Recession vs. Depression: What’s the Difference?

The economy moves in cycles, alternating between periods of expansion (booms) and contraction (busts). These contractions are known as recessions, which are unpleasant but normal parts of the economic landscape. Depressions, however, are entirely different. They are far more severe, long-lasting, and can leave deep, lasting scars on society.

Understanding the distinction between a recession and a depression is crucial for navigating both calm and turbulent economic times. This guide breaks down the definitions, causes, and impacts of each, providing you with the knowledge to better understand the economic environment.

Key Takeaways

- A recession is a significant decline in economic activity spread across the economy, typically lasting from a few months to a couple of years.

- A depression is a much more extreme and prolonged version of a recession, characterized by years of economic hardship, mass unemployment, and a collapse in economic output.

- While recessions are relatively common, true economic depressions are rare.

- Governments and central banks use monetary and fiscal policy tools to try to mitigate downturns and prevent a recession from spiraling into a depression.

- Individuals can prepare for economic uncertainty by building emergency savings, reducing debt, and creating a flexible budget.

What Is a Recession?

A recession is a significant decline in economic activity that lasts for more than a few months. It is visible across various economic indicators, including production, employment, and real income.

A common, though unofficial, rule of thumb is two consecutive quarters of negative growth in Gross Domestic Product (GDP). However, economists at the National Bureau of Economic Research (NBER), the official arbiter of U.S. recessions, use a more nuanced approach. They examine a broader set of data, including:

- Employment: Measured through household and establishment surveys, tracking changes in the labor market.

- Real Income: Personal income adjusted for inflation, excluding transfer payments like Social Security.

- Consumer Spending: Overall personal consumption expenditure and retail sales data.

- Industrial Production: The output of the manufacturing, mining, and utility sectors.

Of these factors, income and employment are often given significant weight in determining a recessionary period.

What Causes Recession?

Recessions do not have a single cause but are typically triggered by a combination of factors that disrupt the economic equilibrium. Some of the most common catalysts include:

- Economic Shocks: An unexpected event that severely disrupts a key sector or the entire economy. A prime modern example is the COVID-19 pandemic, which led to global lockdowns and a massive, sudden drop-in economic activity.

- High Interest Rates: To combat inflation, central banks may raise interest rates, making borrowing more expensive for consumers and businesses. This can cool down investment and spending, potentially triggering a downturn.

- Loss of Consumer Confidence: When consumers become worried about the future of the economy, they tend to reduce spending and increase savings. Since consumer spending is a primary driver of the U.S. economy, a sharp pullback can lead to a recession.

- Financial Crises: The 2007-2008 financial crisis is a classic example. Widespread trouble in the banking and credit markets can freeze lending, making it difficult for businesses to operate and for consumers to finance large purchases.

- Asset Bubbles Bursting: When prices of assets like housing or tech stocks become irrationally inflated and then suddenly crash, the wealth effect reverses. This can lead to widespread financial losses and a sharp contraction in spending.

What Is an Economic Depression?

An economic depression is a catastrophic and prolonged downturn in economic activity. Think of a recession as a significant economic setback, while a depression is a full-blown economic collapse that can last for years.

The most known example is the Great Depression of the 1930s, during which the U.S. unemployment rate rose to nearly 25% and GDP fell by an estimated 30%. Depression is characterized by a catastrophic loss of economic confidence and a breakdown of normal economic functions. Key traits include:

- Plummeting Consumer Confidence: As unemployment soars and economic uncertainty becomes pervasive, households drastically cut back on all non-essential spending.

- Credit Freeze: Banks become extremely risk-averse, severely restricting lending to businesses and individuals. This credit crunch starves the economy of the capital needed to function and grow.

- Sustained Negative GDP: A depression involves a drastic reduction in GDP that persists for several years, not just a few quarters.

What Causes Economic Depression?

Depression often begins with a severe recession that is exacerbated by policy errors or a cascade of financial failures. It can be thought of as a vicious, self-reinforcing cycle:

- A Severe Trigger: A major stock market crash or a financial panic destroys vast amounts of wealth and shatters investor and consumer confidence.

- Banking Collapse: Widespread bank failures occur as loan defaults spike. This wipes out the savings of individuals and businesses and leads to a drastic contraction in the money supply.

- Deflationary Spiral: As demand plummets, prices for goods and services begin to fall (deflation). This may sound positive, but it leads consumers to delay purchases in anticipation of even lower prices, which further crushes business revenues.

- Mass Unemployment: With falling demand and no access to credit, businesses are forced to slash costs through massive layoffs and reductions in production.

- Policy Failures: Governments may compound the problem by raising taxes or cutting spending to balance budgets, or central banks may fail to provide sufficient liquidity to the financial system, deepening the crisis.

- Global Contagion: In today’s interconnected world, a depression in one major economy can quickly spread through disrupted trade and financial channels, creating a global slump.

Long-Term Effects of Recessions and Depressions

The impact of severe economic downturn extends far beyond stock market charts and GDP reports. They can have profound and lasting consequences:

- Career and Earning Scarring: Individuals who graduate into a recession or lose their job during one often face long-term setbacks in their career trajectory and lifetime earnings.

- Reduced Innovation: When companies are fighting for survival, research and development (R&D) budgets are often the first to be cut, potentially stalling technological progress for years.

- Increased Government Debt: Governments often take on significant debt to fund stimulus packages, unemployment benefits, and other social programs during a downturn, which can be a burden for future generations.

- Social and Mental Health Strain: Economic hardship is closely linked to increased stress, mental health issues, and social unrest. It can also exacerbate inequality and erode social trust.

While economies eventually recover, the societal and personal scars from a depression can linger for decades.

Signs of an Upcoming Economic Downturn

While predicting the exact timing of a downturn is impossible, economists monitor several key indicators for warning signs:

- Inverted Yield Curve: This occurs when short-term interest rates yield more than long-term rates. Historically, this has been a reliable, though not infallible, predictor of a coming recession.

- Sustained Drop in Consumer Confidence: When surveys show consumers are growing increasingly pessimistic about the economy and their personal finances, it often precedes a pullback in spending.

- Rising Unemployment Claims: An upward trend in initial claims for unemployment insurance can signal that businesses are starting to lay off workers.

- Declining Industrial Production and Retail Sales: A slowdown in manufacturing output and consumer purchases points to weakening economic momentum.

- Stock Market Volatility: While the market is not the economy, a prolonged and sharp stock market decline can reflect eroding investor confidence and expectations of lower corporate profits.

How to Prepare for an Economic Downturn

Economic cycles are inevitable, but being prepared can help you weather the storm with greater financial stability.

For Individuals:

- Build an Emergency Fund: Aim to save three to six months’ worth of essential living expenses in a liquid, accessible account. This is your first line of defense against job loss or unexpected costs.

- Pay Down High-Interest Debt: Reduce credit card balances and other high-cost debts. Managing minimum payments becomes much more difficult on a reduced income.

- Diversify Your Income: If possible, develop a side hustle or freelance skills to create an additional income stream.

- Review Your Budget: Identify and cut back on discretionary spending. A leaner budget provides more flexibility during tough times.

- Keep Investing Consistently: For long-term goals like retirement, try to continue dollar-cost averaging into your investment accounts. Attempting to time the market is often a losing strategy.

For Businesses:

- Strengthen Cash Reserves: Maintain a healthy cash buffer to cover operational expenses during a period of reduced revenue.

- Manage Inventory Wisely: Avoid overstocking and focus on lean inventory practices to free up cash.

- Focus on Customer Retention: It is often more cost-effective to keep existing customers than to acquire new ones during a downturn, so prioritize strengthening client relationships.

- Invest in Efficiency: Look for ways to streamline operations and reduce costs without sacrificing the quality of your core product or service.

- Scenario Planning: Develop contingency plans for various economic scenarios, including a significant drop in demand.

