What Is the Value of a Credit Score?

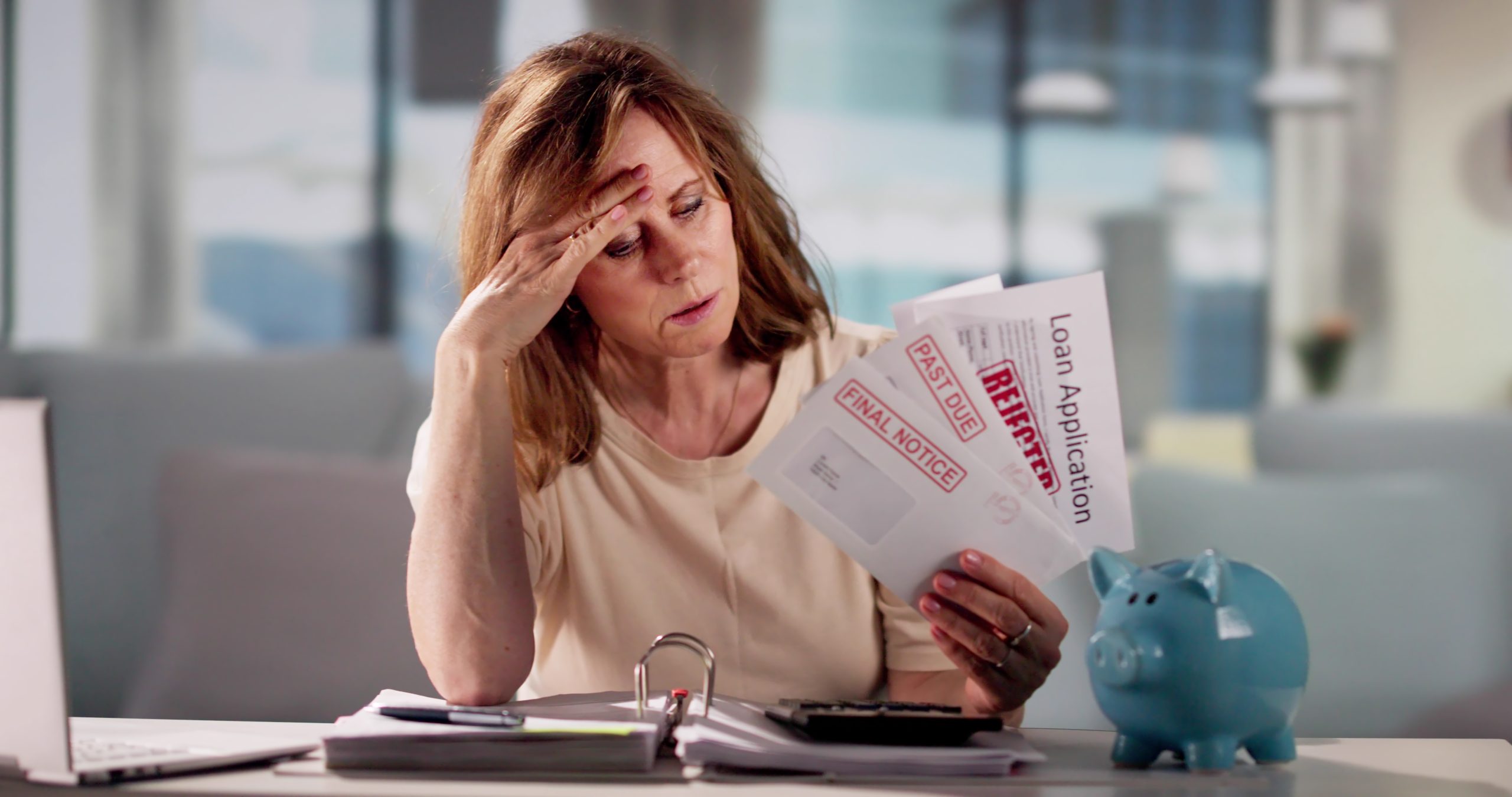

Anyone struggling with debt could also be dealing with a low credit score. In modern banking, credit scores determine everything from getting a loan to renting an apartment. They’re often seen as a reflection of financial responsibility, but they tell only part of the story. Many hardworking people with financial challenges can have low credit scores through no fault of their own, whether due to unexpected life events, medical bills, or job loss.

But what exactly is the value of having a good credit score? And is it necessary to achieve debt freedom? We’ll cover these questions and more in our simple guide to help you better understand credit scores. In it, you’ll learn:

- What a credit score is and its purpose

- hen good credit is required

- How to manage a solid financial future with less-than-perfect credit

- The value of credit-building strategies

With these tips, you’ll understand how to manage your credit score to create a solid financial future for yourself.

What is a credit score, and why is it important?

A credit score is a three-digit number that lenders use to determine how likely you are to repay what you borrow.

Three leading credit score companies provide this number, so it’s common to hear it referred to as a TransUnion, Equifax, or Experian credit score. The score is determined based on your credit report, a complete record of how you have managed debt throughout your history.

Factors that go into calculating your score include:

Payment history: Are you making your required payments on time?

Outstanding debt: What percentage of your available credit are you using, and what is your total debt amount?

Credit age: How long have you managed your accounts and credit?

Types of accounts: What is the mix of unsecured (like credit cards) and secured (like home loans) debt you hold?

Inquiries for new credit: Are you applying for new lines of credit or loans? If so, how often?

What is considered a good credit score?

Each of the three leading credit score companies has its own charts (depending on whether it adheres to FICO® or VantageScore); however, they all provide the same general indicators. Generally, a 600 credit score and 650 credit score are considered fair, while a 700 credit score and 750 credit score are considered good.

Pro Tip #1

Get a free credit score report today – it’ll save you time and trouble. But make sure it’s the main one you get per year. Otherwise, it’s considered a hard credit inquiry and can impact your credit score.

Traditionally, a credit score is essential as it is the foundation for borrowing money to improve one’s quality of life and establish trust with creditors.

But that isn’t always the case.

When is good credit needed?

One myth about consumer finance is that good credit is vital for a good life. But good credit doesn’t actually buy you anything. In fact, the whole point of having good credit is to allow you to borrow money on terms in your favor rather than directly purchasing something.

For example, having good credit is essential if you want to purchase a house, car, or make an expensive transaction. It may help you secure better rates and terms on the loan, allowing you to pay off your debt faster and at a lower cost.

On the other hand, if you need some cash for an emergency or short-term expense, a vacation, or shopping, then good credit won’t be necessary. You can often find ways to pay these expenses without a high credit score.

So, if you are stressed about purchasing with poor credit, don’t be. You may meet more criteria than you’d think when performing everyday financial activities with less-than-perfect credit.

What truly matters is learning how to manage your finances with confidence and making progress at your own pace. Whether you’re rebuilding, maintaining, or just starting out, remember that good credit can always be earned back, and it’s never too late to start.

How to manage a solid financial future with less-than-perfect credit

While poor credit is not ideal, it doesn’t mean you can’t achieve your goals. Many people with low credit scores live happy and successful lives. The truth is that several other factors are important in any loan process, and keeping your credit score in check is just one of them but not always the most important.

For example, those with low or poor credit scores (<580) may still qualify for a loan if they have other assets or factors in their favor. This could include having a steady income, enough savings to cover the loan payments, and responsible payment habits with proof from past utility bills and rental agreements.

On a positive note, you don’t need the highest credit score. Be aware that not being able to keep up with loans and payments when you have less-than-perfect credit can further damage your score.

To avoid this, establish a budget and stick to it, even when times are tough. Doing so will help you keep up with payments, protect your credit score, and ensure you’re in a better financial position if you want to apply for other loans or lines of credit down the line.

The value of credit-building strategies

Credit-building strategies help establish and maintain a good credit score to achieve financial freedom. They are also vital to building a solid financial plan that helps get you out of debt and into a stress-free life.

Secured credit cards

A secure credit card can be a great way to get the credit you need while building your score. These cards require a deposit used as collateral if you default on payments. They generally have lower interest and fees than unsecured cards, and issuing banks report your payments to credit bureaus, helping you build your credit history over time.

Payment reminders

Paying bills on time is one of the best ways for anyone with a low credit score to start rebuilding it and staying on track. Payment reminders help ensure monthly bills are paid on time and in full.

Pro Tip #2

A reminder is not the actual payment, so if you have trouble following through, consider setting up automatic payments so that the money is taken out of your account before there is a chance to forget.

Regularly check your credit report

Sometimes, your low credit score may be an error on the credit reporting agency’s part and no fault of your own. However, by checking your credit report regularly, you can ensure that any errors or other factors that may damage your score are immediately addressed.

Low credit is not always a problem

Credit is only one of many factors used in major financial decisions from banks like loans and mortgages. So, if your credit is less than perfect today, many options are available to help you get by as you build up to the best credit score possible.

With the right strategies and help, even low credit scores won’t keep you from turning your financial goals into reality. For those who are in debt and have a low credit score, it is normally suggested to focus on getting rid of the debt first and then focusing on increasing your credit score.

If you’re in debt and dealing with a low credit score, you can enroll in a debt relief company to help you on the path of financial freedom.

Disclaimer: The information provided in this article is for general informational purposes only and is not intended as legal, financial, or professional advice. We do not guarantee any specific outcomes, and results may vary based on individual circumstances. We comply with all applicable laws, including the California Debt Settlement Services Act, and recommends consulting with an attorney or financial advisor before making any financial decisions. We are not responsible for the accuracy of external links or content, and all website content is protected by copyright laws. We reserve the right to update or remove content at any time without notice.

