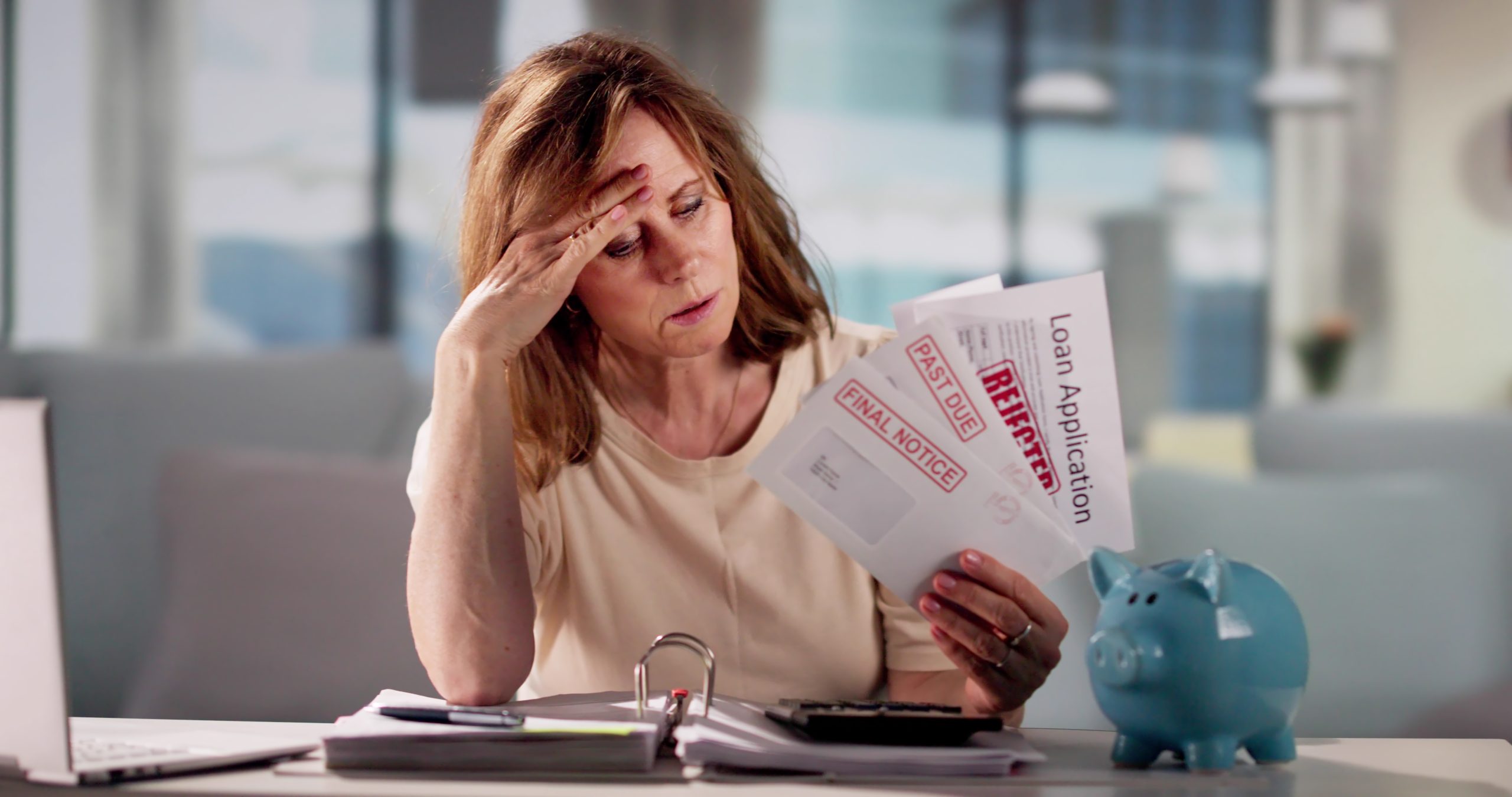

For many Americans, high-interest credit card debt creates a cycle where minimum payments barely cover finance charges, trapping them in long-term financial stress.

A DMP provides a disciplined, guided path toward debt freedom. Unlike debt settlement or bankruptcy, it focuses on repaying your debts in full under manageable, negotiated terms. This guide explains how DMPs work, what to expect, and whether this responsible financial strategy fits your goals.

Key Takeaways

A DMP is a repayment plan managed by a non-profit credit counseling agency that helps pay off unsecured debts in full at reduced interest rates. Counselors negotiate with creditors to lower rates and waive fees, consolidating multiple debts into one fixed monthly payment.

Programs typically last three to five years, and enrolled accounts are closed. While a DMP simplifies finances and saves money, it requires strict commitment and can temporarily affect your credit score. Choosing an accredited agency, such as one recognized by the NFCC or FCAA, is essential.

What Is a Debt Management Program (DMP)?

A DMP is a formal agreement between you, a licensed credit counseling agency, and your creditors. The agency negotiates lower interest rates and waived fees that individuals rarely obtain on their own.

This structure is especially effective for credit card debt, where rates often exceed twenty percent. By cutting those rates, often by more than half, repayment becomes realistic and predictable.