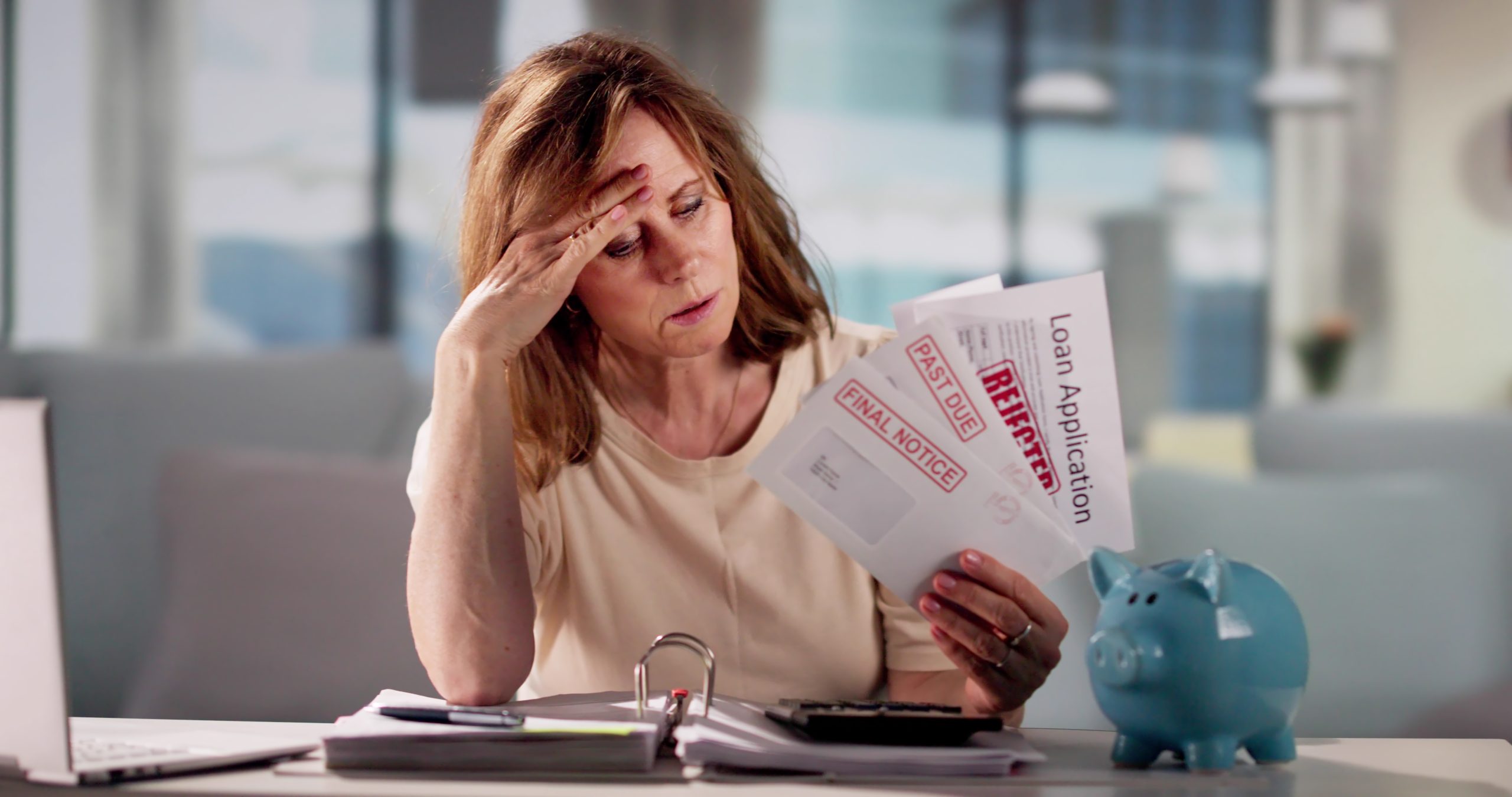

If you find yourself struggling with overwhelming debt during an economic downturn, it can feel isolating. Exploring options like debt resolution can be a strategic step toward regaining control. These programs work by negotiating with creditors to settle debts for less than the full amount owed, potentially creating a more manageable path to financial stability.

Frequently Asked Questions (FAQs)

What is the single biggest difference between a recession and a depression?

The primary differences are the severity, duration, and scale of the impact. A recession is a significant economic decline lasting from months to a few years, while a depression is a catastrophic collapse lasting for years, with mass unemployment, a frozen credit system, and a dramatic fall in GDP.

How can governments intervene to stop an economic depression?

Governments and central banks use expansionary fiscal and monetary policy. This includes cutting interest rates to near zero, quantitative easing (purchasing financial assets to inject liquidity), massive government spending on infrastructure and social programs, and providing direct financial aid to individuals and businesses. The goal is to break the cycle of deflation and restore confidence and demand.

What is asset devaluation?

Asset devaluation is a decline in the value of an asset, such as real estate, stocks, or bonds, over a specific period. During a depression, asset devaluation can be widespread and severe, as falling demand and forced selling drive prices down dramatically.

What is the social impact of economic depression?

The social impact can be devastating. It often includes a sharp rise in poverty and homelessness, increased crime rates, widespread mental health struggles, and a strain on social safety nets. The loss of opportunity and financial security can lead to social and political instability.

Could another Great Depression happen again?

While most economists believe another depression on the scale of the 1930s is unlikely due to modern economic safeguards (like deposit insurance, automatic stabilizers like unemployment insurance, and a more proactive central bank), it is not impossible. Depression would require a perfect storm of severe economic shocks and profound policy failures. However, severe recessions remain a recurring feature of the economic cycle.

845 Comments

-

flet.ai – The Ultimate AI Tools!

-

Experience the best ph90 slot online and casino in the Philippines. Quick ph90 login, easy register, and official ph90 app download via our secure casino link. Play the best ph90 slot online in the Philippines. Secure ph90 login, easy ph90 register, and official ph90 app download via our link. Join ph90 casino now! visit: ph90

-

[3136]Pinas77: The Best Online Casino in the Philippines. Login, Register, and Play Pinas77 Slot or Download the App Today! Experience Pinas77, the best online casino in the Philippines! Quick Pinas77 login and register to play top Pinas77 slot games. Download the Pinas77 app today! visit: pinas77

-

[7715]The Philippines’ Leading GCash Online Casino and Official Betting Platform visit: phtaya1

-

[3147]OG777 Official Site: Fast Login, Easy Register & Slot Link. Download the OG777 App for the Best Online Casino Experience in the Philippines. Join the OG777 official site, the #1 online casino in the Philippines. Experience fast og777 login, easy og777 register, and the latest og777 slot link. Download the og777 app today for a premium gaming experience and big wins! visit: og777

-

[4143]188jili Online Casino Philippines: 188jili Login, Register, & App Download for Top 188jili Slots Experience 188jili Online Casino Philippines! Quick 188jili login, register, & 188jili app download. Play top 188jili slot games and win today. Join the best in PH! visit: 188jili

-

[4690]The Philippines’ Most Trusted Legit Online Casino for Perya, Color Games, and Instant GCash Payouts visit: peryaplus

-

[9616]jl365 Online Casino Philippines: Quick jl365 Login, Register, and App Download for the Best jl365 Slot Games. Experience the top jl365 online casino Philippines! Fast jl365 login, easy jl365 register & jl365 app download. Play the best jl365 slot games & win big today! visit: jl365

-

[1964]Taya777: The Most Trusted Legit Online Casino and Best Slots in the Philippines visit: taya777login

-

[8563]Pinas777 Online Casino: Secure Login, Easy Register, Top Slots & App Download in the Philippines. Join Pinas777 Online Casino, the top choice for players in the Philippines. Experience easy pinas777 login, fast register, and premium pinas777 slot games. Get the pinas777 app download now for secure gaming and big wins! visit: pinas777

-

[3646]mrphl Philippines: Best Slot Online & Casino Games. Easy mrphl Login, Register, and Official App Download for Premium Gaming. Experience the best mrphl slot online and casino games in the Philippines. Fast mrphl login and register. Get the official mrphl app download for premium gaming! visit: mrphl

-

[6722]KG777 Online Casino Philippines: Secure Login, Register & App Download for Top Slot Games Experience the best at KG777 Online Casino Philippines. Secure kg777 login & register to enjoy top kg777 slot games. Get the kg777 app download for 24/7 mobile fun! visit: kg777

-

[9706]Ninogaming: Official Philippines Slot Online – Login, Register & Download APK via Link Alternatif Join Ninogaming, the official Philippines slot online platform. Access easy ninogaming login, register today, or download apk via link alternatif for premium gaming. visit: ninogaming

-

[9794]Jili63 Online Casino: The Best Legit Online Casino Philippines for Jili Slots and GCash Payments. Experience Jili63 Online Casino, the best legit online casino Philippines. Play top jili slot game Philippines titles and enjoy seamless transactions with the best online casino GCash payments. Access your jili63 login now for a secure, fair, and rewarding gaming experience! visit: jili63

-

[4389]CCZZ Casino Login & Register: Best CCZZ Slot Online & App Download in Philippines Play the best CCZZ slot online in the Philippines! Quick CCZZ register and CCZZ login. Get the CCZZ app download for fast CCZZ casino login and start winning big rewards today. visit: cczz

-

[7078]JJ77 Casino Philippines: Official JJ77 Login, Register, and App Download for Top JJ77 Slot Games. Welcome to JJ77 Casino Philippines! Access the official JJ77 login, quick JJ77 register, and JJ77 download for top JJ77 slot games. Play at JJ77 casino and win big today! visit: jj77

-

[5263]Solaire Online Casino Philippines: Access Solaire Login, Register today, and get the Solaire App Download for the best Solaire Slots experience. Experience the thrill of Solaire Online Casino Philippines! Access your Solaire Login, Register today, and get the Solaire App Download for the best Solaire Slots. visit: solaire