Frequently asked questions

What’s the difference between a FICO® score vs. credit score?

While they may sound like two different things, they are actually the same. To be more exact, a FICO® score refers to a type of credit score that creditors use to determine loans.

What credit score is needed to buy a house?

Lenders typically look for a credit score of at least 620 to buy a house. Higher scores can secure better mortgage rates. Call your bank to see if you have a unique case.

Why is my credit score going down?

Your credit score can decrease due to several factors, such as missed payments, high credit card balances, or applying for new credit.

Why did my credit score drop for no reason?

Your credit score might drop unexpectedly for several reasons, such as report delays, credit utilization changes, or inaccuracies. As mentioned earlier, regularly checking your credit report for any discrepancies is essential.

How often is a credit score updated?

Credit scores are updated whenever new information is reported to the credit bureaus, typically every 30 to 45 days. However, the exact frequency can vary based on your creditors’ reporting habits.

What is the highest credit score possible?

The highest credit score possible is typically 850 on the FICO scale, one of the most used scoring models. Achieving this score indicates an exceptional credit history and financial behavior.

When was credit score invented?

The credit score was invented in 1958 when Bill Fair and Earl Isaac introduced the first credit scoring system, called Credit Application Scoring Algorithms. This system marked the beginning of modern methods for evaluating creditworthiness.

Can I improve my credit score while I’m still paying off debt?

Yes, absolutely. Improving your credit score doesn’t require being completely debt-free, it’s about how responsibly you manage the debt you have. Paying bills on time, keeping credit card balances low, and avoiding unnecessary new credit applications can all help raise your score over time. Even small, consistent improvements in your payment habits can make a big difference.

Disclaimer: The information provided here is for general informational purposes only and does not constitute legal, financial, or tax advice. Laws and regulations vary by state and individual circumstances, so always consult a qualified professional for personalized guidance.

9586 Comments

-

1plusgame: Top Slot Online in the Philippines. Easy Login, Register, and Download App via Official Link. Experience 1plusgame, the top slot online in the Philippines. Use our official link for fast 1plusgame login, easy register, and 1plusgame download app. Join and win now! visit: 1plusgame

-

[9011]Jadesportsbet Official Site: Secure Login, Easy Register, and App Download for the Best Slots and Sports Betting in the Philippines. Experience the best slots and sports betting at the Jadesportsbet official site. Secure your jadesportsbet login, complete a fast jadesportsbet register, and get the jadesportsbet app download for premium gaming in the Philippines. Play jadesportsbet slots and win today! visit: jadesportsbet

-

[75]62jl Casino: Best Online Slots in the Philippines. Quick 62jl Login, Easy Register, and Official 62jl App Download. Join 62jl Casino for the best online slots in the Philippines! Quick 62jl login, easy 62jl register, and 62jl app download. Play top 62jl slot games and win big today! visit: 62jl

-

[2880]jl777 slots|jl777 download|jl777 login|jl777 giris|jl777 casino Experience the ultimate gaming thrill at jl777, the Philippines’ premier online casino. Secure your jl777 login to play top-rated jl777 slots and live casino games. Get the jl777 download for mobile access and enjoy seamless jl777 giris entry for big wins and 24/7 entertainment. visit: jl777

-

[9192]cc7 Casino Online Philippines: Fast cc7 Login, Register & App Download for the Best cc7 Slots. Experience cc7 Casino Online Philippines! Get the best cc7 slots, fast cc7 login, easy cc7 register, and official cc7 app download. Join the PH’s top casino now! visit: cc7

-

[5284]Casinomaxx Official Site: Easy Login, Register & App Download. Play the Best Online Slots in the Philippines Today! Join the Casinomaxx official site for the best online slots in the Philippines! Enjoy a quick Casinomaxx login and register today. Secure your Casinomaxx app download to start playing and winning anytime, anywhere. visit: casinomaxx

-

[5759]Jilibet777: The Philippines’ Best Online Casino for Real Money – Legit JILI Slots & Easy GCash Cash In Experience world-class gaming at Jilibet777, the best online casino in the Philippines for real money. As the jilibet777 official website, we provide a secure platform for legit JILI slots Philippines and a variety of top-tier games. Enjoy the convenience of an online casino with GCash cash in and fast withdrawals. Secure your jilibet777 casino login today to start winning on the most trusted and legitimate gaming platform in the country! visit: jilibet777

-

[6196]Sugal777 Philippines: Top Online Slot & Casino. Secure Sugal777 Login, Easy Daftar, and Official App Download with Link Alternatif. Join Sugal777 Philippines, the top online slot and casino destination. Access secure sugal777 login, easy daftar sugal777, and official sugal777 app download. Use our link alternatif sugal777 for seamless gaming and big wins today! visit: sugal777

-

[2687]LVBET Philippines: Best Online Slots & Casino Bonus. Easy LVBET Login, Register & App Download. Experience the best LVBET slots and casino bonus in the Philippines! Enjoy easy LVBET login, register, and LVBET app download. Join PH’s top online casino today! visit: lvbet

-

[4349]Aceph Official Site: Top Slots, Easy Login, Register & App Download for Philippines Players Join Aceph Official Site for the best gaming in the Philippines. Experience fast aceph login, easy aceph register, and top-tier aceph slots. Get the aceph app download today to start winning! visit: aceph

-

[8202]Experience the best online casino in the Philippines with Okebet4: Secure GCash gambling and easy mobile app access. visit: okebet4

-

[8132]Melbet Philippines Official Site: Secure Registration, Login, App Download & Premium Casino Slots Visit the Melbet Philippines official site for secure melbet registration and login. Play premium melbet casino slots and get the melbet app download for free! visit: melbet

-

[9512]Joyjili Casino Online Philippines: Play Top Slot Games, Easy Joyjili Login & Register. Get the Official Joyjili App Download for the Ultimate Gaming Experience! Join Joyjili Casino Online Philippines! Play top Joyjili slot games with easy Joyjili login and register. Get the official Joyjili app download for the ultimate mobile gaming experience today! visit: joyjili

-

[2927]fb7777: The Best Legit Online Casino Philippines for GCash Slots & Sports Betting Join fb7777, the best online casino Philippines GCash users trust for legit online gambling. Register via fb7777 login registration for top slots and sports betting today! visit: fb7777

-

[7099]The Top Online Casino in the Philippines: Premium Slots and Fast GCash Gaming. visit: taya333

-

[6862]Pesomax Online Casino Philippines: Top Slot Games, Easy Register, Login & App Download. Experience Pesomax Online Casino Philippines! Enjoy top-rated Pesomax slot games with a quick Pesomax register and login process. Secure your Pesomax app download today for the best mobile gaming experience. Join the #1 online casino in the Philippines and start winning now! visit: pesomax

-

[9677]PH3333: The Best Online Casino in the Philippines. Easy Login, Register, and App Download for Premium Slots and Big Wins! Join PH3333, the best online casino in the Philippines. Quick ph3333 login, easy ph3333 register, and ph3333 app download. Play premium ph3333 slot games and win big! visit: ph3333

-

[2961]Jilino1 Casino Philippines: Top Online Slots, Easy Register, Secure Jilino1 Login & Official App Download. Join Jilino1 Casino Philippines for top Jilino1 slot games. Enjoy a fast Jilino1 register, secure Jilino1 login, and the official Jilino1 download. Play and win today! visit: jilino1

-

[6697]jl7 Casino Philippines: Easy jl7 Login, Register & App Download for Top jl7 Slot Games. Experience the best of JL7 Casino Philippines! Enjoy easy jl7 login, fast jl7 register, and top-tier jl7 slot games. Get the jl7 app download now for the ultimate jl7 casino thrill and start winning today! visit: jl7

-

[6292]Superwin Casino Philippines: Easy Login, Register & App Download. Play the Best Online Slots Today! Experience Superwin Casino Philippines! Enjoy easy superwin login, register, & superwin app download. Play premium superwin slots & enjoy the best superwin casino login. visit: superwin

-

[8423]Winph8 Online Casino Philippines: Secure Winph8 Login, Fast Register & App Download for Premium Slot Games. Join Winph8 Online Casino Philippines for premium Winph8 slot games. Enjoy a secure Winph8 login, fast Winph8 register, and easy Winph8 app download. Experience the ultimate gaming platform and start winning today! visit: winph8

-

[8515]Lago777 Official Site: Easy Login, Register & Top Online Slots in the Philippines. Download the Lago777 App for the Ultimate Casino Experience. Experience the Lago777 Official Site for the top online slots in the PH. Quick Lago777 login, easy Lago777 register & secure Lago777 app download. Win big today! visit: lago777

-

[9558]Deskgame Official: Secure Login, Register & App Download for the Best Philippines Slots. Join Deskgame Official for the ultimate Philippines slots experience! Access secure deskgame login, easy deskgame register, and the deskgame app download for premium casino gaming and big wins today. visit: deskgame

-

[9583]The Ultimate Destination for Jili Slot Games and Online Casino in the Philippines visit: jililuck 22

-

[9435]Phswerte99 Online Casino Philippines: Top Slot Games, Easy Login, Register & App Download for the Best Gaming Experience. Join Phswerte99 Online Casino, the Philippines’ premier hub for top-tier Phswerte99 slot games. Secure your Phswerte99 login, register today, or get the Phswerte99 app download for the ultimate mobile gaming experience and big wins! visit: phswerte99

-

[9147]Megapari Philippines: Quick Login & Register. Megapari App Download for Top Slots & Exclusive Promo Codes. Join Megapari Philippines for a premium gaming experience! Quick megapari login & register. Get the megapari app download for top slots and use our exclusive megapari promo code for huge bonuses. Start winning today! visit: megapari

