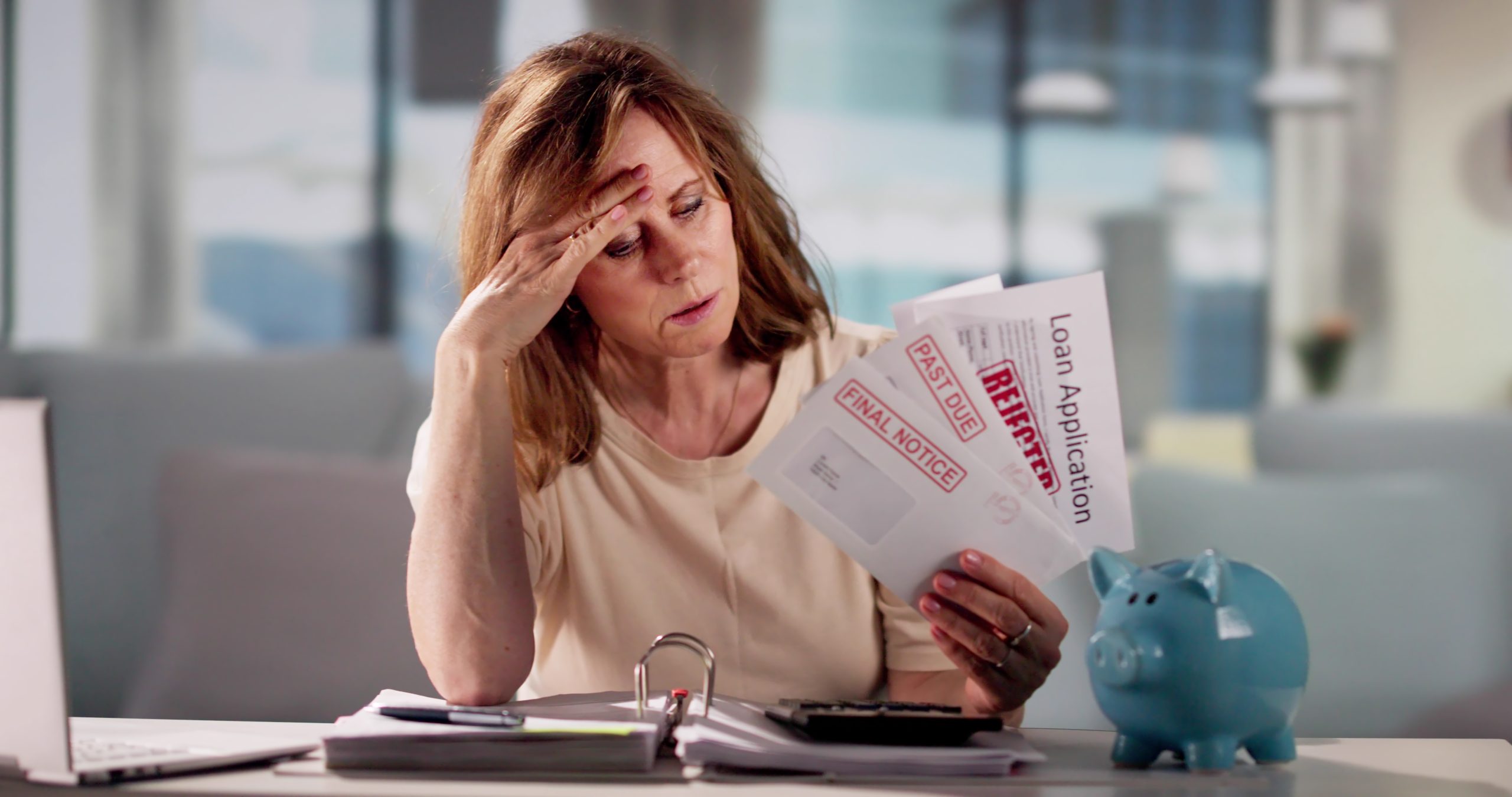

Sometimes, debt is straightforward. If you’ve taken a loan, you must repay it to the creditor. However, debt can become complicated when debt collectors are involved. These collectors can interfere with, possibly derail, the entire repayment process. Today, we’ll cover how to save yourself a whole world of trouble with a debt validation letter.

Understanding your rights and the proper steps to take when dealing with debt collectors is crucial. It is essential to know what a debt validation letter (and its counterpart, the debt verification letter) is. This letter ensures that the claimed debt is legitimate and correctly attributed to you or that an incorrectly claimed debt can be dealt with quickly.

What is a debt validation letter?

A debt validation letter is a document that debt collectors are required to provide by law, detailing:

- The amount of debt

- The creditor to whom the debt is owed

- And your rights regarding the dispute over this debt

If debt collectors first contact you by phone, first things first, request a debt validation letter. Under the Fair Debt Collection Practices Act (FDCPA), a debt collector must provide a written debt validation letter within five days. Failing to do so is a direct violation. It can be reported to the Federal Trade Commission (FTC), the Consumer Financial Protection Bureau (CFPB), or your state’s attorney general.