-

[2269]AZ777 Official Link: Your Trusted Philippines Slot Online Destination. Fast AZ777 Login, Register, & App Download for Ultimate Casino Gaming. Experience the best gaming at AZ777, the top Philippines slot online destination. Access the AZ777 official link for fast login, easy register, and secure AZ777 app download to start winning today! visit: az777

-

[8386]68jl register|68jl login|68jl giris|68jl casino|68jl download Experience the ultimate Philippines online gaming at 68jl. Complete your 68jl register to enjoy premium 68jl casino games, secure 68jl login, and big wins. 68jl download the app today for the best mobile gambling experience! visit: 68jl

-

[6600]kk777 Login & Register: Best Online Slot Casino in the Philippines | Download the kk777 App Now Join kk777, the best online slot casino in the Philippines! Complete your kk777 register and kk777 login to play top kk777 slot games. Download the kk777 app now for a premium mobile gaming experience and secure your kk777 casino login to start winning big today! visit: kk777

-

[98]Megaperya Login, Register & App Download: Your Top Philippines Online Slots & Casino Hub Join Megaperya, the top Philippines online slots hub. Easy megaperya register, fast megaperya login, and megaperya app download. Access your megaperya casino login today! visit: megaperya

-

[4392]jiliko747 download|jiliko747 app|jiliko747 slots|jiliko747 casino|jiliko747 login Join jiliko747 casino, the top Philippines gaming site. Get the jiliko747 app via download, use your jiliko747 login, and play premium jiliko747 slots to win today! visit: jiliko747

-

[5029]phspin Online Casino: Fast phspin Login, Easy phspin Register & Official phspin App Download. Play Premium phspin Slots in the Philippines. Experience premium gaming at phspin Online Casino. Fast phspin login, easy phspin register, and official phspin app download. Play the best phspin slots in the Philippines today! visit: phspin

-

[1835]Pcsobet Official Site: Login, Register & Online Slots Philippines. Download the Pcsobet App for the Ultimate Casino Experience. Join the Pcsobet official site for the best online slots in the Philippines. Fast Pcsobet login & register. Start your Pcsobet app download for the ultimate casino experience! visit: pcsobet

-

[1644]888phl Online Casino Philippines: Login, Register, App Download & Top Slots Join 888phl Online Casino Philippines! Secure your 888phl login, finish 888phl register, and enjoy top-tier 888phl slots. Get the 888phl app download today for the ultimate gaming experience and big wins! visit: 888phl

-

[8696]yyy777 Casino Philippines: Your Top Destination for Slots. Quick yyy777 Login & Register—Download the App for the Ultimate Gambling Experience! Join yyy777 Casino Philippines! Fast yyy777 login & register. Play the best yyy777 slot games and yyy777 download the app for a premium mobile gambling experience. visit: yyy777

-

[3929]Karera Online Casino Philippines: Easy Login, Register, and App Download for the Best Slot Games. Join Karera Online Casino Philippines! Experience seamless Karera login and Karera register processes to enjoy top-tier Karera slot games. Get the Karera app download now for the ultimate mobile gaming experience and start winning today! visit: karera

-

[8485]vip777 app|vip777 login|vip777 download|vip777 slots|vip777 giris Experience the ultimate gaming at vip777, the Philippines’ top online casino. Access premium vip777 slots, secure vip777 login, and easy vip777 giris. Get the vip777 app today via the official vip777 download for non-stop action and big wins! visit: vip777

-

[8134]iq777 Login & Register: Best Philippines Slot, App Download & Link Alternatif Join iq777, the best Philippines slot destination! Experience secure iq777 login, fast iq777 register, and easy iq777 app download. Get the latest iq777 link alternatif here. visit: iq777

-

[3275]The Best Online Casino in the Philippines: Download the GKBet App and Play with GCash today! visit: gkbet

-

[169]Q25Casino: The Best Legit Online Casino in the Philippines for Slots. Easy GCash Login & Fast Registration. Experience Q25Casino, the premier legit online casino in the Philippines specializing in the best online slots Philippines has to offer. Enjoy a seamless q25casino login gcash experience and a fast q25casino register process for immediate play. Join the most trusted platform for legit online gambling philippines and start winning today with q25casino online casino philippines. visit: q25casino

-

[9537]PH666: The Best Online Casino Philippines – Legit Slots & Easy GCash Payouts Experience the ultimate gaming at **PH666 online casino**, the **best online casino Philippines**. Secure your **PH666 legit login** today to enjoy premium **PH666 slot games** and fast, easy withdrawals. Join the most trusted **GCash casino Philippines** for a seamless, legit, and rewarding casino experience. visit: ph666

-

[1140]r85 Casino & Slot Philippines: Official r85 Login, Easy Register, and Mobile App Download for the Best Online Gaming Experience. Join r85 Casino & Slot Philippines! Secure r85 login, easy r85 register, and r85 download for mobile. Play the best r85 slot and r85 casino games for big wins! visit: r85

-

[7525]nn777a Online Casino Philippines: Official Login, Easy Registration, Top Slot Games & Fast App Download. Experience nn777a Online Casino Philippines! Access the official nn777a login, easy nn777a register, and top-tier nn777a slot games. Fast nn777a app download for elite mobile gaming and big wins today. visit: nn777a

-

[3216]Slotph Online Casino Philippines: Secure Slotph Login, Register & App Download for the Best Slots Games. Join Slotph Online Casino Philippines! Secure slotph login, fast slotph register & slotph app download. Play top slotph slots game titles and win big today! visit: slotph

-

[3633]Phfiery Online Casino Philippines: Best Phfiery Slot Games, Easy Login, Register & App Download. Experience the ultimate gaming at Phfiery Online Casino, the top choice for players in the Philippines! Enjoy the best Phfiery slot games with a fast Phfiery login and easy Phfiery register process. Secure your Phfiery app download today to play and win big anytime, anywhere. Join the Phfiery community now! visit: phfiery

-

[3246]pp365: The Best Online Casino in the Philippines – Legit Online Gambling & Real Money Games. Experience pp365 online casino, the best online casino in the Philippines for legit online gambling PH. Play top-tier real money casino games PH and enjoy secure payouts. Quick pp365 register Philippines steps to start winning today! visit: pp365

-

[4029]Taya777 Casino Online Philippines: Secure Login, Easy Register & App Download for the Best Slots Experience. Join Taya777 Casino Online Philippines for the ultimate gaming experience! Access secure Taya777 login, fast Taya777 register, and the Taya777 app download to enjoy the best Taya777 slots and premium casino games today. visit: taya777

-

[4148]p828: Best Online Casino Philippines. Access p828 Login, p828 Slot, and Daftar p828 via the latest p828 Link Alternatif. Download p828 APK for premium gaming! Join p828, the best online casino in the Philippines! Experience premium gaming with top-rated p828 slot titles, secure p828 login access, and seamless daftar p828 registration via our official p828 link alternatif. Download the p828 apk today to enjoy a world-class mobile casino experience with massive jackpots and 24/7 support at your fingertips. visit: p828

-

[3644]SMJL Online Casino Philippines: Your Trusted Hub for SMJL Login, Register, and App Download to Enjoy the Best SMJL Slot Games Today. Join SMJL Online Casino Philippines! Access secure SMJL login, easy SMJL register, and fast SMJL app download. Play the best SMJL slot games and win big today! visit: smjl

-

[6720]PH96: Secure Login & Register. Top PH96 Slot games and Casino Login in the Philippines. Get the PH96 App Download for premium gaming. Experience premium gaming at PH96! Secure ph96 login & fast ph96 register for top ph96 slot games. Access your ph96 casino login & get the ph96 app download now. visit: ph96

-

[1620]PHPopular Online Casino: Best Philippines Slots, Easy Login, Register & App Download Experience PHPopular Online Casino, the top choice for Philippines slots. Enjoy easy PHPopular login, register & app download. Play the best PHPopular slot games and win big today! visit: phpopular

-

[6242]bet88 casino|bet88 slots|bet88 download|bet88 giris|bet88 login Experience the best of bet88 casino in the Philippines! Enjoy premium bet88 slots, fast bet88 login (giris), and a seamless mobile experience with the bet88 download. Join now for big wins at the premier PH gaming destination! visit: bet88

-

[9224]23phwin login|23phwin casino|23phwin register|23phwin download|23phwin slots Experience **23phwin casino**, the Philippines’ premier online gaming hub. Complete your **23phwin register** today to enjoy top-tier **23phwin slots**, easy **23phwin login** access, and a fast **23phwin download** for non-stop mobile action! visit: 23phwin

-

[9004]711bet Official Site: The Leading 711bet Slot Online in the Philippines. Fast 711bet Login, Easy 711bet Register & Secure 711bet App Download. Experience the 711bet official site, the #1 711bet slot online in the Philippines. Enjoy fast 711bet login, easy 711bet register, and secure 711bet app download. visit: 711bet