A DMP is not a loan. You make one monthly payment to the agency, which distributes the funds to your creditors under the new terms. This replaces multiple bills and deadlines with one clear payment plan, transforming financial chaos into structure. You are outsourcing the management and negotiation of your debts while focusing on consistent payments and rebuilding financial health.

A DMP is not debt settlement, which involves stopping payments to force creditors into settling for less than owed, often causing severe credit damage and tax liability. Instead, a DMP is cooperative, ethical, and designed to fulfill your obligations responsibly, preserving your financial reputation while helping you recover.

How Does the Debt Management Process Work?

The process begins with a free credit counseling session, where a certified counselor reviews your income, expenses, and debts to assess whether a DMP fits your needs. This session is confidential and educational, allowing you to explore options without pressure.

If a DMP is suitable, the counselor creates a personalized plan that outlines your new payment, program length (usually thirty-six to sixty months), and projected savings. After your approval, the agency begins creditor negotiations, using established relationships to secure reduced interest rates and concessions.

Most creditors prefer this arrangement because it ensures steady repayment. Once enough creditors agree, your plan becomes active, and you begin making consistent monthly payments to the agency.

Your role is to make each payment on time and monitor progress through a secure client portal, where you can track disbursements and see balances decline. Ask your counselor specific questions during the process.

For example, ask how long negotiations usually take, whether each creditor has agreed in writing, and how disputes are handled. Ask how often payments are disbursed and if there are backup options for transfers.

Upon completion, you receive a letter confirming all debts are paid in full. The experience often results in greater financial confidence, improved budgeting skills, and new savings habits.

What Does a Debt Management Plan Do?

A DMP simplifies finances by consolidating multiple payments into one predictable obligation. It reduces the risk of missed payments and late fees, allowing for smoother budgeting.

The main financial benefit is reducing the total cost of debt. Lower interest rates mean more of each payment goes toward principal rather than finance charges.

For example, ten thousand dollars in credit card debt at twenty-four percent APR could take more than twenty years and cost more than fifteen thousand dollars in interest if only minimums are paid.

Under a DMP that negotiates the rate down to eight percent, the same balance could be cleared in about four years with total interest of roughly two thousand six hundred dollars. The difference can reach more than twelve thousand dollars in savings, depending on balances and negotiated terms.

A DMP also provides a defined finish line, usually within three to five years, creating motivation to stay disciplined. It offers professional guidance, relieving you from creditor calls and stress. Credit counselors also provide education on budgeting, saving, and avoiding future debt, turning a financial crisis into an opportunity for growth.

Who Is Eligible for a DMP?

DMPs work best for people with unsecured debts such as credit cards, medical bills, or private student loans. Secured debts like mortgages or car loans cannot be included. Ideal candidates show genuine financial hardship but still have steady income to cover essential expenses and DMP payments.

Participants must be ready to follow the program rules, including closing enrolled accounts and maintaining consistent payments for several years. If an account has a co-signer, both parties may be affected, so discuss co-signed loans with your counselor.

Recipients of certain government benefits should confirm that enrollment will not affect eligibility for assistance or create cash flow conflicts. Counselors can build a realistic plan that accounts for public benefits and irregular income such as freelance payments.

What Are the Three Primary Methods of Debt Management?

There are three main approaches to handling unsecured debt. Understanding their differences helps you choose wisely.

- Debt Management Program (DMP)

A non-profit agency negotiates lower rates and waives fees, consolidating debts into one monthly payment for three to five years. You repay the full amount under more favorable terms. This is best for people with stable income who want to pay their debts ethically and need structured guidance.

- Debt Consolidation

This strategy involves taking out a new loan, such as a personal loan or balance transfer credit card, to pay off existing high-interest debts. It leaves you with one creditor and one payment.

It works best for borrowers with good credit who qualify for low-interest rates and can avoid accumulating new debt.

However, without discipline, it can worsen financial problems. Consider the length of the new loan, the presence of fees, and whether the consolidation loan actually lowers your total interest costs.

- Debt Settlement

A for-profit company negotiates to settle debts for less than owed, often instructing you to stop payments while saving funds in a separate account. This approach severely damages credit, invites collection actions, and can lead to tax liabilities on forgiven debt.

It is a last-resort option for those unable to make even minimum payments. Settlement may appear cheaper in the short term, but it carries long-term financial and legal risks.

Is It Worth Doing a Debt Management Plan? A Detailed Look at the Pros and Cons

A thorough and honest evaluation of the advantages and disadvantages is necessary before enrolling to ensure it aligns with your financial capabilities, goals, and personal discipline.

- The Advantages (Pros)

A DMP can significantly reduce interest rates, saving thousands over the program’s duration. One simplified monthly payment replaces multiple ones, reducing stress and minimizing missed payments. Once creditors begin receiving consistent payments, collection calls often stop, providing relief.

Completing a DMP means you fully repay what you owe, which reflects positively to future lenders. The structure fosters discipline and better money habits, helping you regain control of your finances.

Many people report reduced anxiety and improved sleep after the program begins, simply because they no longer face daily collection pressure.

- The Disadvantages (Cons)

The effect on your credit score is mixed. Closing accounts can temporarily lower your score because of reduced available credit. However, consistent on-time payments improve it over time. Missing payments can cause removal from the program and loss of benefits, so discipline is crucial.