Let’s say you received one and aren’t sure what the next step is after receiving the debt validation letter. There are two routes:

Read it carefully. Make sure it’s error-free and accurate. If it’s correct, then it’s time to pay off the debt.

- If, upon reading it, you find the letter to have misinformation

- then it’s time to respond accordingly.

For this, we’ll cover how to dispute a debt validation letter - how to send it, and other essential details

How to dispute a debt validation letter

After receiving a debt validation letter that needs to be disputed, send one back. With any debt validation letter comes a debt verification letter/dispute letter. It is important to manage and dispute debts you are unaware of or believe to be inaccurately reported.

Side note

You may notice that debt validation and debt verification are often used interchangeably online. Most people think you need to figure out how to write a debt validation letter when it’s a debt verification letter. There’s a clear distinction between the two:

Debt validation: What a debt collector sends to validate a debt.

Debt verification: What you send in return to verify or formally dispute the information in the letter.

This will be your secret weapon to smooth out the process, no matter what kind of debt you’re paying off. If you dispute the debt in writing, the debt collector must provide written evidence of the debt to rid yourself of falsified debt claims.

Keep in mind that you must send a response within 30 days. Failing to do so indicates that the debt is valid.

How to write a debt verification letter

Writing a debt verification letter can be intimidating when being chased by debt collectors. However, this letter can provide you with some relief, even if it’s temporary.

Besides ensuring the claim is valid (or invalid), sending a letter disputing your debt helps halt the hounding. Your debt collectors are legally prohibited from contacting you except in response to your letter (and must be in writing).

Along with stating that you’re not responsible for the debt collected, the debt collector must provide you with some details. Here are some of the details that you should include in your letter:

- Evidence that the debt belongs to you

- The amount you owe (based on the last statement or bill)

- Whether the debt is beyond the statute of limitations

- The most recent action taken on the account

- Proof that the debt collector is authorized and licensed to pursue the debt in your state

There are plenty of free debt validation letter templates online. Download one to have on hand, so you can fill in your details and tweak the letter to fit your situation.

Sending your debt verification letter

Once your letter is prepared, send it via certified mail and request a return receipt. This way, you’ll have legal proof of delivery within the required timeframe.

Additional tips for handling debt validation letters

When dealing with debt collectors, stay cool, calm, and informed. One of the most effective ways to protect yourself is by knowing the right steps to take. Responding to debt validation letters promptly is important, but here are a few more notes for the journey.

Keep records of all correspondence

Every document should be stored. When dealing with debt collectors, it’s important to keep records of all communications. From letters received to phone calls (and their date and time), emails received, and anything you’ve sent as well.

Take notes during phone conversations with debt collectors, including the names of the representatives you speak with, the time and date of the call, and any promises or agreements made.

If anything feels suspicious or wrong, it can be used as evidence in your favor. This will help you track your dispute process and provide proof if the situation escalates.

Understand the statute of limitations

The statute of limitations refers to the maximum period during which a debt collector can take legal action to collect a debt. This time frame varies depending on the type of debt and the state you live in.

If the debt in question has passed this deadline, you may be able to request that the collector stop pursuing the debt entirely. This can be an essential tool in your dispute process.

Don’t ignore debt validation letters

If a debt collector continues to pursue a debt after you’ve asked for validation, or if they fail to provide you with the proper documentation, don’t ignore it. Ignoring debt collectors may lead to legal action or additional fees. Continue to exercise your rights by formally requesting validation or disputing the debt.

In summary

Responding to debt validation letters can help you defend against false or fraudulent debt claims. This approach empowers you with knowledge and documentation to support necessary legal actions and protects you against wrongful accusations.

By knowing your rights and following proper procedures, you can manage and resolve disputes effectively. Whether through a debt relief program or simply staying informed, it’s important to take control of your financial situation and protect your peace of mind.

Disclaimer: The information provided in this article is for general informational purposes only and is not intended as legal, financial, or professional advice. We do not guarantee any specific outcomes, and results may vary based on individual circumstances. We comply with all applicable laws, including the California Debt Settlement Services Act, and recommend consulting with an attorney or financial advisor before making any financial decisions. We are not responsible for the accuracy of external links or content, and all website content is protected by copyright laws. We reserve the right to update or remove content at any time without notice.

–

Frequently asked questions

Is a 609 debt validation letter related to normal debt validation letters?

Not exactly, however, it’s important to know what they are. If you’re facing inaccurate, negative, or untrue information on your credit report, a 609 debt validation letter (aka a 609 dispute letter) comes in handy.

It is based on two sections of the Fair Credit Reporting Act (FCRA).

Section 609 – which allows you to request credit card reports and other recorded information.

Section 611 – which summarizes your rights to dispute inaccurate information in the report.

By identifying what needs to be disputed and asking the credit agency to validate that information, you can have it removed from your report.

Can I send a debt validation letter after 30 days?

Unfortunately, no. A debt collector can assume the debt they’re attempting to collect is valid if you don’t dispute it within 30 days of initial contact. As with most things, sort it out sooner than later.

What should I do if the debt collector doesn’t validate the debt within 30 days?