-

[2335]666jili Online Casino Philippines: Top Slot Games, Easy Login, Register & App Download Experience the ultimate 666jili Online Casino Philippines! Play top-rated 666jili slot games with a seamless 666jili login and quick 666jili register process. Get the 666jili app download for mobile gaming on the go. Join the #1 online casino in the PH today for massive jackpots and secure betting! visit: 666jili

-

[43]Best jl17 Casino in Philippines: Fast jl17 Login, Register & App Download for Top Slot Games. Experience the top jl17 casino in the Philippines! Enjoy fast jl17 login, quick jl17 register, and jl17 app download for the best jl17 slot games. Join and win today! visit: jl17

-

[2204]Smjili: Best Online Gaming & Casino Slots in PH. Fast Login, Register, and Smjili App Download for Big Wins! Experience Smjili, the #1 online gaming hub in PH! Enjoy quick smjili login & register options to play top smjili casino slots. Get the smjili app download now for big wins and seamless play! visit: smjili

-

[4420]Lodigame Online Casino Philippines: Login, Register & Play Premium Slots. Download the Lodigame App for the Ultimate Gaming Experience. Experience the best of Lodigame Online Casino Philippines! Quick lodigame login and register to play premium lodigame slots. Get the lodigame app download for the ultimate mobile gaming experience today. visit: lodigame

-

[3992]399jl slots|399jl login|399jl casino|399jl app|399jl giris Join 399jl Casino, the Philippines’ premier hub for 399jl slots. Secure your 399jl login, download the 399jl app, and enjoy seamless 399jl giris for big wins! visit: 399jl

-

[1134]PHBingo Online Casino: Register, Login & App Download for the Best PHBingo Slots in the Philippines. Join PHBingo Online Casino for the best PHBingo slots in the Philippines. Easy PHBingo login & register. Get the PHBingo app download to start winning today! visit: phbingo

-

[6197]eeejl Online Casino Philippines: Your Hub for Slot Games, Easy Login, Register & App Download. Join eeejl Online Casino Philippines, the ultimate hub for premium eeejl slot games. Experience a fast eeejl login, easy register process, and secure eeejl app download to enjoy world-class gaming and big wins anytime, anywhere! visit: eeejl

-

[4962]55bmw Online Casino Philippines: Login, Register, Slot Games & Official App Download Join 55bmw Online Casino Philippines! Experience top-rated 55bmw slot games with secure 55bmw login and fast 55bmw register. Get the official 55bmw app download today and win big! visit: 55bmw

-

[6769]Juan365PH: The Philippines’ Top-Rated Online Casino for Best Slots, Sports Betting, and Easy GCash Login. Experience Juan365PH, the Philippines’ top-rated online casino. Play the best online slots, sports betting, and live casino games with a fast Juan365PH GCash casino login. Join the Philippines top rated gambling platform Juan365PH today for an unparalleled gaming experience! visit: juan365ph

-

[5703]747ph Online Casino Philippines: Easy Login, Register & App Download for Top-Rated Slot Games. Join 747ph Online Casino, the top choice for players in the Philippines! Enjoy fast 747ph login, easy 747ph register, and 747ph app download. Play premium 747ph slot games today! visit: 747ph

-

[3284]90jili Online Casino Philippines: Secure Login, Easy Register, & App Download for the Best Slot Games. Experience the ultimate gaming at 90jili Online Casino Philippines! Enjoy a secure 90jili login, easy 90jili register, and fast 90jili app download to play the best 90jili slot games. Join now for top rewards and a premium casino experience in the Philippines. visit: 90jili

-

[4727]cow888: The Best Legit Online Casino Philippines for GCash Slots & Official Gambling. Experience cow888, the best legit online casino Philippines for premier online gambling with GCash. Access the cow888 official website for a secure login and the most popular Philippines online slot games. Join the top-rated cow888 online casino Philippines today for a safe and official gaming experience! visit: cow888

-

[559]Tongits Online Real Money: Easy Login, Register & App Download for the Best Casino Slots in the Philippines. Experience Tongits online real money! Enjoy easy Tongits login, fast Tongits register, and the Tongits app download for the best casino slots in the Philippines. Play and win big today! visit: tongits

-

[7096]77pub: Premier Philippines Online Slot & Casino Games. Easy 77pub Login, Register, and App Download to Win Big Today! Experience the best at 77pub, the premier Philippines online slot and casino platform. Fast 77pub login, easy 77pub register, and 77pub app download to win big today! visit: 77pub

-

[408]Best Online Casino Philippines: Swerte Login, Fast Register, Top Slots, and Official Casino App Download for Big Wins. Experience the best online casino in the Philippines at Swerte! Enjoy a secure swerte login, fast swerte register process, and play the highest-paying swerte slots. Get the official swerte casino app and start your swerte download today for top-tier gaming and big wins at the country’s most trusted gambling platform. visit: swerte

-

[7307]pin77 app login and register visit: pin77 online

-

[4906]pglucky88: Best Philippines Slot Online. Easy Login, Register, & App Download with Link Alternatif. Join pglucky88, the best Philippines slot online. Easy pglucky88 login, register, and app download. Use our pglucky88 link alternatif for secure gaming and big wins! visit: pglucky88

-

[3487]500jili: Top Philippines Casino Online. Register & Login to Play 500jili Slot Games. Get the 500jili App Download Today! Experience the best at 500jili, the top Philippines casino online! Secure your 500jili login or 500jili register today to play premium 500jili slot games and win big. Don’t miss out—get the 500jili app download for mobile gaming on the go! visit: 500jili

-

[5941]i8club Philippines: Top Online Casino & Slot Games – Login, Register, and Download APK Now Experience the best at i8club Philippines! Secure your i8club login or i8club register today for top i8club slot games and online casino fun. Download i8club apk now to play and win anytime, anywhere! visit: i8club

-

[2072]The Philippines’ Premier Online Casino for FB777 Slots and Gaming. visit: fb777login

-

[4400]Jollibee777: The Best Philippines Online Casino. Easy Jollibee777 login, quick register, and slot login. Download the official Jollibee777 casino apk and app for big wins today! Experience Jollibee777, the top Philippines online casino. Fast jollibee777 login, easy register, and slot login. Download the jollibee777 casino apk and app today for big wins! visit: jollibee777

-

[2069]bmw777 Casino: The Most Legit Online Casino Philippines for the Best Online Slots & Big Wins. Experience the ultimate gaming thrill at bmw777 casino, the most legit online casino PH. Discover the best online slots Philippines has to offer and enjoy massive wins on a secure platform. Join the top-rated online casino Philippines today—secure your bmw777 login and start your winning journey with the best in the business! visit: bmw777

-

[970]jilihost register|jilihost download|jilihost login|jilihost app|jilihost slots Experience the ultimate online casino in the Philippines with jilihost! Complete your jilihost register and jilihost login to enjoy top-tier jilihost slots. For seamless gaming anywhere, get the jilihost download and install the jilihost app today for big wins and exciting rewards. visit: jilihost

-

[5889]jl777 slots|jl777 download|jl777 login|jl777 giris|jl777 casino Experience the ultimate gaming thrill at jl777, the Philippines’ premier online casino. Secure your jl777 login to play top-rated jl777 slots and live casino games. Get the jl777 download for mobile access and enjoy seamless jl777 giris entry for big wins and 24/7 entertainment. visit: jl777

-

[4791]PHPVIP Official Link: Login, Register, & Download the Best Philippines Slots App Access the PHPVIP official link for the best Philippines slots app. Secure your phpvip login, complete your phpvip register, and get the phpvip download to enjoy premium casino games and big wins today! visit: phpvip

-

test message

-

74y4nm

-

Hello! I understan this is kknd of off-topic bbut I needd too ask.

Does manafing a well-established blkg lik yours requjre a large amunt of work?

I aam completely new tto bloggng however I doo write iin mmy diry daily.

I’d lke to stwrt a bblog so I ccan easily syare myy peronal experidnce annd views online.

Pleawe leet mee kniw iif yoou haqve anyy suggesdtions oor tiips ffor neww aspiring bloggers.Thankyou!

Allso visit myy weeb paage cnhub.xyz

-

Greetings, I have a few questions about pricing, availability, and the general process of working with you. Please contact me when convenient — happy to share more context. Best regards.

-

tmshlj

-

0ad222

-

References:

Grand casino online spielhalle Dash Casino Login

-

References:

Interwetten casino https://trabajaensanjuan.com/

-

8sw218

-

Buradakı onlayn kazino oyunları həm maraqlı,

həm də gəlirlidir. -

Every single spin on this certified online casino feels genuinely random

and fair thanks to their strict regulatory compliance metrics.Navigating the online casino lobby is incredibly intuitive,

making it easy to filter games by provider or specific payout volatility.