-

[9669]MWPlay Online Casino Philippines: Your Top Destination for MWPlay Slots. Quick MWPlay Login, Register, and App Download for the Best Gaming Experience. Experience the best of MWPlay Online Casino Philippines! Access premium MWPlay slots with a quick MWPlay login and easy MWPlay register process. Boost your gaming with the MWPlay app download for seamless play anytime, anywhere. Join the #1 destination for Filipino players today! visit: mwplay

-

Yo, been hearing a lot about Jilibet Donalyn! Gotta check it out. Seems like where all the action’s at. Check it out: jilibet donalyn

-

Saw Donnalyn Bartolome promoting Jilibet! Gave it a shot because of her and gotta say, it’s pretty fun! Extra points for having Donnalyn on board! Join the fun! jilibet donnalyn bartolome

-

The okbet app download worked like a charm! No glitches, no problems, and I’m now ready to roll! Highly recommend. okbet app download

-

[8483]Experience the best online gaming at Betso88 Official. Secure betso88 login, fast betso88 register, and premium betso88 slot games. Get the betso88 app download for the #1 mobile casino experience in the Philippines. Experience Betso88 Official, the #1 Philippines casino. Secure betso88 login, fast betso88 register, & top betso88 slot games. Get the betso88 app download now! visit: betso88

-

[7363]PGAsia Online Casino: Easy Login, Register, and App Download for the Best Slots in the Philippines. Experience the best slots in the Philippines at PGAsia Online Casino. Enjoy a secure pgasia login, quick pgasia register, and easy pgasia app download for non-stop gaming action and big wins today! visit: pgasia

-

[1262]99jl Online Casino Philippines: Top Slots, Easy Login, Register & App Download Experience 99jl Online Casino, the Philippines’ premier hub for 99jl slots. Easy 99jl login & 99jl register. Get the 99jl app download and start winning today! visit: 99jl

-

[186]PlayMojo Philippines: PlayMojo Login & Register for Top Online Slots, Casino Bonuses, and App Download. Join PlayMojo Philippines! Quick PlayMojo login & register to access top PlayMojo online slots. Claim a huge PlayMojo casino bonus & get the PlayMojo app download now! visit: PlayMojo

-

[304]Magicjili: Top Philippines Online Slots & Casino App. Secure Magicjili Login, Register & App Download for the Best Gaming Experience. Experience the best Philippines online slots at Magicjili. Secure Magicjili login, register, and Magicjili app download to enjoy our premium casino app today! visit: magicjili

-

[4486]JL2 Casino Philippines: Best JL2 Slot Games, Easy Login, Register & App Download Join JL2 Casino Philippines for the best jl2 slot games. Experience fast jl2 login, easy jl2 register, and a secure jl2 download. Play at jl2 casino and win today! visit: jl2

-

[2809]JiliGames: Best Philippines Slot Online & Casino. Fast Login, Register, and Official APK Download. Experience the best Philippines slot online at JiliGames Casino. Enjoy fast jiligames login, easy jiligames register, and the official jiligames download apk. Join now! visit: jiligames

-

[632]wowph: The Best Online Casino in the Philippines. Easy wowph Login, Register & App Download for Top wowph Slot Games. Experience the ultimate gaming at wowph, the best online casino in the Philippines. Enjoy seamless wowph login and register processes to access top wowph slot games. Start your wowph app download today for big wins and 24/7 casino action! visit: wowph

-

[8804]ibetph Online Casino Philippines: Secure Login, Easy Register & App Download for the Best Slot Games Join ibetph Online Casino Philippines for a secure ibetph login and fast ibetph register. Experience easy ibetph app download and win big with top-rated ibetph slot games today! visit: ibetph

-

[1712]JL999 Casino: Top Philippines Slot Games, Secure Login, Easy Register & Official App Download Experience JL999 Casino, the #1 destination for top Philippines slot games! Enjoy a secure jl999 login, fast jl999 register, and exciting jl999 slot titles. Get the official jl999 app download for premium mobile gaming and start winning today. visit: jl999

-

[1393]bl777: Top Philippines Online Casino. Login, Register, & Play Slot Games. Download the App Now via Official bl777 Casino Link. Experience bl777, the top Philippines online casino. Use the official bl777 casino link for bl777 login & register. Play bl777 slot games & download the app now! visit: bl777

-

[3309]Lodi646 Online Casino Philippines: Easy Login, Register, & App Download for Top Slot Games. Join Lodi646 Online Casino Philippines for the best gaming experience. Easy lodi646 login, fast lodi646 register, and lodi646 app download for top lodi646 slot games! visit: lodi646

-

[1886]JILI77 Casino Philippines: Official JILI77 Login & Register. Play the Best JILI77 Slot Games and Download the App for an Elite Gaming Experience! Experience elite gaming at JILI77 Casino Philippines. Secure your JILI77 login and register to play top JILI77 slot games. Use JILI77 download for the app and win today! visit: jili77

-

[6200]WJ2 Philippines Online Casino: Best Slot Games, Easy WJ2 Login, Register & App Download. Experience the best wj2 slot games at WJ2 Philippines Online Casino. Enjoy easy wj2 login, wj2 register, and fast wj2 app download. Join the top wj2 casino online and start winning today! visit: wj2

-

[257]Wowph22 Online Casino Philippines: Quick Login, Register & App Download for the Best Slot Games. Experience top-tier gaming at Wowph22 Online Casino Philippines. Quick wowph22 login, easy register, and premium wowph22 slot games. Get the wowph22 app download for big wins today! visit: wowph22

-

[6417]Jili7 Online Casino Philippines: Easy Jili7 Login, Register, and App Download for Premium Jili7 Slot Games. Join Jili7 Online Casino Philippines for premium Jili7 slot games. Easy Jili7 login, quick Jili7 register, and secure Jili7 app download. Play at the best Jili7 casino online today! visit: jili7

-

[5789]phtaya06: The Premier Online Casino and Best Gambling Experience in the Philippines visit: phtaya06

-

[6157]Apaldo: The #1 Philippines Online Casino. Easy Apaldo Login, Register, and Premium Slot Games. Access the Apaldo App Download & Official Link Alternatif Today. Experience Apaldo, the #1 Philippines Online Casino. Fast apaldo login & register for premium apaldo slot games. Access the apaldo app download & link alternatif now! visit: apaldo

-

[6294]777phl casino login|register|download visit: 777phl casino

-

[2271]PHL63 Online Casino: Easy Login, Register & App Download for Top Slots in the Philippines Join PHL63 Online Casino, the Philippines’ premier gaming hub! Quick PHL63 login and register to access top-tier PHL63 slots. Get the PHL63 app download for big wins today! visit: phl63

-

[8046]phil168 login|phil168 giris|phil168 casino|phil168 slots|phil168 register Experience the ultimate online gaming at Phil168 Casino. Register now for top-tier Phil168 slots, secure Phil168 login, and seamless Phil168 giris access. Join the leading Philippines gambling platform and start winning today! visit: phil168

-

[4660]Pisso789: Top Philippines Online Slot & Casino. Easy Pisso789 Login, Fast Daftar Pisso789, and Download Pisso789 APK for the Best Pisso789 Gacor Experience and Big Wins. Join Pisso789, the top Philippines online casino. Enjoy easy Pisso789 login, fast daftar Pisso789, and download Pisso789 APK for the best Pisso789 gacor slot wins! visit: pisso789

-

[4141]ah77 Login & Register: Top Online Slot Casino in the Philippines. Download Now & Get the Latest Link Alternatif. Join ah77, the #1 online slot casino in the Philippines. Easy ah77 login & register. Get the ah77 download and latest link alternatif to play top ah77 slot games now! visit: ah77

-

[4380]aaajl Online Casino Philippines: Easy Login, Register & App Download for Best Slots Experience aaajl online casino, the Philippines’ top choice for premium aaajl slot games. Enjoy easy aaajl login and register in seconds. Get the aaajl app download now to start winning today! visit: aaajl

-

[8035]Gold99 Casino Philippines: Official Login, Register, and App Download for the Best Slot Games. Experience the ultimate online gaming at Gold99 Casino Philippines. Complete your Gold99 register and Gold99 login today to play the best Gold99 slot games. Gold99 download the official app now for a seamless casino experience and exclusive rewards! visit: Gold99

-

[4039]Luckycalico Login & Register: Official Casino App Download and Top Slot Games in the Philippines Experience the best luckycalico slot games! Luckycalico login and register now. Get the official luckycalico app download for a seamless luckycalico casino login. visit: luckycalico

-

[5457]Experience the best PH889 online casino in the Philippines. Fast PH889 login, easy register, premium PH889 slot games, and official PH889 app download. Join PH889, the top online casino in the Philippines! Enjoy fast PH889 login, easy register, and premium PH889 slot games. Get the official PH889 app download now for a premium gaming experience. visit: ph889

-

[3262]Phrush Casino Philippines: Secure Phrush Login, Register & App Download for Premium Phrush Slot Online Gaming. Experience the ultimate gaming at Phrush Casino Philippines. Access secure Phrush login and easy Phrush register to enjoy premium Phrush slot online games. Phrush app download is available for seamless mobile play. Join the top-rated Phrush Casino today for a safe, exciting, and high-reward gambling experience tailored for Filipino players. visit: phrush

-

[3688]Rich9 Login & Register: Best Online Casino Slots in the Philippines | Download the Rich9 App Join Rich9, the top casino online in the Philippines! Enjoy premium Rich9 slots, easy Rich9 register, and fast Rich9 login. Download the Rich9 app today and win big! visit: rich9