If the debt collector fails to validate the debt within 30 days, they are legally required to stop all collection efforts. You can request that they provide proof of the debt in writing. If they still don’t comply, you may want to file a complaint with the Consumer Financial Protection Bureau (CFPB) or consult with a credit attorney.

Can I get away with no response to a debt validation letter?

Ignoring a debt validation letter is not advised. Failing to respond within 30 days essentially forfeits your right to dispute the debt, allowing the collector to assume the debt’s validity. Always respond promptly to validate the debt or dispute inaccuracies.

What’s a medical debt validation letter?

A medical debt validation letter is like any other one, but specifically pertains to medical debts. Given the complexity and frequency of billing errors in healthcare, you must request validation for any medical debt to confirm it’s accurate and correct.

What’s a Sherry Beckley debt validation letter?

It’s not too far off from a standard debt validation letter. To be exact, this is a considerable part of what Sherry Beckley—a credit coach and online personality—promotes as part of her work.

Can a debt collector continue to contact me if I request validation?

No, once you request a debt validation, the collector must cease collection efforts until they provide proof that the debt is valid. This is part of your rights under the Fair Debt Collection Practices Act (FDCPA). If they continue to contact you after your validation request, they may be violating the law.

It’s important to keep a record of your request in writing so you have proof of the date and content of your communication. You can also request that all future communications be in writing, which can help protect you from harassment or repeated phone calls. Remember, debt collectors are legally obligated to respond to your validation request and provide documentation of the debt, including the amount owed, the original creditor, and other relevant details. If they fail to do so, you have the right to dispute the debt and report any violations to the Consumer Financial Protection Bureau (CFPB) or your state attorney general’s office.

157 Comments

-

[8373]jl365 Online Casino Philippines: Quick jl365 Login, Register, and App Download for the Best jl365 Slot Games. Experience the top jl365 online casino Philippines! Fast jl365 login, easy jl365 register & jl365 app download. Play the best jl365 slot games & win big today! visit: jl365

-

[9280]jljl55 casino|jljl55 register|jljl55 slots|jljl55 login|jljl55 download Welcome to jljl55 casino, the premier online gaming destination in the Philippines. Quick jljl55 register and jljl55 login to enjoy massive rewards on jljl55 slots. Secure your jljl55 download today for the best mobile casino experience and start winning real prizes! visit: jljl55

-

[4967]PUB777 Official Site: Best Slot Online Casino in the Philippines. Easy PUB777 Login, Register & App Download for Big Wins. Join PUB777 Official Site, the top-rated slot online casino in the Philippines. Secure PUB777 login, easy PUB777 register, and fast PUB777 app download for massive wins today! visit: pub777

-

[3621]Phcash: Best Philippines Online Slot & Casino – Easy Register, Login, Sign Up & App Download. Join PHCASH, the best Philippines online slot & casino. Experience seamless phcash login, quick phcash register, and easy phcash casino sign up. Get the phcash app download now for top-tier online slots and a premium gaming experience anytime, anywhere! visit: phcash

-

[8884]Winforlife Online Casino Philippines: Register & Login for Premium Slots and Easy App Download. Experience Winforlife Online Casino, the Philippines’ top destination for premium winforlife slots. Winforlife register today, secure your winforlife login, and get the winforlife app download for elite mobile gaming! visit: winforlife

-

[9282]w777: The Best Legit Online Casino in the Philippines – Top GCash Slots & Live Dealer Games Experience premier gaming at **w777**, the best online gambling site in the Philippines. As a top-rated **w777 legit casino GCash** players trust, we provide an elite selection of **online slots Philippines w777** enthusiasts love, plus immersive **w777 live dealer games PH**. Join the most reliable **w777 online casino Philippines** for secure transactions, fast payouts, and a world-class casino experience. visit: w777

-

[5051]The Best Online Casino in the Philippines: Experience Top Slots and Easy GCash Payments at 2222ph. visit: 2222ph

-

[5261]BMW55 Philippines: Best Slot Gacor Platform – Easy Login, Register & Download APK. Official Link Alternatif Available Now. Experience the best slot gacor at BMW55 Philippines! Easy bmw55 login and bmw55 register process. Get the official bmw55 link alternatif and bmw55 download apk now. visit: bmw55

-

[3853]WineHQ Online Casino: The Best Legit Real Money Casino in the Philippines. Experience top-tier gaming at WineHQ Online Casino, recognized as the best legit real money casino in the Philippines. Fast-track your winnings with a secure WineHQ login or enjoy seamless play via the WineHQ Casino app download. Join the most trusted online casino Philippines has to offer and start winning real cash today! visit: winehq

-

[502]Winph111 Login & Register: The Best Legit Philippines Casino. Experience Top Winph111 Slot Games and Fast Winph111 App Download Today! Winph111 is the top legit Philippines casino! Secure your Winph111 login & register to enjoy premium Winph111 slot games. Fast Winph111 app download available now. visit: winph111

-

[4685]Jili33 Online Casino Philippines: Top Jili33 Slots, Easy Login, Register & App Download Experience Jili33 Online Casino Philippines! Enjoy top Jili33 slots, easy Jili33 login, fast register, and the official Jili33 app download. Join now for big wins! visit: jili33