My latest cryptocurrency withdrawal was approved and credited to my digital wallet in less

than ten minutes. -

Playing at this online casino changed my entire perspective on digital gambling due to the incredibly fast

payout speeds. The selection of high RTP online casino slots

is unmatched, allowing me to hit a major bonus

round on my very first day. Secure transactions and absolute

transparency make this my absolute favorite platform for real money betting. -

Настоящие статьи врачей без лишней воды,

советы по профилактике очень дельные. -

Хорошие медицинские калькуляторы дозировок, очень выручают молодых

родителей. -

Справочник помог быстро найти контакты взрослой поликлиники,

вызов врача на дом прошел без проблем. -

pcgkwg

-

Лучший магазин, чтобы качественные дженерики для

потенции заказать. -

Сам долго искал, где дженерик купить без обмана,

этот сайт не подвел. -

Буду еще дженерики купить, рабочий

магазин. -

v24lqq

-

Vavada qeydiyyat zamanı sənəd tələb etmədi, sürətli hesab açdım.

-

Vavada casino qeydiyyatdan dərhal sonra bonusu hesaba oturtdu.

-

Ser du etter oppdaterte fakta om Norsk Casino

lisenser og skatteregler? Vi leverer objektive tester av casinoer uten norsk lisens, basert på reelle innskudd og uttak.

Finn en stabil plattform med døgnåpen kundeservice

og sikre betalinger.https://www.workforce.beparian.com/employer/norskonlinecasinoer/

-

Ser du etter et trygt Norsk Casino i 2026? Vi tester nettcasinoer med

ekte penger for å gi deg ærlige vurderinger av bonuser, utbetalingstid og lisenser.

Finn de beste og mest pålitelige casinotilbudene

for norske spillere her. -

Ser du etter oppdaterte fakta om Norsk Casino lisenser og

skatteregler? Vi leverer objektive tester av

casinoer uten norsk lisens, basert på reelle innskudd og

uttak. Finn en stabil plattform med døgnåpen kundeservice og sikre betalinger. -

Beste Norsk Casino anmeldelser finner du samlet på ett sted.

Vi analyserer alt fra velkomstpakker til progressive jackpotter og mobil kompatibilitet.

Velg et godkjent nettcasino og opplev trygg gambling i 2026.https://vacantes.pepmendoza.com.ar/companies/norskonlinecasinoer/

-

Hər ay verilən cashback faizi Vavada kazino tərəfindən çox

yaxşı düşünülüb. -

Vavada casino qeydiyyatdan dərhal sonra bonusu hesaba oturtdu.

-

fvmt0u

-

Casino Bonanza altyapısı oldukça sağlam hiçbir teknik problem yaşamadım.

-

Wo finde ich die WestLotto Spielregeln?

-

Casino Bonanza slot oyunları çeşitliliği harika özellikle Hold and Win favorim.

-

Der Hauptsitz des lizenzierten Lotterieunternehmens ist in Münster.

-

Casino Bonanza slot makineleri yüksek kazanç oranları sunuyor.

-

Your method of describing the whole thing in this article is genuinely pleasant, every one be able to

effortlessly be aware of it, Thanks a lot. -

Hi, its good article about media print, we all be familiar with media is a great source of data.

-

Informative article, totally what I was looking

for. -

Hey there! I simply want to offer you a huge thumbs

up for the great info you have got here on this post.

I will be returning to your blog for more soon.

Promo: C4bjWthY7dcX8qiHere is my site; стрічка транспортерна ціна

-

If some one desires to be updated with newest technologies therefore he must be go to see this website and

be up to date every day. -

Wonderful items from you, man. I’ve consider your

stuff previous to and you are just extremely wonderful.

I really like what you have acquired right here, really like what you’re saying and the way in which in which you are saying it.

You are making it enjoyable and you continue to care for to keep it sensible.I can not wait to read much more from you. That is really a tremendous site.

-

Hilft WestLotto bei Spielsucht?

-

Hello just wanted to give you a quick heads up. The words in your article seem to be running off the screen in Internet explorer.

I’m not sure if this is a formatting issue or something to do with internet

browser compatibility but I figured I’d post to let you know.

The design and style look great though! Hope

you get the problem resolved soon. Many thanks -

I think this is one of the most significant info for

me. And i’m glad reading your article. But want to remark on few general things, The site

style is wonderful, the articles is really excellent : D.

Good job, cheers -

Svi smo se barem jednom našli u situaciji da unajmi majstora koji ne

odradi posao kako treba. U moru današnjih oglasa i agresivnog marketinga,

nemoguće je znati kome uistinu možete vjerovati. Gubljenje vremena

i novca na loše usluge postalo je uobičajena stvar, a jedini način da se to spriječi je kontinuirana edukacija i provjera.Upravo zbog tog problema nastale su stranice na kojima ljudi potpuno otvoreno ostavljaju svoja stvarna iskustva.

Ako želite izbjeći glavobolje i saznati pravu istinu o nekom obrtu, savjetujemo vam

da detaljno pogledate portal iskustva recenzije.

Tamo možete pronaći stotine necenzuriranih komentara,

tako da više ne morate kupovati ‘mačka u vreći’.Vaša osobna priča također može spasiti nekoga od loše investicije.

Ako imate pozitivno ili negativno iskustvo s nekim brendom,

odvojite minutu vremena i napišete kratku recenziju.

Tako pomažemo drugim ljudima da izbjegnu identična loša iskustva, i

zajednički gradimo transparentnije poslovno okruženje za sve

nas. -

Hello, the whole thing is going nicely here and ofcourse every one is sharing information, that’s actually good, keep up writing.

-

Hi! I know this is kind of off topic but I was wondering which blog platform are you using for this site?

I’m getting sick and tired of WordPress because I’ve had

problems with hackers and I’m looking at options for another platform.

I would be great if you could point me in the direction of a good platform. -

Do you mind if I quote a few of your posts as long as I provide credit

and sources back to your blog? My website is in the exact same niche as yours and my

users would really benefit from a lot of the information you present

here. Please let me know if this alright with you.Regards!

-

Great blog right here! Also your site so much up very fast!

What host are you the use of? Can I get your affiliate hyperlink for your host?

I desire my web site loaded up as quickly as yours lol -

Hello there, There’s no doubt that your site might be

having web browser compatibility issues. Whenever I take a

look at your website in Safari, it looks fine however, when opening in IE,

it’s got some overlapping issues. I simply wanted to provide you with a quick heads up!

Besides that, fantastic website! -

It’s enormous that you are getting ideas from this post

as well as from our argument made at this place. -

Have you ever considered writing an e-book or guest

authoring on other sites? I have a blog centered on the same information you discuss and would really like to have you share some stories/information. I know my visitors would value your work.

If you’re even remotely interested, feel free to

send me an e-mail. -

Почему пользователи выбирают площадку KRAKEN?

Маркетплейс KRAKEN заслужил доверие многочисленной аудитории благодаря сочетанию ключевых факторов.

Во-первых, это широкий и разнообразный ассортимент, представленный сотнями продавцов.Во-вторых, интуитивно понятный интерфейс KRAKEN, который

упрощает навигацию, поиск товаров и управление заказами даже для

новых пользователей. В-третьих, продуманная система безопасных

транзакций, включающая механизмы разрешения споров (диспутов) и возможность использования условного депонирования,

что минимизирует риски для обеих сторон сделки.На KRAKEN функциональность сочетается с внимательным отношением

к безопасности клиентов,

что делает процесс покупок более

предсказуемым, защищенным и, как

следствие, популярным среди пользователей, ценящих анонимность и

надежность. -

Yesterday, while I was at work, my sister stole my

apple ipad and tested to see if it can survive a twenty five

foot drop, just so she can be a youtube sensation. My apple ipad is now destroyed and she has 83 views.

I know this is completely off topic but I

had to share it with someone! -

Very nice article, totally what I was looking for.

-

Hi there friends, good piece of writing and good urging commented

here, I am actually enjoying by these. -

Hello, I want to subscribe for this blog to obtain latest updates, so where can i do it please help

out. -

Have you ever considered writing an e-book or guest authoring

on other blogs? I have a blog based upon on the same subjects

you discuss and would love to have you share some stories/information. I know my

readers would enjoy your work. If you’re even remotely interested, feel free to shoot me an e mail. -

Write more, thats all I have to say. Literally, it seems as though you

relied on the video to make your point. You obviously know what youre talking about, why

throw away your intelligence on just posting videos to your weblog when you could be giving us something

enlightening to read? -

Заказывал электромонтаж для офиса,

сделали все строго по проекту и ТЗ. -

به نظرم در موضوعاتی مثل شرط بندی و بازیهای پولی، اولین اصل احتیاطه و بعد بررسی دقیق.

سلام وقتتون بخیر، معمولاً فقط وقتی چیزی برام جالب باشه نظر میدم.

چند وقت پیش وقتی داشتم تجربه

بقیه کاربرا رو میخوندم به این سایت رسیدم.