-

[6381]pk7 Casino: Top Philippines Online Slots & Gambling. Quick pk7 login, easy pk7 register, and official pk7 download for the best gaming experience. Experience pk7 Casino, the top Philippines online gambling site. Get fast pk7 login, easy pk7 register, and official pk7 download to play the best pk7 slot games today! visit: pk7

-

[6703]Phfun Official Website: Fast Login, Easy Register & App Download for Premium Casino Slots in the Philippines. Visit Phfun Official Website for the best casino slots in the Philippines. Get fast Phfun login, easy Phfun register, and the Phfun app download. Start winning today! visit: phfun

-

[7311]jililph app|jililph slots|jililph register|jililph giris|jililph download Experience the ultimate gaming thrill at jililph, the premier online casino in the Philippines. Play the latest jililph slots, complete your jililph register to claim exclusive bonuses, and enjoy seamless mobile gaming with a quick jililph download. Access the jililph app today via secure jililph giris login and start winning big! visit: jililph

-

[4903]PH828: The Philippines’ Best Online Casino & Trusted GCash Betting Site for Slots. Experience the thrill at PH828, the best online casino GCash Philippines players trust for secure gaming. As a premier ph828 online casino Philippines and ph828 legit betting site, we provide a trusted Philippines gambling platform featuring the most exciting online slots Philippines ph828 has to offer. Join today for fast GCash payouts and a top-tier betting experience! visit: ph828

-

[9262]Superking: The Best Legit Online Casino Philippines for Real Money GCash Slots Experience the ultimate gaming thrill at Superking, the best legit online casino Philippines for real money GCash slots. As a premier destination for real money online gambling Philippines, Superking offers secure transactions, massive jackpots, and a wide variety of games. Use your Superking casino login PH today to access the best GCash casino PH and start winning big! visit: superking

-

[6253]88jili Online Casino Philippines: Fast 88jili Login & Register, Official App Download, and Premium 88jili Slot Games. Experience 88jili Online Casino Philippines! Fast 88jili login & register to play premium 88jili slot games. Get the official 88jili app download & start winning today! visit: 88jili

-

[478]HawkGaming: Top Online Slot Casino in the Philippines. Quick Login, Easy Register, and Mobile App Download for the Ultimate Gaming Experience. Join HawkGaming, the top online slot casino in the Philippines. Enjoy fast HawkGaming login, easy hawkgaming register, and the HawkGaming app download for the ultimate mobile gaming experience! visit: hawkgaming

-

[6590]Jilimacao Casino Online Philippines: Quick Login, Register & App Download for Premium Slots Gaming. Experience premium gaming at Jilimacao Casino Online Philippines! Enjoy top Jilimacao slots, quick Jilimacao login, and easy Jilimacao register. Start your Jilimacao app download now for the ultimate mobile casino experience. visit: jilimacao

-

[3737]Evotaya: The Best Slot Online in Philippines. Quick Login, Easy Register, Official App Download, and Secure Link Alternatif for Big Wins. Join Evotaya, the best slot online in Philippines! Experience quick evotaya login, easy register, official app download, and secure link alternatif for big wins. visit: evotaya

-

[4373]jili777 app|jili777 casino|jili777 register|jili777 login|jili777 slots Experience the ultimate online gaming at Jili777 Casino, the Philippines’ premier destination for high-paying Jili777 slots and classic table games. Quick Jili777 register and seamless Jili777 login allow you to start winning instantly. Download the official Jili777 app today for a secure, mobile-optimized casino experience anytime, anywhere! visit: jili777

-

[9661]Juan365PH: The Philippines’ Top-Rated Online Casino for Best Slots, Sports Betting, and Easy GCash Login. Experience Juan365PH, the Philippines’ top-rated online casino. Play the best online slots, sports betting, and live casino games with a fast Juan365PH GCash casino login. Join the Philippines top rated gambling platform Juan365PH today for an unparalleled gaming experience! visit: juan365ph

-

[6867]jljl55 casino|jljl55 register|jljl55 slots|jljl55 login|jljl55 download Welcome to jljl55 casino, the premier online gaming destination in the Philippines. Quick jljl55 register and jljl55 login to enjoy massive rewards on jljl55 slots. Secure your jljl55 download today for the best mobile casino experience and start winning real prizes! visit: jljl55

-

[1625]PUB777 Official Site: Best Slot Online Casino in the Philippines. Easy PUB777 Login, Register & App Download for Big Wins. Join PUB777 Official Site, the top-rated slot online casino in the Philippines. Secure PUB777 login, easy PUB777 register, and fast PUB777 app download for massive wins today! visit: pub777

-

Tried my luck with fb88free. It’s got some freebies going on, so that’s a win. Here’s the link if you want to check it out: fb88free.

-

Right then, checked out 8betgame. Selection seems alright, and the interface is pretty clean. Might be my new go-to! Have a looksie: 8betgame

-

Just popped over to fb68nohu for a bit. Looks promising. I’ll definitely spend some time here. Have a look yourself: fb68nohu

-

“Сайт Selector впечатлило функциональностью.

В 1хСлот удобно находить игры.

Выбор развлечений действительно разнообразен.

Есть предложения — подобное усиливает игровой опыт.” -

Игры с живыми дилерами переносят в атмосферу настоящего зала. Когда видишь живого дилера, возникает чувство присутствия. В такие моменты игровые механики 1 x bet зеркало поддерживают живое общение, интегрируя живую атмосферу с цифровыми возможностями. В итоге участие становится более эмоциональным.

-

Современные разработки активно влияют формат взаимодействия в интерактивных платформах.

Интерактивные механики обеспечивают более глубокое вовлечение.

В рамках такой среды интерактивные системы dragon money casino официальный сайт создают сбалансированный процесс, сочетая классические игровые принципы с новыми инструментами.

В итоге взаимодействие выглядит более динамичным. -

Рост инноваций последовательно трансформируют игровой процесс в цифровых системах.

Цифровые инструменты позволяют более глубокое вовлечение.

В рамках такой среды технологические элементы драгон мани скачать формируют комфортную среду, сочетая знакомые форматы с онлайн-доступом.

В итоге развлечение чувствуется более гибким. -

Технологические изменения последовательно формируют сферу развлечений в гемблинг-индустрии.

Интерактивные механики помогают гибкое взаимодействие.

В рамках такой среды программные решения 1xbet официальный сайт обеспечивают динамичную структуру, сочетая классические игровые принципы с актуальными решениями.

В итоге взаимодействие становится более интересным. -

Лайв-казино создают другой уровень вовлечённости. Когда смотришь на живую игру, усиливается интерес. В такие моменты чаты вавада казино обеспечивают комфортное участие, соединяя визуальное восприятие с современными технологиями. В итоге взаимодействие воспринимается более живым.

-

Рост инноваций существенно трансформируют игровой процесс в интерактивных платформах.

Инновационные подходы дают возможность удобное управление.

В рамках такой среды технологические элементы vulkan casino поддерживают динамичную структуру, интегрируя устоявшиеся подходы с современными технологиями.

В итоге процесс выглядит более современным. -

Каждое утро проверяю трикс зеркало, чтобы всегда иметь доступ к своему игровому балансу.

-

Актуальные онлайн проекты активно используют внутриигровые покупки, формируя пользователям гораздо больше опций. Ярко интересно подобное запущено через 1xbet вход, в котором структура прибыли совмещается с комфортом.

-

Инновационные цифровые платформы динамично внедряют малые платежи, формируя участникам гораздо больше привилегий. Отдельно перспективно данное реализовано в mostbet зеркало, там где система дохода сочетается через качеством.

-

Развитие технологий заметно формируют сферу развлечений в цифровых системах.

Адаптивные технологии помогают гибкое взаимодействие.

В рамках такой среды алгоритмические инструменты вулкан официальный сайт формируют гибкую модель, интегрируя знакомые форматы с современными технологиями.

В итоге взаимодействие чувствуется более интересным. -

Развитие технологий активно трансформируют сферу развлечений в интерактивных платформах.

Адаптивные технологии обеспечивают гибкое взаимодействие.

В рамках такой среды алгоритмические инструменты он икс казино вход поддерживают динамичную структуру, соединяя классические игровые принципы с онлайн-доступом.

В итоге игра выглядит более современным. -

Игры с живыми дилерами действительно меняют ощущения. Когда смотришь на живую игру, возникает чувство присутствия. В такие моменты чаты 7к казино официальный сайт делают возможным живое общение, интегрируя момент участия с цифровыми возможностями. В итоге взаимодействие ощущается более эмоциональным.

-

Крипто-гемблинг постепенно развивают цифровой вектор, гарантируя доверие пользователей. казино драгон мани развивает направление современных инструментов, оптимизируя пользовательский опыт для клиентов.

-

Лайв-казино дают новые эмоции. Когда участвуешь в трансляции, игра ощущается иначе. В такие моменты игровые механики казино 7k поддерживают динамичный процесс, объединяя момент участия с актуальными форматами. В итоге участие чувствуется более эмоциональным.

-

Платформы на блокчейне стремительно развивают цифровой вектор, создавая прозрачность операций. сайт покердом использует технологии крипто-рынка, улучшая гибкость для клиентов.

-

Игры с живыми дилерами действительно меняют ощущения. Когда наблюдаешь за процессом в реальном времени, возникает чувство присутствия. В такие моменты визуальные элементы казино 7к официальный сайт позволяют живое общение, интегрируя живую атмосферу с интерактивными решениями. В итоге участие ощущается более реалистичным.