-

[7221]Jili3 Official Casino Philippines: Register, Login, and App Download for the Best Slot Games. Join Jili3 Official Casino Philippines! Easy Jili3 register & Jili3 login to play top Jili3 slot games. Get the Jili3 app download for the best mobile experience today. visit: jili3

-

[448]2ph Online Casino: Secure 2ph Login, Register & App Download for Premium PH Slots. Experience premium gaming at 2ph Online Casino! Secure 2ph login & 2ph register for access to top-tier 2ph slots. Get the 2ph app download today for the best PH casino action. visit: 2ph

-

[627]jljl3355 login|jljl3355 app|jljl3355 casino|jljl3355 giris|jljl3355 slots Experience the ultimate online gaming at jljl3355 casino, the premier destination for Philippines players. Access your account via jljl3355 login or jljl3355 giris to enjoy a massive selection of jljl3355 slots and live dealer games. For seamless mobile action, download the jljl3355 app today and start winning with secure payouts and exclusive bonuses! visit: jljl3355

-

[1413]The Best Online Casino in the Philippines: Download the GKBet App and Play with GCash today! visit: gkbet

-

[3505]Q25Casino: The Best Legit Online Casino in the Philippines for Slots. Easy GCash Login & Fast Registration. Experience Q25Casino, the premier legit online casino in the Philippines specializing in the best online slots Philippines has to offer. Enjoy a seamless q25casino login gcash experience and a fast q25casino register process for immediate play. Join the most trusted platform for legit online gambling philippines and start winning today with q25casino online casino philippines. visit: q25casino

-

[5470]9ajili Online Casino Philippines: Easy Login, Register & App Download for the Best Slots Experience Experience the ultimate gaming at 9ajili Online Casino Philippines. Enjoy a seamless 9ajili login, fast 9ajili register, and the latest 9ajili app download for the best 9ajili slots and live games. Join the most trusted online casino in the PH today for massive jackpots and premium rewards! visit: 9ajili

-

[3405]Reebet Official Site Philippines: Seamless Reebet Login, Register, App Download & Top Online Slots. Experience world-class gaming at the Reebet official site Philippines. Access your account via reebet login, complete your reebet register quickly, and secure the reebet app download for premium mobile play. Discover the best reebet slots and exclusive casino rewards today—your ultimate winning journey starts here! visit: reebet

-

[6414]10jili Online Casino Philippines: Top Slot Games, Easy Login, Register, and App Download. Experience the best 10jili Online Casino Philippines! Access top 10jili slot games with a quick 10jili login or 10jili register. Get the 10jili app download now for big wins and exclusive rewards today! visit: 10jili

-

[3466]Jilibet Online Casino: Easy Jilibet Login, Register & App Download for Best Jilibet Slots in the Philippines. Experience the best Jilibet Online Casino in the Philippines! Secure jilibet login & register to play top jilibet slot games. Jilibet app download available now for big wins on the go. visit: jilibet

-

[9085]639jl slots|639jl giris|639jl login|639jl download|639jl app Experience premier online gaming at 639jl, the leading casino platform in the Philippines. Enjoy a wide variety of 639jl slots, secure 639jl login, and easy 639jl download options. Install the 639jl app or use our 639jl giris link to start your winning journey with top bonuses today! visit: 639jl

-

[1143]NicePH Online Casino: Your Premier PH Destination for Slot Games. Register, Login, and Get the NicePH App Download Today for the Ultimate Gaming Experience! Experience the ultimate thrill at NicePH Online Casino, the premier PH destination for top niceph slot games. Complete your niceph register and login to start winning today. Get the niceph app download for a seamless mobile gaming experience anytime, anywhere! visit: niceph

-

[5108]Taya777 Casino Online Philippines: Secure Login, Easy Register & App Download for the Best Slots Experience. Join Taya777 Casino Online Philippines for the ultimate gaming experience! Access secure Taya777 login, fast Taya777 register, and the Taya777 app download to enjoy the best Taya777 slots and premium casino games today. visit: taya777

-

[6125]p828: Best Online Casino Philippines. Access p828 Login, p828 Slot, and Daftar p828 via the latest p828 Link Alternatif. Download p828 APK for premium gaming! Join p828, the best online casino in the Philippines! Experience premium gaming with top-rated p828 slot titles, secure p828 login access, and seamless daftar p828 registration via our official p828 link alternatif. Download the p828 apk today to enjoy a world-class mobile casino experience with massive jackpots and 24/7 support at your fingertips. visit: p828

-

[6130]SMJL Online Casino Philippines: Your Trusted Hub for SMJL Login, Register, and App Download to Enjoy the Best SMJL Slot Games Today. Join SMJL Online Casino Philippines! Access secure SMJL login, easy SMJL register, and fast SMJL app download. Play the best SMJL slot games and win big today! visit: smjl