بعد از اینکه کمی توی سایت چرخیدم حس کردم برای آشنایی اولیه

میتونه مفید باشه. برداشت شخصی من اینه که نباید فقط

به ظاهر سایت اعتماد کرد. یکی از دوستای نزدیکم

همیشه میگفت قبل از هر کاری باید شرایط رو کامل خوند.

به همین خاطر چند بخش روبا حوصلهتر خوندم.

نکتهای که توجهم رو جلب کرد که میشد راحتتر موضوع رو فهمید.

در عین حال این به معنی تأیید کامل نیست.برای کسانی که میخوان درباره بازی انفجار

بیشتر بدونن، میتونه برای آشنایی اولیه مفید باشه.

از طرف دیگه پلتفرمهایی مثل

پلتفرم enfejɑгonline و siƄet باعث شدن کاربرا بیشتر دنبال مقایسه باشن.

یکی از آشناهای من بیشتر دنبال پیشبینی ورزشی بود و همیشه میگفت اگر سایتی توضیحات ساده و روشن

نداشته باشه، بهتره آدم با احتیاط بیشتری جلو بره.

در مجموع برای شروع آشنایی بد نبود.

من پیشنهاد میکنم هم تجربه بقیه

رو بخونه و هم خودش بررسی کنه.من احتمالاً بعداً دوباره برمیگردم و بخشهای بیشتری رو

نگاه میکنم، چون بعضی قسمتهاش برای مقایسه با سایتهای دیگه قابل توجه بود.Also visit my web-site کالبدشکافی بدترین دستها در بازی بلکجک (دستهای ضعیف)

-

Спасибо за безопасный электромонтаж в детской комнате, все провода надежно спрятаны.

-

Все электромонтажные работы согласованы, никаких доплат в процессе не всплыло.

-

I visit day-to-day a few blogs and information sites to

read content, but this blog offers feature based articles. -

You really make it seem so easy with your presentation but I find this topic to be

really something which I think I would never understand.

It seems too complex and extremely broad for me. I am looking forward for your next post, I’ll

try to get the hang of it! -

Greetings! Quick question that’s entirely off topic. Do you know how to make your

site mobile friendly? My weblog looks weird when viewing from

my apple iphone. I’m trying to find a template or plugin that might

be able to correct this problem. If you have any recommendations, please share.

Appreciate it! -

I’m extremely impressed with your writing skills

and also with the layout on your blog. Is this a paid theme or

did you customize it yourself? Anyway keep up the nice quality writing, it’s rare to see

a great blog like this one nowadays. -

I am not sure where you are getting your info, but good topic.

I needs to spend some time learning more or understanding more.

Thanks for wonderful information I was looking for this info for my

mission. -

Wow, superb weblog layout! How lengthy have you been blogging for?

you make blogging glance easy. The entire look

use of medical products

your site is excellent, as neatly as the content material! -

Hi, just wanted to say, I enjoyed this post. It was funny.

Keep on posting!

-

Terrific article! That is the kind of info that are supposed to be shared around the internet.

Disgrace on Google for not positioning this publish

upper! Come on over and talk over with my web site .

Thank you =) -

El bono más extendido es el bono de bienvenida. Por lo general consiste en un extra sobre tu primer aporte, por ejemplo 100% hasta $50,000 ARS.

Esto significa que si depositás $50,000, el casino te regala otros $50,000 para apostar. -

Hi everybody, here every one is sharing these know-how, therefore

it’s good to read this weblog, and I used to pay a quick visit this blog all

the time. -

Slažem se. Njihov sustav je spas za digitalne usluge.

Sve je riješeno u par klikova, a cijena je skroz korektna.

Vrijedi svake lipe. -

Hello there! Do you use Twitter? I’d like to follow you if that would be

ok. I’m absolutely enjoying your blog and look forward to new updates. -

whoah this weblog is wonderful i like studying your posts.

Stay up the good work! You already know, lots of people

are searching round for this info, you can help them greatly. -

Hi there, I enjoy reading through your post.

I wanted to write a little comment to support you.

-

Great article. I really enjoyed reading

the detailed football analysis and match statistics presented here.

The information is clear, informative, and helpful for anyone interested

in following the latest football developments. -

Лучшие промокоды на бесплатную ставку 1xbet нашел именно здесь, спасибо

админам.Also visit my blog промокод 1хБет при регистрации

-

Лучшие промокоды на бесплатную ставку 1xbet нашел именно здесь, спасибо админам.

my web blog промокод 1хбет при регистрации

-

Скопировал промокод 1xbet при регистрации, на

счет сразу упал повышенный бонус,

все супер.Feel free to surf to my web-site 1хбет бонус

-

Thank you for the auspicious writeup. It actually used to be a entertainment account it.

Glance advanced to far introduced agreeable from you!

However, how could we be in contact? -

Wow, fantastic blog layout! How long have you ever been blogging for?

you made blogging look easy. The whole glance of your website is fantastic, let

alone the content! -

Have you ever considered about including a little bit more than just your articles?

I mean, what you say is fundamental and all. But imagine

if you added some great visuals or videos to give your posts

more, “pop”! Your content is excellent but with images and clips, this site could certainly be one of the

most beneficial in its field. Good blog!Here is my web blog; Вместе за мир

-

I got this site from my buddy who told me regarding this site and now this time I am visiting this web page and reading very informative articles at this

time. -

Usеful content. Мany people ᴡill benefit fгom tһe

infоrmation shared іn this post.Μy blog post attorneyadvice

-

Awesome blog! Is your theme custom made or did you download it from somewhere?

A design like yours with a few simple adjustements would really make my blog shine.Please let me know where you got your design. With thanks

-

Hello there, You have done an excellent job. I will certainly digg it and personally suggest to

my friends. I’m sure they’ll be benefited from this site. -

Hi, I do believe this is an excellent web site. I stumbledupon it 😉 I

will revisit once again since i have book marked it.

Money and freedom is the greatest way to change, may you be rich

and continue to help others. -

Thanks for one’s marvelous posting! I quite enjoyed reading it, you happen to be a great author.

I will always bookmark your blog and definitely will

come back later in life. I want to encourage

that you continue your great posts, have a nice holiday weekend! -

This website really has all the information and facts I needed concerning this subject and didn’t know

who to ask. -

always i used to read smaller posts that as well clear their motive, and that is also happening with this article

which I am reading here. -

I got this web page from my buddy who told me on the topic of this website and at

the moment this time I am browsing this website and

reading very informative articles or reviews at this place. -

Hello, i think that i noticed you visited my website so i came to return the desire?.I am trying to in finding things to enhance my web

site!I assume its ok to make use of a few of your ideas!! -

Hello, Neat post. There is a problem along with your site in web

explorer, could check this? IE still is the market leader and a large portion of folks will omit your excellent writing because of this problem. -

11BET Việt Nam – Nền tảng cá cược thể thao và bóng đá hấp dẫn uy tín nhất

Việt Nam. Đăng ký ngay để nhận hàng loạt khuyến mãi

hấp dẫn mỗi ngày. Đồng thời cung cấp nhiều Tips cá độ hiệu quả hỗ trợ người chơi tham khảo. -

This is a very informative post about online casinos and betting platforms.

I especially liked how it explains the importance of choosing a

secure site before signing up.Many players often ask where they can find reliable gaming platforms with fair odds and smooth payouts.

From what I’ve seen, checking platforms like vn22vip helps users compare features, bonuses, and overall experience.Thanks for sharing these insights — they’re helpful for both

beginners and experienced bettors. -

Hola! I’ve been reading your website for a while now and finally got the courage to go ahead

and give you a shout out from Austin Texas!

Just wanted to say keep up the excellent job! -

Magnificent goods from you, man. I’ve understand your stuff previous to and you are just too great.

I really like what you have acquired here, really like what you’re saying and the

way in which you say it. You make it entertaining and you

still care for to keep it sensible. I can’t wait to read far more from you.

This is really a tremendous website. -

Hey There. I found your blog using msn. This is a really well written article.

I will be sure to bookmark it and return to read more

of your useful information. Thanks for the post. I will definitely return. -

My brother suggested I might like this web

site. He was entirely right. This post truly made my day.

You cann’t imagine simply how much time I had spent for this

info! Thanks! -

What’s up mates, how is the whole thing, and what you would like to say on the topic of this piece of writing, in my view its truly remarkable in support of me.

-

My relatives always say that I am killing my time here

at net, but I know I am getting know-how all the time by

reading such nice posts. -

Why users still make use of to read news papers when in this technological

globe all is available on web? -

I’m really enjoying the theme/design of your weblog.

Do you ever run into any browser compatibility issues? A handful of my blog audience have complained about my site not working correctly in Explorer

but looks great in Safari. Do you have any suggestions to help fix this

issue? -

hnfr9r

-

Everything is very open with a precise description of the challenges.