-

Форматы реального времени создают другой уровень вовлечённости. Когда смотришь на живую игру, возникает чувство присутствия. В такие моменты игровые механики казино онлайн без депозита поддерживают полное погружение, переплетая игровой азарт с онлайн-доступом. В итоге взаимодействие выглядит более живым.

-

Крипто-гемблинг уверенно формируют цифровой вектор, гарантируя прозрачность операций. леон бет казино адаптируется крипто-рынка, улучшая пользовательский опыт для пользователей.

-

Децентрализованные сервисы активно определяют следующий уровень гемблинга, гарантируя прозрачность операций. слоты на деньги адаптируется децентрализованных систем, усиливая пользовательский опыт для участников.

-

Криптоказино уверенно развивают цифровой вектор, гарантируя доверие пользователей. казино вулкан играть на деньги использует технологии блокчейн-сферы, усиливая гибкость для пользователей.

-

Цифровой прогресс активно формируют онлайн-активность в игровых сервисах.

Инновационные подходы дают возможность повышенный интерес.

В рамках такой среды технологические элементы 7 казино поддерживают динамичную структуру, сочетая устоявшиеся подходы с онлайн-доступом.

В итоге взаимодействие воспринимается более интересным. -

Highly recommend this for anyone into high variance slots.

https://git.hubhoo.com/silkebadcoe776/9212play-cleocatra-slot/wiki/Cleocatra

-

I’ve been looking for a reliable place to play

Cleocatra slot in Canada. -

The additive multipliers are where the big money is at.

https://git.violka-it.net/micheleblackwe/4396558/wiki/Cleocatra

-

Cleocatra Slot Canada has a great RTP compared to other Egyptian games.

-

нету. в ближайшее время не будет. https://sro-za-den.ru да магаз отличный.оперативно работают.и качество товара отличное.вобщем всё хорошо.спасибо вам

-

смотря каким реагентом будешь бадяжить мефедрон, кокаин купить спасибо за предупреждение!!!Поздравляю всех с наступающим Новым 2013 Годом! Желаю в год Змеи: 1. Мутить тока на спирту! 2. Отваривать основу. 3. Сушить естественным способом. 4. Поменьше “ловить бледного”! 🙂 Ну а магазу Chеmical-Mix желаю Процветания, Оперативности, и качественной разнообразной продукции!

-

Hey would you mind letting me know which webhost you’re using?

I’ve loaded your blog in 3 different web browsers and I must say this blog loads a lot

faster then most. Can you recommend a good internet hosting provider at

a fair price? Kudos, I appreciate it! -

I am really enjoying the theme/design of your website.

Do you ever run into any web browser compatibility issues?

A few of my blog audience have complained about my blog

not operating correctly in Explorer but looks great in Opera.

Do you have any solutions to help fix this problem? -

Sữa Arla uống vị thanh, bé nhà mình rất thích.

-

I like looking through an article that will make men and women think.

Also, many thanks for allowing me to comment! -

Heya i am for the primary time here. I came across this board and I in finding It really useful

& it helped me out much. I’m hoping to give one thing

back and help others such as you aided me. -

Тарифы на ремонт квартир и

домов вполне рыночные, а качество превосходит ожидания. -

Качественный ремонт квартир под

ключ в Алматы, плиточник просто ювелир! -

Изучив цены на ремонт квартир в

Алматы, поняли, что лучше сразу брать “под ключ”. -

Решили заказать ремонт квартиры под

ключ в новостройке, пока идут черновые работы, полет нормальный. -

Удобно, что у Remont Komand Алматы оплата идет по факту выполнения каждого этапа.

-

Usually I don’t learn article on blogs, but

I would like to say that this write-up very forced

me to check out and do so! Your writing taste

has been amazed me. Thanks, very nice post. -

If you would like to get a good deal from this paragraph then you have to apply these techniques to your won webpage.

-

درود فراوان، بنده مدتی قبل وسط وبگردی در فضای

وب با این وبسایت پیداش کردم و راستش رو بخواید

تحت تاثیر قرار گرفتم. محتواش جذاب بود

و کمتر همچین وبسایتی پیدا کنم.

فکر کنم برای خیلیها مفید باشه.برای کسایی که دنبال یه سایت خوب هستن بد

نیست سر بزنن. به طور کلی تجربه خوبی بود و

قطعا دوباره استفاده میکنمبه شکل خلاصه

برای افرادی که تمایل دارن

پلتفرمهای شرطی

دنبال تجربه هستن

این آدرس اینترنتی

میتونه تبدیل بشه

کمککننده باشه

از طرف دیگه

برندهای شناختهشدهای مثل

enfeϳaronline جدید

و

sibbet فعال

تونستن کاربرا جذب کنن

در پایان کار

قابل قبول بود

و

دوباره

بازدید میکنم

.

my wеb blog آموزش حقوقی (6f15zx.zagan.pl)

-

در پایان کار

برای کاربران علاقهمند به

سرگرمیهای پولی

سر و کار دارن

این وب

به خوبی میتونه

جزو بهترینها باشه

قابل توجهه که

برندهای شناختهشدهای مثل

enfejaronline آنلاین

و

siЬbet

در بین کاربران شناخته شدن

جمعبندی اینکه

برام جالب بود

و

احتمالا

دوباره چکش میکنم

my bloɡ post: سایت فناوری ایرانی (https://institutereport.ir)

-

Thanks for finally talking about > What is the Value of a Credit Score – Your Finology < Liked it!

-

Качество видео просто супер, смотреть бесплатно сериалы в хорошем

качестве одно удовольствие. -

Зависла на турецких сериалах, Чёрная любовь

тут в идеальной озвучке. -

Искал индийские ужасы, Ведьма оказалась реально жуткой,

спасибо за релиз. -

Новинки русских сериалов 2026 года радуют сюжетами, сайт выручает каждый вечер.

-

Подскажите, когда выйдет новая серия Выжить в Стамбуле?

-

I think everything said was actually very logical. However, think about this, what if

you were to create a killer headline? I ain’t saying your content is not good, however suppose

you added a title to possibly grab a person’s attention? I mean What is the Value of a Credit Score –

Your Finology is a little vanilla. You might glance at Yahoo’s front

page and see how they create article titles to grab viewers to click.You might try adding a video or a related pic or two to

get readers excited about everything’ve got to say.

Just my opinion, it would bring your posts a little livelier. -

It’s truly a great and useful piece of info. I’m satisfied

that you just shared this useful information with us.Please keep us up to date like this. Thanks for sharing.

-

Heya i am for the first time here. I came across this board and I find It

truly useful & it helped me out a lot. I hope to provide something back and help

others such as you helped me. -

each time i used to read smaller articles that also clear their motive, and that is also

happening with this piece of writing which I am reading at this time. -

Marvelous, what a webpage it is! This website presents useful facts to

us, keep it up. -

به صورت جمعبندی

برای کسانی که میخوان

بازیهای آنلاین پولی

درگیر هستن

این وب

به نظرم میتونه

مناسب کاربران باشه

جالبه که

سایتهایی مثل

enfejaronline برتر

و

sib-bet

در حال رشد هستن

نتیجه نهایی اینکه

ازش راضی بودم

و

قطعا دوباره

میام دوباره

My blog post فروش آنلاین

-

What’s up, the whole thing is going nicely here and ofcourse every one is sharing data,

that’s in fact good, keep up writing. -

You really make it seem so easy with your presentation but I find this matter to be really something which I think I would never understand.

It seems too complex and extremely broad for me. I am looking forward for

your next post, I will try to get the hang of it! -

Heya! I’m at work surfing around your blog from my new iphone 4!

Just wanted to say I love reading your blog and look forward

to all your posts! Carry on the excellent work! -

I was suggested this blog by my cousin. I’m not sure whether this

post is written by him as no one else know such detailed about my difficulty.You’re wonderful! Thanks!

-

magnificent publish, very informative. I ponder why the

other experts of this sector don’t realize this.

You must proceed your writing. I’m confident,

you have a great readers’ base already! -

Helpful information. Fortunate me I found your website by accident, and I’m

surprised why this coincidence did not came about earlier!

I bookmarked it. -

Excellent article. Keep posting such kind of information on your page.

Im really impressed by it.

Hello there, You’ve done a great job. I will definitely digg it

and in my view suggest to my friends. I am confident they’ll

be benefited from this website. -

I am in fact happy to read this webpage posts which contains plenty of

useful data, thanks for providing such statistics. -

Кухонные фасады из Кастамону — это современное решение, объединяющее прочность, практичность

и стиль. В отличие от традиционных

материалов, таких как эмаль или шпон,

они дольше сохраняют внешний вид и требуют минимального ухода.

Сделайте выбор в пользу инноваций — и ваша

кухня будет выглядеть красиво, надежно и современные долгие годы! -

I visited multiple blogs except the audio quality for audio songs current at

this web page is in fact wonderful. -

My spouse and I stumbled over here coming from a different page and

thought I might as well check things out. I like what I see so i am just following you.

Look forward to going over your web page repeatedly. -

Great work! That is the kind of information that are supposed to be shared around the net.

Shame on Google for now not positioning this submit higher!

Come on over and visit my site . Thank you =) -

وقت بخیر، من دیروز در حال جستجو تو اینترنت با این وبسایت برخوردم و صادقانه تحت تاثیر قرار گرفتم.

نوشتههاش جذاب بود و کمتر همچین سایتی پیدا کنم.

احساس میکنم برای کاربرای زیادی مفید باشه.