-

[799]SuperLG Online Casino: The Best and Most Legit Online Gambling Platform in the Philippines. Experience **SuperLG Online Casino**, the **best online casino Philippines** has to offer. As the most **legit online gambling PH** platform, SuperLG provides a secure and licensed environment for slots, live dealers, and sports betting. Use your **SuperLG login** to access exclusive bonuses and fast payouts. Join **SuperLG Casino Philippines** today and play at the country’s most trusted destination for premium online gaming. visit: superlg

-

[9823]Filbet Philippines: Official Filbet Login & Register. Play Top Filbet Slot, Casino Games & App Download. Experience the best of Filbet Philippines! Access the official Filbet login and register page to play premium Filbet slot and casino games. Get the Filbet download for mobile and start winning today! visit: filbet

-

[6583]ff777 Online Casino Philippines: Quick Login, Register & App Download for the Best Slots Experience Experience ff777 Online Casino Philippines! Quick ff777 login, easy ff777 register, and top ff777 slot games. Get the ff777 app download now and win big today! visit: ff777

-

[1995]Betpk Online Casino Philippines: Secure Betpk Login, Register, and App Download for the Best Online Slots and Casino Games. Join Betpk Online Casino Philippines for secure betpk login, easy betpk register, and betpk app download. Play the best betpk slots & casino games. Sign up now! visit: betpk

-

[7546]Wagibet931: Login & Daftar Slot Gacor Terpercaya. Download APK Wagibet931 & Link Alternatif Resmi Terbaru. Wagibet931 adalah platform slot gacor terpercaya di Philippines. Segera daftar & login Wagibet931 untuk menang besar. Download APK Wagibet931 & akses link alternatif resmi terbaru sekarang! visit: wagibet931

-

[5101]JILI8 Online Casino Philippines: Quick JILI8 Login, Register & App Download. Play the Best JILI8 Slots and Win Big Today! Experience JILI8 Online Casino Philippines! Quick JILI8 login & register to play top JILI8 slots. Get the JILI8 app download for mobile fun & win big today! visit: jili8

-

[8904]gogojili Casino Philippines: Easy Login, Register, and App Download for the Best Online Slots. Join gogojili Casino Philippines for the ultimate gaming experience! Enjoy easy gogojili login, fast register, and quick gogojili app download to play the best gogojili slots and win big today. visit: gogojili

-

[8013]777perya Online Casino Philippines: Easy Login, Register & App Download for the Best Slot Games. Join 777perya Online Casino Philippines! Experience easy 777perya login, fast register, and the official app download for top-tier slot games. Play and win today! visit: 777perya

-

[9369]9999jili: The #1 Legit Online Casino in the Philippines for Premium Jili Slots & Big Wins. Experience 9999jili, the #1 legit online casino in the Philippines. Discover premium Jili slots Philippines and massive jackpots on the most trusted platform. Secure your 9999jili login today to enjoy the best online casino Philippines experience with top-tier rewards and legit online gambling. visit: 9999jili

-

[7061]jljl16 Casino: The Top Online Slot Platform in the Philippines. Fast jljl16 Login, Easy Register, and Official jljl16 App Download for Big Wins. Experience jljl16 Casino, the top online slot platform in the Philippines. Fast jljl16 login, easy register, and official jljl16 app download for big wins today! visit: jljl16

-

[2928]Bet100 Official Site: Best Philippines Online Slots, Easy Login, Register & App Download Experience the best Philippines online slots at the bet100 official site. Enjoy a quick bet100 login, easy bet100 register, and secure bet100 app download. Join now! visit: bet100

-

[7641]a777 Online Casino Philippines: The Best Legit Slots for Real Money and Easy GCash Payouts. Experience the ultimate gaming thrill at a777 Online Casino Philippines, the top destination for the best online slots PH. Secure your a777 legit casino login today to play exciting games for real money and enjoy the fastest online gambling GCash Philippines payouts. Join a777 casino real money for a safe, legit, and rewarding experience tailored for Filipino players. visit: a777

-

[2678]ph35: Best Philippines Online Slot & Casino. Fast ph35 login, easy ph35 register, and official ph35 app download. Access your ph35 casino login for big wins! Experience the best Philippines online slot and casino at ph35. Enjoy fast ph35 login, easy ph35 register, and the official ph35 app download. Access your ph35 casino login now to play premium ph35 slot games and start winning big today! visit: ph35

-

[5686]phwin99 Online Casino Philippines: Fast phwin99 Login, Register, & App Download. Experience the Best phwin99 Slot Games Today! Join phwin99 online casino, the premier gaming destination in the Philippines. Enjoy fast phwin99 login, easy phwin99 register, and phwin99 app download. Play the best phwin99 slot games and win big today! visit: phwin99

-

[5831]377jili Casino & Slot: Official Login, Register, and App Download for the Best Online Gaming in the Philippines. Join 377jili Casino for the best online gaming experience in the Philippines. Secure 377jili login, easy register, and 377jili app download for premium 377jili slot games and big wins today! visit: 377jili

-

[2510]Letswin Online Casino Philippines: Quick Letswin Login & Register. Play Top Letswin Slots & Secure your Letswin App Download for the Ultimate Gaming Experience. Experience Letswin Online Casino Philippines! Quick Letswin login & register to play top Letswin slots. Secure your Letswin app download for the best gaming now. visit: letswin