DMPs only cover unsecured debts, and you must continue paying secured loans separately. There are modest setup and monthly fees, usually under one hundred dollars initially and twenty-five to fifty dollars monthly, which should be disclosed and compared to expected interest savings.

In rare cases an agency may charge different fees for clients with very complex portfolios. Always ask for a written fee schedule and an estimate of total fees over the life of the program. Inquire about refunds if you leave the program early and whether fees are refundable on a prorated basis.

Credit Score Impact Explained in Detail

A DMP affects credit in stages. Initially, accounts may be noted as “managed through a debt management program,” and closed accounts reduce available credit, causing a temporary dip. Over time, steady payments build a strong record, which improves scores.

As balances drop, your utilization ratio decreases, strengthening your credit. Within twelve to twenty-four months of consistent payments, many participants begin to see measurable score improvements.

By completion, many participants end up with higher credit scores and a cleaner financial record than before enrollment. Keep records of payment confirmations and request written proof of creditor agreements to resolve any reporting discrepancies.

How to Choose the Right Credit Counseling Agency

Choosing a reputable agency determines the success of your DMP. Select one accredited by the National Foundation for Credit Counseling (NFCC) or the Financial Counseling Association of America (FCAA). Accreditation ensures certified counselors, ethical practices, and transparency.

Verify the agency’s non-profit status through the IRS or by requesting its EIN. Avoid for-profit companies that pose as counselors, as they often charge excessive fees and use aggressive tactics. Always request fee transparency in writing. If an agency pressures you to sign up or promises guaranteed results, it is a red flag.

Look for agencies that emphasize education through workshops, budgeting tools, and personal coaching. Their goal should be to empower you, not just process payments. Strong customer service and technology also matter.

A secure online portal, responsive support, and clear communication reflect professionalism and commitment to your financial recovery. When you call or meet, ask how counselors are certified, how long the agency has operated, whether the agency has client references, and how it handles complaints.

Request a sample written agreement and confirm whether fees change after the first year. Red flags include high up-front fees, pressure to enroll immediately, and vague or evasive answers to basic questions.

Common Questions to Ask During the Free Counseling Session

Before you enroll, bring a list of questions to your free counseling session. Ask the counselor to explain how the agency will contact creditors and request written confirmations of any agreements.

Ask about the timeline for negotiations, how fees are assessed, whether accounts will be closed, and how early payoff is handled. Inquire about the agency’s complaint process and whether it offers follow-up coaching after the plan completes.

A Real-World Case Study: Maria’s Journey with a DMP

Maria, a graphic designer, had twenty-five thousand dollars in credit card debt across four cards with APRs from nineteen to twenty-six percent.

Her six-hundred fifty-dollar minimum payments barely reduced her balance, and collection calls caused constant anxiety. After consulting an NFCC-accredited agency, she enrolled in a DMP. The agency negotiated her average interest rate from twenty-two percent down to nine percent, reducing her payment to five hundred seventy-five dollars over forty-eight months.

The negotiated plan also eliminated late fees and reduced several penalty APRs. Maria’s monthly budget freed a small amount that she used to begin a modest emergency fund. Over the life of the plan she saved more than twelve thousand dollars compared with minimal payments.

The program restored her ability to sleep, stopped the collection calls, and gave her financial education and peace of mind to manage her money confidently in the future, ultimately resetting her financial life.

The Bottom Line

A Debt Management Program is a structured, ethical, and effective solution for individuals.

149 Comments

-

PHLove Online Casino: Register & Login Now for the Best Slot Games in the Philippines. Download the PHLove App for 24/7 Gaming Excellence! Experience PHLove Online Casino! Easy phlove register & phlove login for the best phlove slot games in the Philippines. Get the phlove app download for 24/7 fun. visit: phlove

-

[3418]Kingjl Login & Register: Top Philippines Online Casino, Kingjl Slot & App Download Experience the best at Kingjl, the #1 Philippines online casino! Complete your Kingjl login or Kingjl register to play premium Kingjl slot games. Enjoy secure gaming and get the Kingjl app download for big wins on the go! visit: kingjl

-

[6336]EM777: The Best Slot Gacor in the Philippines – Easy Login, Register, and Download APK via Official Link Alternatif. Experience the best slot gacor in the Philippines at EM777! Enjoy easy em777 login, fast em777 register, and secure em777 download apk via our official em777 link alternatif. Start your winning journey with the most trusted online casino platform today. visit: em777

-

[5445]Richjili: The Best Jili Slots Site & Legit Online Casino Philippines with GCash. Richjili is the best Jili slots site and a legit online casino in the Philippines. Experience top-rated online gambling with seamless GCash transactions. Access the Richjili official login now to enjoy premium games and big rewards at the most trusted PH gaming platform. visit: richjili

-

[4896]789taya Online Casino Philippines: Register & Login for Top Slots and App Download Experience the best at 789taya Online Casino Philippines! Enjoy premium 789taya slot games. 789taya register & login now for big wins. Get the 789taya app download today! visit: 789taya

-

[7801]FunBingo Philippines: Top Online Casino & Slots. Quick FunBingo Login, Register, and App Download to Play and Win Big. Experience FunBingo Philippines, the top online casino for slots! Quick FunBingo login, easy register, and FunBingo app download. Play and win big today! visit: funbingo