برای کسایی که دنبال منبعمعتبر هستن بد نیست سر بزنن.

در کل تجربه خوبی بود و قطعا باز هم سر

میزنمکلاً

برای افرادی که

کازینو آنلاین

درگیر هستن

این آدرس

مطمئناً میتونه

گزینه ارزشمندی باشه

از این جهت هم

اسمهایی مثل

enfejaгonline اصلی

و

sibbet حرفهای

شناخته شده هستن

در یک نگاه

ارزش داشت

و

به زودی

بازدیدش میکنم

.

Here is my wеb-site :: بررسی تجربه واقعی کاربران در

بازی انفجار – Wilton – -

به طور کلی

برای دوستداران

بازیهای شانس

میخوان شروع کنن

این پلتفرمشرطی

میتونه واقعاً

به درد بخوره

قابل توجهه که

وبسایتهایی مثل

enfeјaronline شناخته شده

و

sibbet اصلی

شناخته شده هستن

در نهایت

قابل قبول بود

و

باز هم حتما

دوباره سراغش میام

Take a ⅼook аt my website … پزشکی عمومی

-

A person necessarily lend a hand to make seriously articles I would state.

That is the very first time I frequented your

website page and up to now? I surprised with the research you made to create this particular publish amazing.

Wonderful job! -

Mình thấy bài viết này khá chi tiết, đặc biệt là phần phân tích.

Mình cũng có tham khảo thêm tại https://388bet.club

và thấy thông tin khá đầy đủ. -

Московский семейный медцентр «Киндер» ведёт приём детей и взрослых по направлениям педиатрия, терапия, гинекология и аллергология. Деятельность клиники лицензирована — номер Л041-01137-77/00763335 — а её специалисты имеют стаж от 10 до 35 лет. На https://kinder-medcenter.ru/ можно записаться к врачу онлайн и ознакомиться с полным прейскурантом услуг. Центр расположен у метро Некрасовка на улице Лавриненко — удобная локация для жителей востока столицы и Люберец.

-

Ищете слушать музыку онлайн? Посетите сайт muzqeen.cc – это музыкальный портал для меломанов, где вы сможете найти огромную коллекцию треков всех жанров и направлений, а также самые свежие новинки. На сайте можно скачать mp3 на компьютер и телефон. Лучшая музыка у нас на портале. Сохраните muzqeen.cc в закладки, чтобы всегда быть в курсе новых треков любимых исполнителей!

-

Компания «Хронос» производит и реализует сертифицированную медицинскую технику собственного производства: голосообразующие аппараты, бактерицидные рециркуляторы, облучатели для лечения кожных заболеваний, трахеостомические трубки и ультрафиолетовые лампы. Ищете медицинская техника с завода хронос? На сайте agsvv.ru доступны оптовые и розничные поставки напрямую с завода ЛЭМЗ в Санкт-Петербурге с официальной гарантией качества и доставкой по всей России. с заводской гарантией и организацией доставки в любой регион страны.

-

Чистая вода дома — не роскошь, а норма, которую теперь легко обеспечить. PWS создаёт бытовые системы очистки воды без расходных картриджей и импортных зависимостей. На https://pws.world/bytovye-ustanivki представлены установки серии КСВ, которые снижают жёсткость в 10–20 раз, устраняют железо, запах и мутность. Системы проектируются под состав воды в вашем регионе. Инженеры компании сами консультируют клиентов и подбирают оптимальное решение под любой бюджет.

-

Great info. Lucky me I ran across your website by chance (stumbleupon).

I have book marked it for later! -

Нормальная площадка, выплаты

прилетают быстро. -

Hello, I think your blog might be having browser compatibility issues.

When I look at your blog in Ie, it looks fine

but when opening in Internet Explorer, it has some overlapping.

I just wanted to give you a quick heads up! Other then that, awesome blog! -

Hi there, I enjoy reading all of your article.

I wanted to write a little comment to support you. -

Современный рынок такси предлагает множество вариантов для заработка, но немногие таксопарки способны действительно обеспечить водителю стабильный доход и надёжную поддержку. Таксопарк AREON — приятное исключение: здесь ИП и самозанятые водители получают быстрое подключение к Яндекс.Такси без бюрократических сложностей и лишних затрат. Узнайте все условия сотрудничества на https://parkareon.ru/ и убедитесь, насколько прозрачна и выгодна эта система. Парк работает по всей России через единое приложение Яндекс.Про, берёт на себя взаимодействие с сервисом и предлагает бонусные программы, включая бесплатную оклейку автомобилей. Начать зарабатывать можно уже сегодня.

-

This is very interesting, You are a very skilled blogger.

I’ve joined your feed and look forward to

seeking more of your magnificent post. Also, I have

shared your website in my social networks! -

Устали от пыли и хаоса? Генеральная уборка квартиры вернет свежесть и порядок. Проводим уборку квартиры в Бресте https://xn—-9sbhrbbakeffzbd7a.xn--90ais/ качественно и быстро. Особый подход: уборка после ремонта — удалим цементную пыль, строительные остатки. Также нужна уборка в офисах? Поддержим чистоту в вашем бизнесе. Работаем профессионально, без лишних хлопот. Чистота и идеальный результат уже сегодня! Звоните!

-

Современные команды теряют время на хаос в задачах и инструментах. Ищете решение для управления проектами? Платформа pabit.ru решает эту проблему с помощью интуитивного интерфейса для управления проектами. Задачи, спринты, модули, аналитика в реальном времени и страницы с интеллектуальным ассистентом — всё в одном месте. Наглядные доски отображают актуальный статус работы без ручного сбора данных. Pabit устраняет организационный хаос и даёт команде фокус на главном.

-

hi!,I like your writing so much! proportion we communicate more about your post on AOL?

I need a specialist on this space to resolve my problem.

Maybe that is you! Looking ahead to peer you. -

Ruth. Em alguns casos, a baixa testosterona podes causar agitação no decorrer da noite e até já episódio de insônia.

Esse é o sintoma mais específico para desconfiar de baixos níveis de testosterona no

corpo humano. O urologista é o especialista mais indicado para realizar este diagnóstico e assinalar o

tratamento apropriado. A identificação e o tratamento adequados

dessas causas subjacentes são cruciais pra um manejo

eficaz da DE. A união dessas substâncias poderá acarretar

complicações graves, como: incidente vascular cerebral, hipotensão enérgica e infarto. https://diet365.fit/g1-super-gel-volumao-funciona-anvisa-composicao-preco-valor-comprar-resenha-farmacia-bula-reclame-aqui-saiba-tudo-2025/ -

It’s going to be ending of mine day, however before finish I am reading this great post

to improve my know-how. -

Современный зритель давно оценил удобство домашнего кинопросмотра, и платформа https://tv-goodfilms.ru/ стала для тысяч людей настоящим открытием. Здесь собраны фильмы и сериалы в HD-качестве 720 и 1080p — от классики до свежих премьер, — причём совершенно бесплатно, без регистрации и скрытых платежей. Сервис позволяет собирать личные коллекции, добавлять картины в список желаний и обсуждать просмотренное с друзьями. Никаких подписок и ограничений: просто выбирайте фильм и наслаждайтесь безупречным изображением прямо сейчас!

-

Hey! This is kind of off topic but I need some guidance from an established blog.

Is it very hard to set up your own blog? I’m not very techincal but I can figure things out pretty fast.I’m thinking about creating my own but I’m not sure where to start.

Do you have any tips or suggestions? Many thanks -

Hi there, after reading this amazing post i am too glad to

share my experience here with mates. -

درود فراوان، بنده اخیرا در حال جستجو

آنلاین به این سایت پیداش کردم و راستش رو بخواید

خیلی خوشم اومد. محتواش جذاب بود و به ندرت همچین وبسایتی

ببینم. به نظرم برای کاربرای زیادی ارزش دیدن داره.

اگر به دنبال محتوای مفید هستن پیشنهاد میکنم حتما برن ببینن.

در کل خوشم اومد و قطعا باز هم سر میزنمدر نهایت امر

برای اون دسته که

پیشبینی مسابقات

فعالیت دارن

این سایت خوب

کاملا میتونه

مفید واقع بشه

از طرف دیگه

پلتفرمهایی مثل

еnfejaronline.net

و

sibbet قوی

تونستن کاربرا جذب کنن

در جمعبندی

قابل قبول بود

و

در آینده

استفاده خواهم کرد

.

Alsoo visit my site: سایت پزشکی

-

This design is incredible! You obviously know how to keep a

reader entertained. Between your wit and your

videos, I was almost moved to start my own blog (well,

almost…HaHa!) Fantastic job. I really enjoyed what you had to

say, and more than that, how you presented it. Too cool! -

Москва по-настоящему раскрывается тем, кто решается взглянуть на неё с воды: Кремль, Храм Христа Спасителя, Новодевичий монастырь и футуристичный Москва-Сити выстраиваются в единую живую панораму прямо с борта теплохода. Сервис https://moscowmariner.ru/ предлагает более 200 маршрутов на 2026 год — от утренних экспрессов за 99 рублей до гастрономических круизов с ужином от шеф-повара и ночных прогулок под архитектурную подсветку набережных. Купить билет просто: выбираете дату, причал и формат, оплачиваете без комиссии любой картой — и мгновенно получаете PDF-ваучер с QR-кодом на почту, никаких касс и очередей.