-

[3897]jlboss casino|jlboss login|jlboss download|jlboss register|jlboss giris Experience top-tier gaming at jlboss casino, the Philippines’ favorite online platform. Enjoy secure jlboss login, easy jlboss register, and fast jlboss download for mobile play. Use jlboss giris for instant access to premium slots and live dealer games today! visit: jlboss

-

[6795]kk777 Login & Register: Best Online Slot Casino in the Philippines | Download the kk777 App Now Join kk777, the best online slot casino in the Philippines! Complete your kk777 register and kk777 login to play top kk777 slot games. Download the kk777 app now for a premium mobile gaming experience and secure your kk777 casino login to start winning big today! visit: kk777

-

[485]Megaperya Login, Register & App Download: Your Top Philippines Online Slots & Casino Hub Join Megaperya, the top Philippines online slots hub. Easy megaperya register, fast megaperya login, and megaperya app download. Access your megaperya casino login today! visit: megaperya

-

[2089]jiliko747 download|jiliko747 app|jiliko747 slots|jiliko747 casino|jiliko747 login Join jiliko747 casino, the top Philippines gaming site. Get the jiliko747 app via download, use your jiliko747 login, and play premium jiliko747 slots to win today! visit: jiliko747

-

[9402]91ph Casino: Official Login, Register & App Download. Play the Best 91ph Slots in the Philippines Today! Join 91ph Casino for the top 91ph slots in the Philippines! Secure your 91ph login, fast 91ph register, and easy 91ph app download to start winning big today. visit: 91ph

-

[9341]123jili Casino Philippines: Official 123jili Login, Register & App Download. Play the Best 123jili Slots Online Today! Join 123jili Casino Philippines for the best 123jili slot games. Official 123jili login, easy 123jili register & 123jili app download. Start winning today! visit: 123jili

-

[2234]GG777 Online Casino Philippines: Easy GG777 Login & Register. Play GG777 Slot & Get the GG777 App Download for Big Wins! Experience the best at GG777 Online Casino Philippines. Enjoy quick GG777 login and register to play premium GG777 slot games. Get the official GG777 app download now for a chance at big wins and secure gaming! visit: gg777

-

[347]Like777: The Best Online Casino Philippines for Legit Slot Games & Real Money GCash Wins. Experience Like777, the best online casino Philippines for legit slot games and real money wins. Join the premier GCash online casino real money platform today and enjoy the most trusted online casino Philippines for real money experience with fast payouts and non-stop excitement. visit: like777

-

[2441]Sulit777: Best Philippines Online Casino & Slots. Easy Sulit777 Login, Register, and App Download for Big Wins. Experience the best Philippines online casino at Sulit777! Get fast Sulit777 login and register access to play top Sulit777 slot and casino games. Sulit777 download the app now for big wins and exclusive rewards! visit: sulit777

-

[1565]Jilifish Online Casino Philippines: Best Slot Games, Jilifish Login, Register, and App Download. Experience the best Jilifish slot games at Jilifish Online Casino Philippines. Secure Jilifish login, quick register, and Jilifish app download. Play and win now! visit: jilifish

-

[707]nh88 Casino: Best Philippines Online Slots. Easy nh88 Register, Login, and App Download. Experience the best Philippines online slots at nh88 casino. Enjoy a seamless nh88 register process and nh88 login to play top-tier nh88 slot games. Start your nh88 download today for the ultimate mobile gaming experience and big wins! visit: nh88

-

[3389]677jili casino|677jili slots|677jili app|677jili register|677jili giris Join 677jili, the premier online casino in the Philippines. Experience top-rated 677jili slots, download the official 677jili app, and complete your 677jili register today for secure giris access and exclusive rewards. visit: 677jili

-

[7034]Phpfamous: Best Slot Gacor Philippines. Login, Register, & Download APK for Real-Time RTP Live & Big Wins! Join Phpfamous, the best slot gacor in the Philippines! Login, register, or download the APK for real-time RTP live data and your chance at big wins. Play now! visit: phpfamous

-

[960]Experience the best lol646 online casino in the Philippines. Quick lol646 login, register, and lol646 app download to enjoy premium lol646 slot games today! Experience the best lol646 online casino in the Philippines! Enjoy a quick lol646 login and lol646 register process to play premium lol646 slot games. Get the lol646 app download today for a seamless mobile gaming experience and exclusive rewards! visit: lol646

-

[1461]7sjl Casino & Slot Philippines: Top Online Gaming with Easy 7sjl Login, Register, and App Download. Experience the best of 7sjl Casino & Slot Philippines. Enjoy a fast 7sjl login, easy 7sjl register, and seamless 7sjl app download. Play top 7sjl slot and casino games to win big today! visit: 7sjl

-

[6614]Otso Casino: The Best Legit GCash Online Casino and Slots in the Philippines. Experience Otso Casino, the premier online casino Philippines destination. As the best legit GCash online casino, we offer top-tier legit online slots Philippines and secure payouts. Visit otsocasino and use your otso casino login to start winning big at the most trusted gaming platform in the country! visit: otsocasino