-

[7642]Otso Casino: The Best Legit GCash Online Casino and Slots in the Philippines. Experience Otso Casino, the premier online casino Philippines destination. As the best legit GCash online casino, we offer top-tier legit online slots Philippines and secure payouts. Visit otsocasino and use your otso casino login to start winning big at the most trusted gaming platform in the country! visit: otsocasino

-

[3507]mwcbet register|mwcbet login|mwcbet casino|mwcbet giris|mwcbet app Join MWCBet, the Philippines’ premier online casino platform. Complete your MWCBet register and login (giris) today to access a wide range of premium MWCBet casino games, including slots and live dealers. Download the MWCBet app for a seamless mobile gaming experience and start winning with the most trusted casino in PH! visit: mwcbet

-

[2252]Plot777: The premier Philippines online casino. Experience top-tier Plot777 slot online games. Fast Plot777 login, easy Plot777 register, and secure Plot777 app download via our official Plot777 casino link. Join Plot777, the premier Philippines online casino! Experience top-tier Plot777 slot online games today. Enjoy fast Plot777 login, easy Plot777 register, and secure Plot777 app download via our official Plot777 casino link for a premium gaming experience. visit: plot777

-

[3627]ah88 Login & Register: Top Philippines Online Slot Site. Download ah88 APK & Access Official ah88 Link Alternatif for Seamless Gaming. Join ah88, the top Philippines online slot site! Experience easy ah88 login and ah88 register processes. Download ah88 apk or use our official ah88 link alternatif to enjoy the best ah88 slot games and seamless gaming today. visit: ah88

-

[3469]Top Philippines Online Casino & Slot Games: Easy vipjl Login, Register, and Official vipjl App Download Today. Join vipjl, the top Philippines online casino for elite vipjl slot games. Experience easy vipjl login, fast vipjl register, and the official vipjl app download. Play and win big at the most trusted online gaming platform in the PH today! visit: vipjl

-

[6803]WJSLOT: Official Slot Gacor Site, WJSLOT Login & Register. Access Link Alternatif and Download APK for the Best Philippines Casino Experience. Experience the best Philippines casino at WJSLOT, the official slot gacor site. Easy WJSLOT login & register, access link alternatif, and download APK for big wins! visit: wjslot

-

[2693]Epicwin Online Casino Philippines: Easy Login, Register, and Download the Best Epicwin Slot Games for Big Wins Today. Join Epicwin Online Casino Philippines for big wins! Experience fast epicwin login & register processes. Get the epicwin download now to play premium epicwin slot games and enjoy the ultimate gaming experience today! visit: epicwin

-

[5922]BONS Official Site Philippines: Secure BONS Login & Casino Register. Play BONS Slots Online or Get the BONS App Download Today. Experience top-tier gaming at the BONS official site Philippines. Access a secure BONS login, fast BONS casino register, and the best BONS slots online. Enhance your experience with the BONS app download today! visit: BONS

-

[9355]PHPlus Online Casino: Top Slot Games in the Philippines. Login, Register, and Download the App to Win Big. Experience the best phplus slot games at PHPlus Online Casino Philippines! Phplus login, phplus register, or phplus download app today for your chance to win big. visit: phplus

-

[9810]Jili56 Casino Philippines: Jili56 Login, Register & App Download for Top Jili56 Slot Action. Experience the ultimate gaming at Jili56 Casino Philippines! Quick Jili56 login & register to play top Jili56 slot games. Get the Jili56 app download for non-stop casino action today. visit: jili56

-

[8506]The Best Legit Online Casino in the Philippines for Slots and More at 668jili visit: 668jili

-

[1124]Top646 Casino Login & Register: Best Philippines Online Slots & App Download Join Top646, the #1 Philippines online slots destination! Quick Top646 login and register to play premium games. Get the Top646 app download for mobile access and start winning at Top646 casino login today! visit: top646

-

[943]666jili Online Casino Philippines: Top Slot Games, Easy Login, Register & App Download Experience the ultimate 666jili Online Casino Philippines! Play top-rated 666jili slot games with a seamless 666jili login and quick 666jili register process. Get the 666jili app download for mobile gaming on the go. Join the #1 online casino in the PH today for massive jackpots and secure betting! visit: 666jili

-

[812]Gobetplay: #1 Philippines Online Casino. Secure Login, Register & App Download for Premium Slot Online & Official Link Alternatif. Join gobetplay, the #1 Philippines Online Casino! Secure gobetplay login, register & app download. Play premium gobetplay slot online via our official link alternatif today. visit: gobetplay

-

[832]Arina Philippines: Official Arina Login & Register. Play Arina Slot Online, Download APK, and Access the Latest Arina Casino Link Today. Join Arina Philippines today! Access the official Arina login & register to play Arina slot online. Download the Arina APK and get the latest Arina casino link now. visit: arina

-

[2399]PHL777 Online Casino Philippines: Easy Login, Register & App Download for the Best Slot Games Experience. Join PHL777 Online Casino Philippines for the best PHL777 slot games! Quick PHL777 login, easy register & secure app download. Play now and experience big wins! visit: phl777

-

[5989]No1JL: Best Online Casino in Philippines – Easy No1JL Login, Register & App Download for Top Slot Games Experience No1JL, the premier online casino in Philippines! Quick No1JL login, register & No1JL app download for top No1JL slot games. Join the #1 platform today! visit: no1jl