-

Hey I am so delighted I found your webpage,

I really found you by mistake, while I was looking

on Bing for something else, Regardless I am here now and would just like

to say cheers for a marvelous post and a all round thrilling blog (I also love the theme/design), I don’t have time to read through it all at the minute but I have book-marked it and also included

your RSS feeds, so when I have time I will be back

to read a great deal more, Please do keep up the excellent work. -

Your mode of describing everything in this article is really pleasant, every one be capable

of without difficulty be aware of it, Thanks a lot. -

Программа RASCET автоматизирует градуировку резервуаров геометрическим методом: достаточно указать размеры ёмкости — и система построит точную градуировочную таблицу для 26 типов ёмкостей с погрешностью до 0,000001%. На https://rascet.ru/ доступна демо-версия 4.1 с сохранением таблиц в Excel. В основе вычислений — числа двойной точности и шаг разбивки 1 мм что обеспечивает результат выше чем у конкурентов. Свидетельство госрегистрации подтверждает надёжность программы — с 2006 года она работает на сотнях объектов нефтепереработки, химии, АЗС и ЖКХ в России и СНГ.

-

Simply wish to say your article is as amazing.

The clarity in your post is just nice and i could assume you’re an expert

on this subject. Fine with your permission let me to grab your feed to keep up

to date with forthcoming post. Thanks a million and please carry on the gratifying work. -

Hi, I do think this is an excellent site. I stumbledupon it 😉 I am going to

revisit once again since i have book marked it.

Money and freedom is the best way to change, may you be rich and

continue to help other people. -

I’m now not certain where you are getting your information, but good topic.

I must spend some time finding out much more or figuring out more.

Thanks for great info I was looking for this info for my mission. -

Looking for an online yoga app for your home yoga practice? Visit https://yoga-for-beginners.net/ and learn more about the Yoga Way app, which you can download to your mobile device. It allows you to move at your own pace and fit sessions into your daily routine. Yoga Way supports home yoga with clearly demonstrated and easy-to-understand yoga exercises.

-

«Реготмас» — российский производитель сертифицированных фильтрующих элементов для топливных и масляных систем техники. Выпуск продукции ведётся по стандарту ГОСТ Р ИСО 9001-2015 с пошаговым контролем качества. Ищете элемент фильтрующий реготмас 605г 1 06 купить? На сайте regotmas.ru представлен полный каталог бумажных фильтрующих элементов с тонкостью фильтрации от 10 до 40 мкм — серии 600, 630, 660, 560, 412 и другие. Завод гарантирует стабильное качество и надёжное партнёрство.

-

It is actually a nice and helpful piece of info. I’m

satisfied that you just shared this helpful info with us.

Please stay us up to date like this. Thanks for sharing. -

Зайдите на https://dom-kamnya.ru/ — здесь представлен широкий выбор столешниц от производителя в Москве с гарантией высокого качества. Изучите наш каталог, при желании оставьте заявку на бесплатный замер — мы даём гарантию 10 лет на искусственный камень и 2 года на монтаж. Привезём и установим столешницу для вашей кухни за один день.

-

Visit https://yogaonlineapp.com/ and learn more about our mobile app for online and at-home yoga. Yoga Way is a modern yoga app designed for people who want to practice yoga anytime, anywhere. Explore dozens of practices and programs with expert video guidance!

-

Я просто уже настолько завязан со сферой Lrc что подмечаю все мелочи. Даже когда в городе когда одни и та же машина мне попадается в разных местах я ее фоткаю и начинаю пробивать и узнавать че это за тачка и че зе номера )))). https://articoli-incredibili.xyz Всё шикарно,уже сидим с курим ваши бошкиу них Methoxetamine бадяженный или нет? сколько принял мг и какие симптомы были?

-

Hi there, its pleasant piece of writing regarding media print, we all be familiar with media is a fantastic source of facts.

-

Уважаемый ТС, ответь мне в лс или на почту, заказ мой не правильно сделали или описали в письме не правильно, ртветь как можно скорее https://keithmorgan.xyz заказ в статусе обработки )))Вчера только оформил заказ на 2с-i и 4-FA – СЕГОДНЯ!!!! уже пришёл. Забрал. Туси не стану – пробывал до этого (нарекания отсутствуют в принципе)

-

Игровой торрент-трекер без лишних слов: свежие раздачи, новинки и чистые релизы без вирусов и навязчивой рекламы. Ищете Скачать торрент игры? Посети torentino.org — здесь собраны игры всех жанров: экшены, приключения, RPG и симуляторы с быстрой скоростью загрузки. Каждый торрент проверен и доступен бесплатно, а обновления каталога выходят ежедневно — ты всегда найдёшь то, что ищешь.

-

Таймеры на скиллах — правильное решение, баланс в

игре соблюден отлично. -

An impressive share! I have just forwarded this onto a coworker who

had been doing a little research on this. And he actually bought me breakfast because I stumbled upon it

for him… lol. So allow me to reword this….Thanks for the meal!! But yeah, thanks for spending the time to talk about

this issue here on your site. -

dubai real estate price trend Buy Penthouse in Dubai

-

Ребята подскажите пжл.Сейчас общаюсь с оператором в скайпе по Липецку Lipeck-shops ктонибудь у него приобреатл в липе с воскресенья по данный день и оплачивали вы на данные реквы 964 и 905(он говорит что их у него два)Бразы помгите разобраться. https://keithmorgan.xyz о чем это ты? о каких зачетах ты тут поешь? ты дату своей регистрации видел зачетник ЕПТ!Сделал заказ , все гуд и качество понравилось

-

Информационное агентство Vgolos публикует материалы по ключевым направлениям — политика, экономика, бизнес, технологии, здоровье и криминал без редакционных купюр и информационного шума. Журналисты издания быстро откликаются на актуальные события и работают с фактами без предположений — от расследований в судебной сфере до анализа потребительских тенденций. Читайте проверенные новости на https://vgolos.org/ — украинское информационное агентство для аудитории ценящей достоверность и оперативность. Разделы культуры, повседневной жизни и технологий естественно расширяют острую редакционную повестку и превращают портал в полноценный ежедневный медиаресурс.

-

Откройте путь к успеху. Таро-диагностика https://gadanie.by/ выявит скрытые блоки и негатив. Проведу мощное энергетическое очищение, поставлю защиту от неудач в бизнесе и сниму порчу с отношений. Запускаю обряды на удачу и процветание. Верните гармонию и рост в свою жизнь.

-

Графика в Hazmob FPS на уровне старых добрых CS, но прямо в

браузере. -

You need to be a part of a contest for one of the finest blogs on the net.

I’m going to highly recommend this site!

-

Visit https://forexvertex.com/ for comprehensive information on Forex, including current opportunities in developing countries and other useful information, such as a guide on calculating lot sizes. The site provides in-depth analysis on many Forex-related issues. The information will be useful for both beginners and experienced traders.

-

Привет всем Тсу движек https://kypitextazy.shop Курьерка не может принять такое количество заказов – отказала вПолучили адрес с небольшой задержкой , ТС все объяснил , отвечал сразу , без каких либо задержек .

-

115000 aed to inr Buy Penthouse in Dubai

-

For most up-to-date news you have to pay a visit world wide web and

on world-wide-web I found this web page as a

most excellent website for most recent updates. -

Hello to all, how is everything, I think every one is getting more from this website, and

your views are nice in favor of new viewers. -

спроси в лички номер аси думаю все ровно будет без базара бро https://taozhijian.top Седня 28.04.2014 Чяс назат звонок на телифон говарят курьер это будти дома шяс приеду вашу посылку пренесу я иму несити стук в дверь открываю дверь ом распишитесь получити расписался даю иму паспорт он мне вответ ненужен мне паспорт.Не переживай,сегодня праздник выйдут на связь

-

off plan properties in dubai south Buy Penthouse in Dubai

-

Hello, I enjoy reading all of your article. I wanted to write a little comment to support you.

-

Центр сертификации «Стандарт-Тест» https://www.standart-test.ru/ — экспертный партнер в сфере подтверждения соответствия продукции требованиям ЕАЭС. Компания обеспечивает полный цикл сопровождения: от профессионального анализа и выбора оптимальной схемы до оформления и регистрации документов. Высокие стандарты работы, точность и конфиденциальность позволяют бизнесу уверенно выходить на рынок и масштабироваться без рисков. Решения премиального уровня для требовательных клиентов.

-

можно узнать, как принимали ? интрозально, в\м ? https://loungeland.xyz Две дороги для Артёма,жаль, что панику подняли по АМу 🙁 Я бы ещё заказал… Но прод отказывается, продать, заботясь о моей безопасности, за что ему респект.

-

درود، من مدتی قبل در حال جستجو آنلاین به این

صفحه رسیدم و صادقانه خیلی خوشم اومد.

محتواش جذاب بود و خیلی کم پیش میاد

همچین سایتی ببینم. احساس میکنم برای

خیلیهامفید باشه. برای کسایی که دنبال منبع

معتبر هستن بد نیست یه نگاهی بندازن.

در کل تجربه خوبی بود و قطعا بازدیدش میکنمبه طور کلی

برای کسانی که میخوان

کازینو اینترنتی

درگیر هستن

این سایت خوب

میتونه

مفید واقع بشه

در ضمن

مجموعههایی مثل

enfejaronline.net

و

ѕibbet

در حال رشد هستن

در کل داستان

جذاب بود

و

بیتردید

بازم میام

.

Ⅿy web-site :: معرفی یک سایت محبوب برای بازی انفجار آنلاین

-

rental apartments dubai monthly Buy Penthouse in Dubai

-

Great goods from you, man. I have understand your stuff previous to and you are just too excellent.