-

[3650]sz777 Official: Best Philippines Online Slot Casino. Secure sz777 Login, Easy Register, and sz777 App Download for Big Wins. Join sz777 official: the top Philippines online casino. Easy sz777 register, secure sz777 login, and sz777 app download. Play sz777 slot games and win big today! visit: sz777

-

[7738]PHPub Online Casino Philippines: Easy Login, Register, and App Download for the Best Online Slots Experience. Join PHPub Online Casino Philippines! Enjoy easy PHPub login, fast register, and the PHPub app download. Play the best PHPub slots and PHPub casino online today for a premium gaming experience. visit: phpub

-

[7570]The Top Online Casino and Slot Games Destination in the Philippines visit: slotphlogin

-

[9673]Jiliplay Online Casino Philippines: Quick Login, Register & App Download for Top Jiliplay Slot Games Experience the best jiliplay slot games at Jiliplay Online Casino Philippines. Fast jiliplay login, easy register & jiliplay app download. Join the #1 jiliplay online casino today! visit: jiliplay

-

[9213]Jilicrown: Top Online Casino in Philippines – Easy Login, Register & App Download for Premium Slot Games Join Jilicrown, the top online casino in the Philippines. Experience easy Jilicrown login, fast register, and Jilicrown app download for premium Jilicrown slot games. Play now and win! visit: jilicrown

-

[105]KKJILI Casino Philippines: Easy Login, Register & App Download for Top Online Slots. Experience the ultimate gaming at KKJILI Casino Philippines! Quick kkjili login and register to play top-rated kkjili slot games. Get the kkjili app download for seamless mobile casino action and start winning today. visit: kkjili

-

[7678]JLSlot: Best Online Slot & Casino Games in the Philippines. Quick JLSlot Login, Register, and App Download for Top-Tier Gaming. Experience top-tier gaming at JLSlot, the #1 hub for online slot and casino games in the Philippines. Quick jlslot login, register, and jlslot app download. Join now! visit: jlslot

-

[8502]The Top Online Casino in the Philippines: Premium Slots and Fast GCash Gaming. visit: taya333

-

[6302]Philippines’ Top Online Casino: Easy sa88 Login, Register, & App Download. Play the Best sa88 Slot & Live Casino Games Today. Experience the best of sa88, the Philippines’ top online casino. Quick sa88 login & sa88 register. Get the sa88 download for mobile and play sa88 slot or live casino games today. Join sa88 casino now! visit: sa88

-

[6243]RG777 Online Casino: The Best Slot Gaming in the Philippines. Register or Login to enjoy top-tier RG777 Slots and get the official RG777 App Download for non-stop winning action. Experience the best gaming at RG777 Online Casino. Complete your RG777 register or RG777 login to play top RG777 slot games. Get the official RG777 app download for non-stop winning action in the Philippines! visit: rg777

-

If you’re looking for results, ket qua 9.net is where it’s at. Nice and simple design, easy to navigate. Definitely worth checking out! Peep it here: ket qua 9.net

-

Hey, I’ve been checking out rong.bach kim lately! Seems pretty interesting, and the interface is super smooth. Anyone else using it? rong.bach kim

-

Just found ‘roongf bachj kim’. I find it useful for checking the results! Try your luck on ‘roongf bachj kim’: roongf bachj kim.

-

p94fp2

-

30zhpu

-

r0f0y5

-

Whhy vviewers sill make usee oof too read newes papedrs when inn this technological gloe

alll iss avaulable on net?Alsoo visit mmy wweb ppage – roloxxx

-

Great article.

Also visit my web-site – cnhub.xyz

-

a6fav3

-

azqhol

-

5k602x

-

References:

Spielhallen online deutschland casino geld verdienen erfahrungen

-

v0060y

-

References:

Mcphillips street station casino jobszimbabwe.co.zw

-

cgt0ha

-

7uzbg8

-

wkt68f

-

ncfk9n

-

y9ikc3

-

l1razk

-

References:

Legiano Casino Spielen https://board-de.farmerama.com

-

References:

Legiano Casino Alternative https://utmagazine.ru

-

References:

KingMaker Casino Einzahlung mit Apple Pay https://hackthehill.io/silasnesmith1

-

References:

KingMaker einzahlung bonus code https://vnn.bio

-

References:

KingMaker Casino Einzahlung per Handyguthaben sbfpageing.com

-

References:

KingMaker Casino um Echtgeld spielen https://vnn.bio

-

References:

KingMaker 100 bonus einzahlung http://www.google.co.ao/url?sa=t&url=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Kingmaker Casino Bonus ohne Einzahlung http://toolbarqueries.google.com.mm/

-

References:

Kingmaker casino registrieren und einzahlen http://www.morrowind.ru/

-

References:

Kingmaker Casino https://m.kaskus.co.id/redirect?url=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker willkommensbonus images.google.co.mz

-

References:

KingMaker Casino Echtgeld Einzahlung https://34.pexeburay.com/index/d1?diff=0&utm_clickid=wmco4s4kogws8sss&aurl=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Legiano Casino Promo Code http://www.google.com.af/url?q=https://gardenwiki.site/wiki/Legiano_Casino_Tausende_Spiele_TopBoni_2025