-

[3058]fbjili giris|fbjili download|fbjili register|fbjili slots|fbjili login Experience the best online gaming at fbjili, the Philippines’ top casino platform. Join today for easy fbjili register and fbjili login to play premium fbjili slots. Get the fbjili download for mobile access and start your fbjili giris to enjoy secure betting and massive rewards! visit: fbjili

-

[6477]The Philippines’ Best GCash Online Casino for Peso Betting and Top Slots. visit: pesomaxfun

-

[698]Experience the Best Online Casino in the Philippines with Phtaya 63 Slot Games and More. visit: phtaya 63

-

Is the fb777 VIP program worth joining? What kind of perks do they offer? Looking for some real experiences. fb777 vip

-

Needed to Okbet download and honestly it was the fastest install ever. Didn’t even have time to grab a beer! The app itself is pretty good. okbet download

-

PH88 is the spot to be! Been playing on ph88game.org for a few weeks now and I’m digging the variety of games. Site’s easy to navigate too. Get on it ph88

-

[4401]PHDream23 Casino: Login, Register & Download the Best Online Slots in the Philippines. Experience the ultimate gaming at PHDream23 Casino! PHDream23 login and register now to play the best online slots in the Philippines. Get the official PHDream23 download for mobile access to premium PHDream23 slot games, exclusive bonuses, and big wins today. visit: phdream23

-

[7713]jljl77 register|jljl77 login|jljl77 download|jljl77 casino|jljl77 giris Experience the ultimate online gaming destination at jljl77 casino, the Philippines’ leading platform for slots and live dealer games. Secure your jljl77 login or complete your jljl77 register today to unlock exclusive bonuses. Enjoy seamless mobile gaming with the jljl77 download app and access our official jljl77 giris portal for a safe and thrilling gambling experience. visit: jljl77

-

[723]AZ777 Official Link: Your Trusted Philippines Slot Online Destination. Fast AZ777 Login, Register, & App Download for Ultimate Casino Gaming. Experience the best gaming at AZ777, the top Philippines slot online destination. Access the AZ777 official link for fast login, easy register, and secure AZ777 app download to start winning today! visit: az777

-

[518]68jl register|68jl login|68jl giris|68jl casino|68jl download Experience the ultimate Philippines online gaming at 68jl. Complete your 68jl register to enjoy premium 68jl casino games, secure 68jl login, and big wins. 68jl download the app today for the best mobile gambling experience! visit: 68jl

-

[8387]AceSuper Login & Register: The Best Online Slots and Casino App Download in the Philippines. Join AceSuper, the premier online slots destination in the Philippines! Quick AceSuper login & register access. Get the AceSuper app download for a seamless casino login experience and big wins today. visit: acesuper

-

[108]Swerte88 Online Casino Philippines: Quick Login, Register & App Download for Premium Slot Games Join Swerte88 Online Casino Philippines for the ultimate gaming experience. Quick Swerte88 login and register to play premium Swerte88 slot games. Get the Swerte88 app download now for secure, fast, and exciting casino action! visit: swerte88

-

[4039]Kingjl Login & Register: Top Philippines Online Casino, Kingjl Slot & App Download Experience the best at Kingjl, the #1 Philippines online casino! Complete your Kingjl login or Kingjl register to play premium Kingjl slot games. Enjoy secure gaming and get the Kingjl app download for big wins on the go! visit: kingjl

-

[9387]077pub Official Site: Best Online Slots in the Philippines. Quick 077pub Login, Easy Register & Official App Download. Join 077pub Official Site, the #1 platform for online slots in the Philippines. Experience fast 077pub login, easy 077pub register, and the official 077pub app download. Play premium 077pub slots and win today! visit: 077pub

-

[1692]VipSlots: The Best Philippines Online Slots & Casino App. Secure VipSlots Login and Register to Start Winning. Fast VipSlots Download Available Now! Experience the best Philippines online slots at VipSlots! Secure your VipSlots login and register now to start winning. Get the fast VipSlots download for the ultimate VipSlots casino app experience. Join the #1 platform for secure gaming, exciting rewards, and non-stop action today. visit: VipSlots

-

[47]888phl Online Casino Philippines: Login, Register, App Download & Top Slots Join 888phl Online Casino Philippines! Secure your 888phl login, finish 888phl register, and enjoy top-tier 888phl slots. Get the 888phl app download today for the ultimate gaming experience and big wins! visit: 888phl

-

[7834]yyy777 Casino Philippines: Your Top Destination for Slots. Quick yyy777 Login & Register—Download the App for the Ultimate Gambling Experience! Join yyy777 Casino Philippines! Fast yyy777 login & register. Play the best yyy777 slot games and yyy777 download the app for a premium mobile gambling experience. visit: yyy777

-

[711]Karera Online Casino Philippines: Easy Login, Register, and App Download for the Best Slot Games. Join Karera Online Casino Philippines! Experience seamless Karera login and Karera register processes to enjoy top-tier Karera slot games. Get the Karera app download now for the ultimate mobile gaming experience and start winning today! visit: karera

-

[8038]jlfff Online Casino Philippines: Login, Register & App Download for Top Slots Join jlfff Online Casino Philippines! Quick jlfff login & jlfff register to play premium jlfff slot games. Get the jlfff app download now for the best mobile casino experience. visit: jlfff