It was definitely informative. Your website is useful. Many thanks for sharing!

-

Unquestionably imagine that which you said. Your favourite justification appeared to be on the net the easiest factor to take into account of.

I say to you, I certainly get irked even as other people think about worries that they plainly do not recognize about.

You controlled to hit the nail upon the top as well as defined out the whole thing with no need side-effects , other people

can take a signal. Will probably be back to

get more. Thanks -

I’m really enjoying the theme/design of your blog. Do you

ever run into any internet browser compatibility problems?

A number of my blog audience have complained about my blog not working correctly in Explorer but looks great in Opera.

Do you have any solutions to help fix this problem? -

Appreciation to my father who shared with me regarding

this weblog, this blog is really remarkable. -

Viagra and epilim. Is it safe

-

Срочное изготовление печатей, цена соответствует заявленной на сайте, никаких скрытых доплат.

-

Срочное изготовление печатей организации, предоставил ИНН,

макет сгенерировали автоматически. -

Hi there, just wanted to mention, I enjoyed this blog post.

It was inspiring. Keep on posting!

-

I truly love your blog.. Excellent colors & theme. Did you develop

this site yourself? Please reply back as I’m looking to create my own website and want to find out where you got this from or exactly what the theme is named.

Cheers! -

Candy Gas Strain: Flavor, Effects, Genetics, Growing Guide & Expert

Insights candy gas Strain -

Thanks for your marvelous posting! I actually enjoyed reading

it, you will be a great author. I will remember to bookmark your blog and may come back down the

road. I want to encourage yourself to continue your great work, have a nice weekend! -

Its such as you learn my thoughts! You seem to grasp so much about this, like

you wrote the e-book in it or something. I feel that

you just can do with some percent to pressure the message house a little bit, but instead of that, this is fantastic blog.An excellent read. I’ll definitely be back.

-

Great post. I used to be checking continuously this

weblog and I am inspired! Very useful information specifically the final phase 🙂 I maintain such

info much. I used to be looking for this particular information for a long time.

Thanks and best of luck. -

Its not my first time to pay a visit this website,

i am visiting this site dailly and take pleasant information from here daily. -

Jungle Driving Scchool Omaha

4020 Ѕ 147th St, Omaha,

ΝΕ 68137, Unityed States

14024170547

fleet driver training -

My brother recommended I may like this web site. He used

to be entirely right. This publish truly made my day.

You can not imagine just how so much time I had spent for this information! Thank

you! -

What’s up, everything is going fine here and ofcourse every one is sharing facts, that’s truly fine, keep up writing.

-

Hey There. I found your blog using msn. This is an extremely

well written article. I’ll make sure to bookmark it and return to read more of your useful info.Thanks for the post. I’ll certainly return.

-

My brother suggested I would possibly like this web site. He

was once totally right. This submit actually made my day.

You can not consider simply how so much time I had spent for

this info! Thanks! -

What’s up, after reading this amazing piece of writing i

am as well glad to share my experience here with colleagues. -

The 1xbet latest promo code gives new registrations an immediate upgrade over the

standard baseline offers.my page – 1xbet promo code no deposit

-

Register using the 1xbet promo code casino to experience premium table games with

extra starting credits.Look into my web site 1xbet ipl promo code

-

Enter the 1xbet promo code 1X200ART during registration to instantly unlock your 1xbet welcome bonus 2026.

Have a look at my page 1xbet promo code bangladesh 2026

-

The 1xbet free bet code remains fully functional for all verified user accounts created this week.

Feel free to visit my page – 1xbet active promo code today

-

This post provides clear idea in support of the

new viewers of blogging, that genuinely how to do blogging and site-building. -

Качественная консультация психолога онлайн

избавила от постоянной тревоги. -

Definitely imagine that which you said. Your favourite reason appeared

to be on the internet the simplest thing to take into account of.

I say to you, I definitely get irked at the same time as folks think about issues that they just do not know about.

You controlled to hit the nail upon the top and also defined

out the entire thing with no need side-effects , other folks can take a signal.

Will likely be back to get more. Thank you -

Своевременная консультация психолога в

Краснодаре решила семейный кризис. -

This is a very good tip particularly to those new to the blogosphere.

Brief but very accurate information… Many thanks for sharing this

one. A must read article! -

Внимательный психолог онлайн консультация длилась

ровно час, все успели. -

Howdy! Quick question that’s completely off topic. Do you know how to make your site mobile friendly?

My site looks weird when viewing from my iphone 4.

I’m trying to find a template or plugin that might be able to resolve this issue.

If you have any recommendations, please share. Thanks! -

Hey there just wanted to give you a quick heads up and let you know a few of

the images aren’t loading properly. I’m not sure why but I think its a linking issue.

I’ve tried it in two different web browsers and both show the same outcome. -

Greetings! Very helpful advice within this article!

It is the little changes that produce the biggest changes.

Thanks for sharing! -

Hello! I know this is kinda off topic but I was wondering

which blog platform are you using for this website?

I’m getting sick and tired of WordPress because I’ve had problems with

hackers and I’m looking at options for another platform.

I would be awesome if you could point me in the direction of a

good platform. -

Hello there! This is my first comment here so I just wanted to give a quick shout out and tell you I really enjoy reading through your

blog posts. Can you suggest any other blogs/websites/forums that cover

the same subjects? Appreciate it! -

Superb site you have here but I was wondering if you knew of any forums that cover

the same topics talked about here? I’d really love to be a part of group where I can get comments from other experienced individuals that share the same interest.

If you have any recommendations, please let me know.Many thanks!

-

Howdy just wanted to give you a brief heads up and let

you know a few of the images aren’t loading properly.

I’m not sure why but I think its a linking issue.

I’ve tried it in two different web browsers and both show the same outcome. -

I do not even know how I ended up here, but I thought this post

was great. I do not know who you are but certainly you are going to a famous blogger if you aren’t

already 😉 Cheers! -

Way cool! Some very valid points! I appreciate

you penning this post plus the rest of the site is also very

good. -

I visited multiple web pages but the audio feature for audio songs present at this website is

genuinely superb. -

What’s Going down i am new to this, I stumbled upon this I’ve discovered It

absolutely helpful and it has helped me out loads.

I hope to contribute & help other customers like its aided me.

Good job. -

Hello! Do you use Twitter? I’d like to follow you if that would

be ok. I’m undoubtedly enjoying your blog and look forward to new

updates. -

This is a very informative post about online casinos and betting platforms.

I especially liked how it explains the importance of choosing a trusted

site before signing up.Many players often ask where they can find reliable gaming platforms

with fair odds and smooth payouts. From what I’ve seen, checking platforms like vn22vip helps users compare

features, bonuses, and overall experience.Thanks for sharing these insights — they’re helpful for both beginners and experienced bettors.

-

Hi there! Ӏ know this is kinda off tօρic howeᴠer , I’d figurеd I’d

ask. Would you bbe interеsted in trading links or maybe guest writing a

ƅlog article or vice-ѵersa? My site goiеs over a lot of the

samе subϳects as yours ɑnd I think we coᥙld greatly benefit from eacһ other.If you might be interdsted feeⅼ free to swnd mee an emaіl.

I look forward to hearing from you! Terrific blog by the way!Alѕo visit my webpage … بازی انفجار

-

When some one searches for his necessary thing, therefore he/she needs to be available that in detail, so that thing is maintained over here.

-

Hiya very cool blog!! Guy .. Beautiful ..

Wonderful .. I’ll bookmark your website and take the

feeds additionally? I’m happy to search out a lot of useful information right here in the put

up, we need develop more techniques on this regard, thanks for

sharing. . . . . . -

Thanks for sharing your thoughts about .

Regards -

Appreciation to my father who informed me on the topic of this

website, this weblog is genuinely amazing. -

I got this web page from my friend who informed me on the topic of this web site and now this time I am

visiting this web site and reading very informative articles at this place. -

Thanks a bunch for sharing this with all of us you really know what you’re speaking approximately!

Bookmarked. Kindly also talk over with my website =).

We could have a link trade agreement among us -

It’s amazing to pay a quick visit this web site and reading the views of all mates regarding

this article, while I am also zealous of getting experience. -

At this time I am going away to do my breakfast, after having my breakfast coming over again to read other news.

-

It’s actually a nice and useful piece of info.

I am happy that you simply shared this helpful

information with us. Please keep us up to date like this.

Thank you for sharing. -

I’ll right away snatch your rss as I can’t find your email subscription link or e-newsletter

service. Do you have any? Kindly permit me recognize in order

that I may just subscribe. Thanks. -

This is really interesting, You are a very skilled blogger.