-

References:

Kingmaker casino einzahlen bonus code http://cies.xrea.jp

-

References:

Legiano Casino VIP Programm m.en.acmedelavie.com

-

References:

Legiano Casino Download clients1.google.com.cy

-

References:

Legiano Casino Echtgeld http://wartank.ru

-

References:

KingMaker einzahlung sofort spielen clients1.google.com.pr

-

References:

KingMaker kreditkarte einzahlung http://images.google.co.in/url?sa=t&url=http://short.turtle.onl/kristinmazure0

-

References:

Kingmaker casino einzahlung deutschland http://toolbarqueries.google.ca

-

References:

Legiano Casino Auszahlung http://aintedles.yoo7.com

-

References:

KingMaker Casino Bonuscode Einzahlung http://clients1.google.co.ck

-

References:

KingMaker Casino 200% Einzahlungsbonus http://www.google.md/

-

References:

KingMaker 200 prozent bonus http://maps.google.co.ao

-

References:

Legiano Casino Auszahlungslimit http://clients1.google.sr/url?q=https://telegra.ph/Legiano-casino-login-konto-erstellen-wie-anmelden-06-07-2

-

References:

Legiano Casinio clients1.google.co.cr

-

References:

Legiano Casino Kundenservice http://k.scandwap.xtgem.com

-

References:

Hitnspin casino seriös http://maps.google.tk/url?q=https://link.avito.ru/go?to=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hit’n’spin casino 50 free spins http://www.google.com.bh

-

References:

Hitnspin kundensupport https://filelist.io/redir.php?http://wartank.ru/?channelId=30152&partnerUrl=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hitnspin casino seriös http://maps.google.iq/url?sa=t&url=https://n-doptor.nothi.gov.bd/password/reset?redirect=de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Monro Casino Auszahlung https://wikimapia.org

-

References:

Hit’n’spin casino 50 free spins http://nashi-progulki.ru/

-

References:

Hitnspin casino auszahlung erfahrungen m.66girls.tw

-

References:

Hit’n’spin casino erfahrungen http://wiki.neverlands.ru/api.php?action=https://www.haphong.edu.vn/profile/huijqborch31849/profile

-

References:

Hitnspin casino kundenbewertungen https://www.camtomycam.com/

-

References:

Hit n spin casino 25 euro code http://electrik.org/

-

References:

Hitnspin casino kostenlos spielen 128704.peta2.jp

-

References:

Hitnspin casino auszahlungsdauer electrik.org

-

References:

Hitnspin casino auszahlungsdauer https://www.musicalion.com/es/scores/notes/composition/get-languages-partial?baseUrl=https://link.epicalorie.shop/soilademaine92

-

References:

Hit n spin promo code anf.asso.fr

-

References:

Hitnspin app musicalion.com

-

References:

Hitnspin casino auszahlungsdauer http://forum.zidoo.tv/proxy.php?link=https://unim.ma/danaeshorter22

-

References:

Hitnspin casino http://forum-1tv.ru/

-

References:

Lollybet Echtgeld toolbarqueries.google.st

-

References:

Lollybet Casino Gutscheincode cse.google.ms

-

References:

Lollybet Bonus Code http://images.google.co.uk

-

References:

Lollybet Erfahrungen https://www.vs.uni-due.de/

-

References:

Lollybet Casino Live Dealer http://images.google.fr/

-

References:

Lollybet Freispiele maps.google.co.bw

-

References:

Lollybet Casino Treueprogramm google.ac

-

References:

Hitnspin casino bonus code http://cse.google.ba/url?sa=t&url=https://xtuml.org/author/cubanmonth04/

-

References:

Hitnspin casino slots http://clients1.google.ml/

-

References:

Hitnspin casino gewinne http://clients1.google.de/

-

References:

Hitnspin casino forum http://images.google.bj

-

References:

Hitnspin anmelden http://maps.google.co.jp

-

References:

Hit n spin casino no deposit bonus http://clients1.google.ae/url?q=https://www.news.lafontana.edu.co/profile/armstrongdzgkvist11079/profile

-

References:

Hitnspin casino betrug http://images.google.com.cy

-

References:

Hitnspin free spins http://clients1.google.tl/url?q=https://digitaltibetan.win/wiki/Post:Toledo_hollywood_casino

-

References:

Australian online pokies payid dev3.worldme.tv

-

References:

With blackjack and hookers https://adsmaz.com/profile/philomenalanse

-

References:

Western lotto 649 keeperexchange.org

-

References:

Wind creek casino atmore al https://academy.tatiosa.com/

-

References:

Online games play https://bookmyaccountant.co/

-

References:

Craps rules https://phantom.everburninglight.org/

-

References:

South point casino las vegas https://hirings.online/employer/beste-casinos-mit-schneller-auszahlung-2026-im-test

-

References:

Online roulette https://www.jobindustrie.ma/companies/casino-ohne-download-die-besten-instant-play-casinos-2026/

-

References:

Treasure island casino las vegas https://youthforkenya.com/employer/instant-wikipedia