-

[1727]jljl3355 login|jljl3355 app|jljl3355 casino|jljl3355 giris|jljl3355 slots Experience the ultimate online gaming at jljl3355 casino, the premier destination for Philippines players. Access your account via jljl3355 login or jljl3355 giris to enjoy a massive selection of jljl3355 slots and live dealer games. For seamless mobile action, download the jljl3355 app today and start winning with secure payouts and exclusive bonuses! visit: jljl3355

-

[3216]PHGolden Casino Philippines: Easy Login, Register & App Download for Top Slots Experience PHGolden Casino Philippines! Enjoy easy phgolden login, fast phgolden register, and phgolden app download. Play top phgolden slots and win big today. visit: phgolden

-

[8485]Sige77: Best Slot Online Philippines | Official Sige77 Login, Register & App Download Join Sige77, the best slot online platform in the Philippines. Access the official Sige77 login, register easily, and get the Sige77 app download or link alternatif today. visit: sige77

-

[4893]56jilicasino: The Top Philippines Online Casino – Register & Login for Premium Slot Games and Fast App Download Experience 56jilicasino, the top Philippines online casino. 56jilicasino register now for premium slot games. 56jilicasino login or use the app download for fast wins! visit: 56jilicasino

-

[781]CC6 Online Casino Philippines: Experience top CC6 slot games. Quick CC6 login, easy register, and CC6 app download for premium gaming and big wins today! Join CC6 Online Casino Philippines today! Quick CC6 login and easy CC6 register to enjoy premium CC6 slot games. Secure CC6 app download for big wins on the go! visit: cc6

-

[224]GalaxyBet: The Best Online Casino in the Philippines for GCash Gambling & Online Slots. Experience top-tier gaming at GalaxyBet, the best online casino in the Philippines. Enjoy seamless GCash online gambling PH and a massive variety of high-payout online slots Philippines. Secure your GalaxyBet PH login today to access exclusive bonuses and fast withdrawals at the most trusted GalaxyBet online casino Philippines. visit: galaxybet

-

[9004]The Best Online Casino in the Philippines: Bet777 App Download, GCash Slots, and Fast Payouts. visit: bet777app

-

[3031]Good88 Philippines: Best Online Casino & Slot Games. Quick Good88 Register, Login, and Official App Download. Join Good88 Philippines, the top online casino for premium good88 slot games. Quick good88 login, fast good88 register, and secure good88 download for mobile play. visit: good88

-

[5069]PPHWIN Official Link: Easy Login, Register & App Download for the Best Philippines Slot Games. Access the PPHWIN official link for easy pphwin login and pphwin register. Experience the best Philippines slot games and get the pphwin app download to play and win today! visit: pphwin

-

[3737]BW777 Login, Register & App Download: The Best Online Slot and Casino in the Philippines Experience the best online slot and casino games at BW777. Quick BW777 login and easy BW777 register for players in the Philippines. Secure your BW777 app download today to enjoy premium BW777 slot action and exclusive casino rewards anytime, anywhere! visit: bw777

-

[7913]Jili99 Online Casino Philippines: Fast Jili99 Login & Register. Enjoy Top Jili99 Slot Games and Official App Download. Experience Jili99 Online Casino Philippines! Fast Jili99 login & register for top Jili99 slot games. Get the official Jili99 app download for secure mobile play now. visit: jili99

-

[3024]Winph777 Online Casino Philippines: Secure Login, Easy Register, and App Download for Top Slot Games. Experience Winph777 online casino Philippines! Enjoy secure winph777 login, fast winph777 register, and top winph777 slot games. Get the winph777 app download now for elite gaming. visit: winph777

-

[8115]bethubph Online Casino: Your Top Choice for Slot Games in the Philippines. Register, Login, and App Download Today! bethubph Online Casino is the top choice for slot games in the Philippines. Experience easy bethubph login, quick register, and the bethubph app download today! visit: bethubph

-

[3329]pub555 Philippines: Top Slot Online, Easy Login & Register. Download App & Official Link Alternatif Now! Experience the best slot online gaming at pub555 Philippines! Secure your pub555 login, fast-track your pub555 register, and get the pub555 download app now. Access the official pub555 link alternatif for seamless casino action and big wins today! visit: pub555

-

[6721]NASA11 Login & Register: Best Slot Online in Philippines. Get the NASA11 Download APK & Official Link Alternatif. Join NASA11, the best slot online in the Philippines! Access NASA11 login & register pages, get the NASA11 download APK, or use our official link alternatif NASA11 now. visit: nasa11

-

[9287]Diwataplay Online Casino Philippines: Easy Login, Register for Top Slots, and App Download. Join Diwataplay Online Casino Philippines! Experience easy diwataplay login and register to play premium diwataplay slot games. Get the diwataplay app download today for the best mobile gaming experience and big wins! visit: diwataplay

-

[7626]fill777 Online Casino Philippines: Official Login, Register, and App Download for Premium Slot Games Join fill777 Online Casino Philippines! Secure fill777 login, easy register, and premium fill777 slot games. Get the fill777 download for mobile app. The #1 fill777 online casino! visit: fill777