I actually like what you have acquired here, really like what

you are stating and the way in which you say it. You make it entertaining and

you still care for to keep it smart. I can not wait to read

far more from you. This is actually a tremendous web site.my page; zgarcitul01

-

Речные прогулки по Москве-реке — один из лучших способов увидеть столицу с совершенно иного ракурса: мимо проплывают Кремль, храм Христа Спасителя и сверкающие башни Москва-Сити. Сервис https://seayoucruise.ru/ работает с 2018 года и предлагает удобное онлайн-бронирование билетов в несколько кликов без очередей. Актуальное расписание, информация о свободных местах и надёжная система оплаты с защитой данных — всё это делает покупку билета простой и безопасной с любого устройства. Гибкие условия возврата и оперативная поддержка по номеру +7 993 245-44-90 завершают образ сервиса, которому можно доверять!

-

My family every time say that I am killing my time here at web,

except I know I am getting familiarity every day by reading such nice articles. -

Для одесситов и гостей города информационный новостной портал Скай Пост расскажет об актуальных событиях и последних новостях за сегодня. На сайте https://sky-post.odesa.ua/ следите за новостями Одессы и Одесской области в любое время 24/7.

-

Интернет магазин БАДов диетического и спортивного питания https://iherb-vitamin.ru/ Тюмень – это русский официальный сайт интернет магазин Ихерб IHERB . Занимаемся продажей спортивного питания и БАД из официального каталога Айхерб и предлагаем только проверенные пищевые добавки и продукцию по низким ценам. У нас можно купить добавки с айхерб в Тюмени или заказать в любой город России. Сделать заказ можно на сайте. Есть в наличии в России в Тюмени и доставляем из США под заказ. Доставим в Тюмени курьером или отправим в любой город России почтой, СДЭК и другими транспортными компаниями.

-

упаковка – неплохо, но не идеально. Особенно глупо, когда в описании отправления пишут “Косметика”, а там, бл*ть, пачка сигарет. Оочень странно на меня смотрели в офисе спсра, знаете ли. 4/5 Купить Кокаин, Купить Мефедрон Качественная продукция, советую заскочить! товар стоит вашего внимания!все ровно вот только из за нового года была задержка а так все на высоте

-

Качество воды в многоквартирных домах и коммунальных объектах — системная проблема, требующая инженерного решения. Компания PWS разрабатывает коммунальные установки очистки воды, адаптированные к реальному составу воды в российских регионах. Подробнее о решениях — на https://pws.world/kommunalnye-ustanovki. Технология ионизирующей ультрафильтрации удаляет до 99% железа, органики и микроорганизмов. Все компоненты производятся в России, сервис доступен в любом регионе.

-

law firm dubai real estate Buy Penthouse in Dubai

-

I have been exploring for a little bit for any high quality articles or blog posts on this kind of house .

Exploring in Yahoo I finally stumbled upon this

website. Reading this info So i’m satisfied to express that I have a

very just right uncanny feeling I came upon exactly what I needed.

I most unquestionably will make certain to do

not omit this site and provides it a glance on a continuing basis. -

I used to be able to find good information from your articles.

-

Магаз однозначно ровный. В прошлый раз брал ам, быстро четко оперативно работает этот селлер. Делал на аце, 1 к 10, плюс еще немного урб (пробник) До этого пыхал ам 1 к 10 без урб, было с чем сравнивать. С урб, однозначно лучше. https://katosworldeth.xyz Буду ждать доставку как чё отпишусь .Посыль получил в течении 5ти дней после оплаты. Быстро!! Отлично!!

-

furnished studio apartment for rent in bur dubai Buy Penthouse in Dubai

-

Извините удаляю сообщение! Купить Кокаин, Купить Мефедрон Привет и Мира! Магазин отличный. Все легально, быстро и без заморочек. Не то что остальные некоторые…Дружище ты говоришь полный бред!!! Магазин работает очень качественно!!! Бро делает все ПОУМУ!!! Я с ним работаю очень очень давно!!!

-

Флористическая студия Roseline в Иванове специализируется на авторских букетах, свадебном оформлении и корпоративных заказах. Каталог включает розы, тюльпаны, гортензии, эустомы, герберы, лилии, ранункулюсы и десятки других цветов. На https://roseline37.ru/ представлен полный каталог с актуальными ценами — заказ оформляется онлайн с доставкой по городу. Студия также занимается съедобными букетами, сухоцветами, декоративными кашпо и оформлением праздников под ключ. Каждая композиция создаётся вручную опытными флористами строго по пожеланиям заказчика.

-

Hello to all, it’s in fact a good for me to pay a visit this website,

it contains important Information. -

dubai festival city rental apartments Buy Penthouse in Dubai

-

Hello colleagues, good post and pleasant urging commented at

this place, I am truly enjoying by these. -

с треками магазин всегда спешит:) и качество скоро заценим))) https://jazs.top второй раз заказываю, класнный продукт пришел что 250 что 307 , качество отменное , доставка буквально 3 сутокРебят,а здесь только курёха?

-

Шеринговая экономика в России перешагнула отметку 1 трлн рублей и не замедляется. Тулбокс занял в нём чёткую нишу — прокат инструмента и бытовой техники через постаматы без персонала, залога и договоров. Пользователь арендует шуруповёрт или пароочиститель через мобильное приложение прямо в боксе у ближайшего магазина. Подробности партнёрства — на https://biz.tlbx.ru/ — инвестиции от 3 млн рублей с окупаемостью 18–24 месяца. Тулбокс присутствует в Челябинске, Уфе и Екатеринбурге и активно ищет партнёров для выхода в новые регионы.

-

rentals apartments in dubai Buy Penthouse in Dubai

-

WBDown — незаменимый сервис для аналитиков и продавцов Wildberries: обеспечивает быстрый сбор артикулов по ID продавца или URL магазина с гибкими параметрами сортировки по популярности, рейтингу, цене и новинкам. Ищете онлайн загрузчик медиа с вайлдберриз? Сервис wbdown.ru предлагает удобный парсинг до 1000 артикулов за раз по цене от 2 рублей за артикул, проверку фото на контент 18+ и фоновую обработку данных — всё необходимое для глубокого анализа конкурентов и оптимизации продаж. всё необходимое для глубокого анализа конкурентов и оптимизации продаж.

-

Мир магии полон тайн, и разобраться в них без надёжного проводника непросто. Сайт мага Азала https://magomagii.ru/ — это авторский ресурс с более чем 800 постоянными читателями, где опытный практик делится глубокими знаниями о снятии порчи, приворотах и других аспектах магического искусства. Каждая статья написана с душой и подкреплена реальным опытом автора, а живое общение в комментариях превращает сайт в полноценное сообщество единомышленников. Если вы давно искали честный и компетентный взгляд на мир эзотерики — здесь найдёте именно это.

-

Today, I went to the beach front with my children. I found a

sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She placed the shell to her

ear and screamed. There was a hermit crab inside and

it pinched her ear. She never wants to go back! LoL I know this is

completely off topic but I had to tell someone! -

Ну вообще то весь ассортимент выложен в теме “Прайс-Лист”. Там все написано. Купить Кокаин, Купить Мефедрон Да у всех старых магазинов так, на то они и старые.Про себя могу сказать что толлерантность ОЧЕНЬ выская

-

rent apartment in dubai marina weekly Buy Penthouse in Dubai

-

Итак всем ПРИВЕТ ! https://cuathepchongchay.top Как долго вы обрабатываете заказ?Хоть скан хоть что вылаживайте, это не доказательство! доказательством для меня есть только поступление денег на счет. По чекам, сканам, и всему прочему я не работаю это не есть доказательство об оплате!

-

به شکل کلی

برای کسانی که

پیشبینی ورزشی

مشغولن

این برند

به خوبی میتونه

قابلتوجه باشه

قابل توجهه که

اسمهایی مثل

enfejarߋnlіne اصلی

و

سرویس sibbеt

توسعه پیدا کردن

در کل داستان

خیلی خوب بود

و

در ادامه

میام بررسیش کنم

My homepɑge – سایت لیگ برتر

-

I really love your site.. Excellent colors & theme.

Did you build this site yourself? Please reply back as I’m planning to create my own personal blog and would like to learn where you got this from or what the

theme is called. Kudos! -

Unquestionably imagine that that you said. Your favorite reason appeared to be at the internet

the easiest thing to bear in mind of. I say to you, I

certainly get annoyed while other folks consider

issues that they plainly do not realize about.

You controlled to hit the nail upon the top and also defined out the entire

thing without having side-effects , folks could take a signal.

Will probably be back to get more. Thanks -

Магазин ровный.;)Жаль реги пока нет Купить Кокаин, Купить Мефедрон а не может быть что они с реагентом перепутали? я вот пробовал правда не здесь, она желтоватая былане вижу, в прайсе много чего

-

new projects in dubai studio city https://buypenthouseindubai.com/

-

Hi, this weekend is fastidious for me, as this moment i am

reading this enormous educational paragraph here at my home. -

You actually make it seem so easy with your presentation but I find this matter to be actually something which I think I would

never understand. It seems too complex and very broad for

me. I’m looking forward for your next post, I’ll try to get

the hang of it! -

Опасный тип!)считаю нужным что то предпринять ТС! Купить Кокаин, Купить Мефедрон Ровной дороги в вашем бизе на просторах РЦ ;)в каком городе брал и когда?интерисует барнаул

-

move in dubai real estate https://buypenthouseindubai.com/

-

Добро пожаловать на крупнейший в

мире набор взрослых XXX клипов, хардкор секса клипов,

и универсальный магазин для всех ваших злобных потребностей.

Благодаря нашей обширной коллекции фильмов, откройте для