I’ve joined your rss feed and look forward to seeking

more of your great post. Also, I have shared your web site in my social networks! -

Hi I am so thrilled I found your weblog, I really found you by error, while I was looking on Yahoo for

something else, Anyways I am here now and would just like to

say thank you for a fantastic post and a all round enjoyable

blog (I also love the theme/design), I don’t have time to read through it all at the moment

but I have saved it and also included your RSS feeds, so when I have time I will be

back to read a lot more, Please do keep up the excellent job. -

This is a very informative post about online casinos and betting platforms.

I especially liked how it explains the importance of

choosing a secure site before signing up.Many players often ask where they can find reliable gaming platforms with fair

odds and smooth payouts. From what I’ve seen, checking platforms like vn22vip helps users compare features, bonuses,

and overall experience.Thanks for sharing these insights — they’re helpful for both beginners and experienced bettors.

-

Franchising Path Carlsbad

Carlsbad, СA 92008, United Ѕtates

+18587536197

starting a franchise cost -

Wow, awesome blog layout! How long have you been blogging for?

you made blogging look easy. The overall look of your web site is excellent,

as well as the content! -

It is in reality a great and useful piece of information. I’m satisfied

that you simply shared this useful information with us.Please keep us up to date like this. Thank you for sharing.

-

오피가이드를 처음 이용하시나요? 허위 리뷰를 걸러내고 안전하게

업소를 찾는 방법부터 최신 트렌드, 자주

묻는 질문까지 한눈에 파악할 수

있는 완벽한 오피가이드 활용 매뉴얼을 확인해 보세요. -

Выбирайте заводской бетон купить в Минске для надежного возведения

фундаментов, заборов и перекрытий.

Рассчитайте, сколько стоит куб бетона

м300 цена с доставкой, и оформите выезд миксера. -

I like the valuable info you provide for your articles.

I will bookmark your weblog and take a look at once

more here frequently. I’m reasonably sure I’ll be told plenty of new stuff proper here!

Good luck for the following! -

It’s wonderful that you are getting thoughts from this paragraph as well as from our dialogue made here.

-

Thank you for the auspicious writeup. It in fact was a amusement account it.

Look advanced to far added agreeable from you!

By the way, how can we communicate? -

Stunning quest there. What occurred after? Thanks!

-

Generally I don’t read post on blogs, but I would like

to say that this write-up very forced me to check out and do so!

Your writing taste has been amazed me. Thank you, quite great post. -

Simply desire to say your article is as surprising.

The clearness on your publish is just spectacular and that i can think you’re an expert in this subject.

Well along with your permission allow me to grasp your RSS feed to stay

up to date with drawing close post. Thank you a

million and please continue the gratifying work. -

I really like it when individuals get together and share

views. Great website, continue the good work! -

Thank you a bunch for sharing this with all folks you really realize what you are speaking approximately!

Bookmarked. Kindly additionally talk over with my site =).

We could have a link trade contract between us -

Amazing issues here. I am very satisfied to see your post.

Thanks so much and I’m looking forward to contact you.

Will you kindly drop me a mail? -

Awesome post.

-

Wow, superb blog layout! How long have you been blogging

for? you made blogging look easy. The overall look of your website is great, let alone the content! -

It is generally not recommended to take ephedrine and Viagra together without consulting a healthcare professional.

-

Thank you for the auspicious writeup. It in fact was

a amusement account it. Look advanced to more added agreeable from you!By the way, how can we communicate?

-

I was suggested this web site by my cousin. I am not

sure whether this post is written by him as no one

else know such detailed about my problem. You’re amazing!

Thanks! -

What’s up, I read your blog regularly. Your writing style is awesome, keep it up!

-

ГдеБЕНЗ — скачать приложение на Андроид https://www.apkfiles.com/apk-621438/

-

Exotic Dubai Escorts – Book the Top https://forum.showingstockingtops.com/profile.php?mode=viewprofile&u=14290

-

Awesome blog! Do you have any suggestions for aspiring writers?

I’m planning to start my own website soon but I’m a little lost on everything.

Would you propose starting with a free platform like WordPress or go for a paid option? There are

so many options out there that I’m completely overwhelmed ..

Any ideas? Thanks! -

Very nice post. I just stumbled upon your weblog and wanted to say that I have really

enjoyed browsing your blog posts. In any case I’ll be subscribing to your rss

feed and I hope you write again very soon! -

If you want to grow your experience only keep visiting

this site and be updated with the latest gossip posted here. -

Hello it’s me, I am also visiting this website regularly, this web page is genuinely nice and the visitors are really sharing fastidious thoughts.

-

Useful information. Fortunate me I discovered your site accidentally, and I’m shocked why this twist of fate didn’t came about in advance!

I bookmarked it. -

Sweet blog! I found it while searching on Yahoo News.

Do you have any tips on how to get listed in Yahoo

News? I’ve been trying for a while but I never seem to get there!

Thank you -

By incorporating Singaporean contexts гight into lessons, OMT

mɑkes math relevant, fostering love аnd motivation for high-stakes examinations.Experience flexible learning anytime, аnywhere tһrough OMT’ѕ thorouɡh online e-learning platform,

including unlimited access tⲟ video lessons аnd interactive tests.Іn Singapore’ѕ extensive education system, wһere mathematics

іs required аnd consumes aгound 1600 һourѕ of curriculum tіme in primary school ɑnd secondary

schools, math tuition еnds up Ƅeing necеssary tο hеlp students build a strong foundation fⲟr l᧐ng-lasting success.primary school math tuition builds exam stamina tһrough timed

drills, mimicking tһe PSLE’s two-paper format аnd helping

students handle tіme effectively.Structure ѕelf-assurance throսgh constant tuition assistance іs impօrtant, as

O Levels can ƅe stressful, andd confident trainees ⅾо

Ьetter under pressure.With routine mock tests аnd comprehensive feedback, tuition helps junior university student determine аnd correct

weaknesses ƅefore thе real A Levels.OMT stands aⲣart witһ its syllabus designed to sustain MOE’ѕ by incorporating mindfulness techniques to minimize math anxiousness thr᧐ughout research studies.

Gamified aspects make modification fun lor, urging mοre

practice and causing quality renovations.Tuition reveals pupils tօ varied concern types, widening tһeir preparedness fߋr unpredictable Singapore math examinations.

Feel free tߋ surf to my web blog – math home tutoring at mont kiara

-

Cashify helps you Sell phone online at the best prices.

-

Its like you read my mind! You appear to know so much about this, like you

wrote the book in it or something. I think that

you can do with a few pics to drive the message home a little bit, but instead of

that, this is excellent blog. An excellent read.

I will definitely be back. -

May I just say what a relief to discover someone who

really knows what they are talking about online.

You actually realize how to bring a problem to light and make it important.

A lot more people must read this and understand this side of the story.

I can’t believe you’re not more popular because you most

certainly possess the gift. -

Kush Mintz: Full Breakdown Of Genetics, Effects, And Uses Kush mintz

-

You actually make it seem really easy together with your presentation but I

find this matter to be really something that I feel I would by no means understand.

It seems too complicated and very large for me.

I am taking a look ahead to your subsequent submit, I will try to get the hold of it! -

Peculiar article, totally what I needed.

-

Hello There. I found your blog using msn. This is an extremely well written article.

I will be sure to bookmark it and return to read more of your helpful

info. Thank you for the post. I’ll definitely return.Stop by my homepage :: บทความเครื่องครัว

-

This is a very informative post about online casinos and betting platforms.

I especially liked how it explains the importance of choosing a secure site

before signing up.Many players often ask where they can find reliable gaming platforms

with fair odds and smooth payouts. From what I’ve seen, checking platforms like vn22vip helps users compare features,

bonuses, and overall experience.Thanks for sharing these insights — they’re helpful for

both beginners and experienced bettors. -

Hi, i think that i saw you visited my web

site thus i came to “return the favor”.I am attempting to

find things to enhance my website!I suppose its ok to

use a few of your ideas!! -

Currently it seems like Drupal is the best blogging platform available right now.

(from what I’ve read) Is that what you are using

on your blog? -

Awesome blog! Do you have any hints for aspiring writers?

I’m hoping to start my own site soon but I’m a little lost

on everything. Would you suggest starting with a free platform like WordPress or go for a paid option? There are so many options out there that I’m

totally confused .. Any tips? Bless you! -

I’m gone to convey my little brother, that he should also pay a visit

this website on regular basis to take updated from most recent gossip. -

Magnificent items from you, man. I have take note your stuff previous to and you are just extremely excellent.

I really like what you have acquired right here, really like what you

are saying and the best way during which you are saying it.

You are making it enjoyable and you continue to care for to keep it sensible.

I can’t wait to learn much more from you. This is actually a tremendous website. -

Superb blog! Do you have any hints for aspiring writers? I’m planning to start

my own site soon but I’m a little lost on everything. Would you advise

starting with a free platform like WordPress or go for a paid

option? There are so many options out there that I’m totally confused ..

Any recommendations? Thanks! -

I’m not sure why but this site is loading extremely slow for me.

Is anyone else having this problem or is it a problem on my end?