-

[235]Bigwin29 Official Link: Secure Login, Register, and Play Top Slots. Download the Bigwin29 App Today for the Best Philippines Casino Experience. Access the Bigwin29 official link for secure Bigwin29 login and register. Play top Bigwin29 slot games and start the Bigwin29 app download for the best PH casino! visit: bigwin29

-

[1738]Jilievo Online Casino: Best Jilievo Slot Games in PH. Jilievo Login, Easy Register, and Fast Jilievo App Download for 24/7 Winning Action. Experience the best Jilievo slot games at Jilievo Online Casino PH. Quick Jilievo login, easy Jilievo register, and fast Jilievo app download for 24/7 winning action! visit: jilievo

-

[8809]30jili: Top Online Casino & Slot Games in the Philippines. Quick Login, Easy Register, and Mobile App Download. Experience 30jili, the top online casino in the Philippines. Play premium 30jili slot games with fast 30jili login and easy 30jili register options. Secure your 30jili app download today for the ultimate mobile gaming experience and big wins! visit: 30jili

-

[9159]Lago777 Official Site: Easy Login, Register & Top Online Slots in the Philippines. Download the Lago777 App for the Ultimate Casino Experience. Experience the Lago777 Official Site for the top online slots in the PH. Quick Lago777 login, easy Lago777 register & secure Lago777 app download. Win big today! visit: lago777

-

[6063]Deskgame Official: Secure Login, Register & App Download for the Best Philippines Slots. Join Deskgame Official for the ultimate Philippines slots experience! Access secure deskgame login, easy deskgame register, and the deskgame app download for premium casino gaming and big wins today. visit: deskgame

-

[5287]jili88ph: The Best Online Slots Philippines & Premier GCash Online Casino Experience world-class gaming at **jili88ph online casino**, the **best online slots Philippines** platform. Secure your **jili88ph login** today to explore a wide array of **jili slot games PH** and enjoy fast, secure payouts at the premier **GCash online casino Philippines**. Join jili88ph for the ultimate slot experience and big wins! visit: jili88ph

-

[3498]PH444 Online Casino: Secure Login, Registration & App Download for Top Slot Games. Join PH444 Online Casino for the best ph444 slot games! Enjoy secure ph444 login, fast ph444 registration, and easy ph444 app download. Play and win big at the top-rated online casino in the Philippines today. visit: ph444

-

[4150]UG777 Login & Register: Play the Best UG777 Slots, Official App Download, and Secure Link Alternatif for Philippines Players. Join UG777, the premier online casino for Philippines players. Experience seamless UG777 login and register today to play top-rated UG777 slots. Get the official UG777 app download and access our secure link alternatif for a safe, uninterrupted gaming experience. Start winning big at the most trusted UG777 platform! visit: ug777

-

[1069]365ph Online Casino Philippines: Best Slot Games, Easy App Download, Login & Register Today! Join 365ph Online Casino Philippines for the ultimate gaming experience! Enjoy top-rated 365ph slot games with a quick 365ph login. Complete your 365ph register today and get the seamless 365ph app download for mobile play. Experience secure winning at the best 365ph online casino now! visit: 365ph

-

[6220]Boss77 Login & Register: Best Philippines Slot Online. Official Boss77 App Download and Boss77 Link Alternatif for Secure Gaming. Experience the best Philippines slot online at Boss77. Easy Boss77 login & register. Get the official Boss77 app download & Boss77 link alternatif for secure gaming. visit: boss77

-

[2374]Pagtaya Online Casino Philippines: Easy Register, Login, and App Download for the Best Online Slots Experience. Join Pagtaya Online Casino Philippines for the best pagtaya online slots. Easy pagtaya register & pagtaya login. Get the pagtaya app download for non-stop action. Start your pagtaya casino sign up now to win big! visit: pagtaya

-

[5784]7signs Casino Philippines: Quick Login & Register Online. Download the 7signs App for Top Slot Games and Exclusive Casino Bonuses. Experience the best at 7signs Casino Philippines! Quick 7signs casino login & 7signs register online. Download the 7signs app for top 7signs slot games and claim your exclusive 7signs casino bonus today. visit: 7signs

-

I gotta say, 8sbetapp is pretty solid. The mobile app is super convenient, and they have a surprisingly good selection of sports betting options. Give 8sbetapp a try if you like betting on the go.

-

Someone told me to try jilipark2 and I was pleasantly surprised. Solid selection and easy to navigate. Worth checking out, especially the slots. Get on over to jilipark2.

-

Heard good things about mm88comn, gonna give it a shot tonight. Fingers crossed for some luck! Check it out: mm88comn

-

lygs41

-

ncrihg

-

ohxd50

-

drb4p9

-

smkjm1

-

References:

Elexus resort lara Köln Hbf Casino

-

cb2kx5

-

References:

Craps come bet exelentsmart.com

-

lq4bh6

-

49t6xd

-

62sg9b

-

j7afih

-

References:

Legiano Casino Cashback http://images.google.co.th/

-

References:

Legiano Casino Lizenz https://board-en.skyrama.com/proxy.php?link=https://bion.ly/roscoesides59

-

References:

Legiano Casino Promo Code clients1.google.ng

-

References:

Legiano Online Casino geodesist.ru

-

References:

Legiano Casino Bonus http://maps.google.ms/

-

References:

Legiano Casino Meinungen google.com.hk

-

References:

Legiano Casino Kritik http://www.ensembl.org/

-

References:

Legiano Casino Live Casino http://forum.darnet.ru/go.php?smartbusinesscards.in/chaunceys63468

-

References:

Legiano Casino Kundenservice camslaid.com

-

References:

Legiano Casino seriös cse.google.com.nf

-

References:

Legiano Casino Login Deutschland https://en.lador.co.kr/member/login.html?noMemberOrder=&returnUrl=http://www.textise.net/showtext.aspx?strurl=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Ligiano Casino images.google.cz

-

References:

Legiano Casino Mindestauszahlung images.google.cl

-

References:

Legiano Casino Kundenservice palm.muk.uni-hannover.de

-

References:

Legiano Casino Gratis Spins toolbarqueries.google.com.hk

-

References:

Legiano Casino Login http://m.landing.siap-online.com

-

References:

Legiano Casino Verifizierung offers.sidex.ru

-

References:

Legiano Casino Registrierung http://shababzgm.alafdal.net/

-

References:

Legiano Casino Support http://www.visit-x.net/promo/dyn/dynchat02.php?pfmbanner=1&ver=12&clickurl=https://de.trustpilot.com/review/edelkranz.de

-

References:

Legiano Casino Deutschland https://52.cholteth.com/index/d1?an&aurl=https://de.trustpilot.com/review/edelkranz.de

-

References:

Legiano Casino Auszahlung oluchi.yn.lt

-

References:

Legiano Casino Mindesteinzahlung http://maps.google.mw/url?q=https://ix.sk/KmA1x

-

References:

Legiano Casino PayPal http://www.google.ca/

-

References:

Legiano Casino Bonus ohne Einzahlung forum.donanimhaber.com

-

References:

Legiano Casino Jackpot http://toolbarqueries.google.com.pe

-

References:

Legiano Casino Spielautomaten https://comita.ru/

-

References:

Legiano Casino sicher hoyot.nnov.org

-

References:

Legiano Casino Spielautomaten https://www.forosperu.net/proxy.php?link=https://sosi.al/richardstrehlo

-

References:

KingMaker Casino Einzahlungsbonus 100% https://mssq.me

-

References:

Kingmaker Casino Login Deutschland https://liy.ke

-

References:

Kingmaker Casino Bewertungen https://wsurl.link/

-

References:

Kingmaker casino echtgeld spielen einzahlung maps.google.bj

-

References:

Kingmaker Casino Software http://clients1.google.co.ck/url?q=http://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker kreditkarte einzahlung http://www.google.com.gh/url?sa=t&url=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker Casino Einzahlung mit Trustly https://id.readymap.info

-

References:

KingMaker Casino Einzahlung per Klarna tulum.ru

-

References:

Kingmaker Casino Deutschland https://kak2z.ru

-

References:

Legiano Casino Login Deutschland williz.info

-

References:

Legiano Casino Gutschein alt1.toolbarqueries.google.com.nf

-

References:

KingMaker einzahlung paysafecard https://www.paltalk.com/linkcheck?url=https://sosi.al/chauadkins7371

-

References:

Legiano Casino Erfahrungen http://portal.novo-sibirsk.ru

-

References:

Legiano Casino Treueprogramm cse.google.co.ck

-

References:

Legiano Casino Promo Code https://forums.bit-tech.net/

-

References:

KingMaker einzahlen http://shop2.parisyang.cafe24.com/member/login.html?returnUrl=https://www.mydaradstools.com/juliet76c

-

References:

KingMaker einzahlung gebühren forum.truck.ru

-

References:

KingMaker Casino Registrierungsbonus http://toolbarqueries.google.com.gt/url?sa=t&url=https://heres.link/janeenheffron5

-

References:

Kingmaker Casino Betrug oder seriös riversracing.xsrv.jp

-

References:

Legiano Casino VIP Programm http://k.scandwap.xtgem.com/?id=irenon&url=telegra.ph/Legiano-Casino-500-Bonus–200-Freispiele-06-07

-

References:

KingMaker Casino Einzahlung jetzt maps.google.com.ar

-

References:

Kingmaker Casino Einzahlung https://iframely.pagina12.com.ar/api/iframe?url=https://sbfpageing.com/utzyy&v=1&app=1&key=68ad19d170f26a7756ad0a90caf18fc1&playerjs=1

-

References:

Leggiano Casino http://clients1.google.com.ai

-

References:

Monro Casino Free Spins https://forums.wynncraft.com/proxy.php?link=https://spd.link/megangurle

-

References:

Hitnspin casino promo code toolbarqueries.google.kz

-

References:

Monro Casino Jackpot https://mcpedl.com/leaving/?url=https://innvo.pro/deneselons&cookie_check=1https://abouttexasholdempoker.blogspot.com

-

References:

Hit’n’spin casino 50 free spins http://g.i.ua/?userID=6897361&userID=6897361&_url=https://link.zhihu.com/?target=http://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hit n spin casino promo code https://delta.astroempires.com

-

References:

Hitnspin casino auszahlungslimit gunsnrosesforum.de

-

References:

Hitnspin casino willkommensbonus googleadservices.com

-

References:

Hitnspin casino trustpilot http://image.google.ps/url?q=http://wiki.integral.ru/api.php?action=https://de.trustpilot.com/review/der-wikinger-shop.de

-

8w16cx