A Guide to Financial Stability

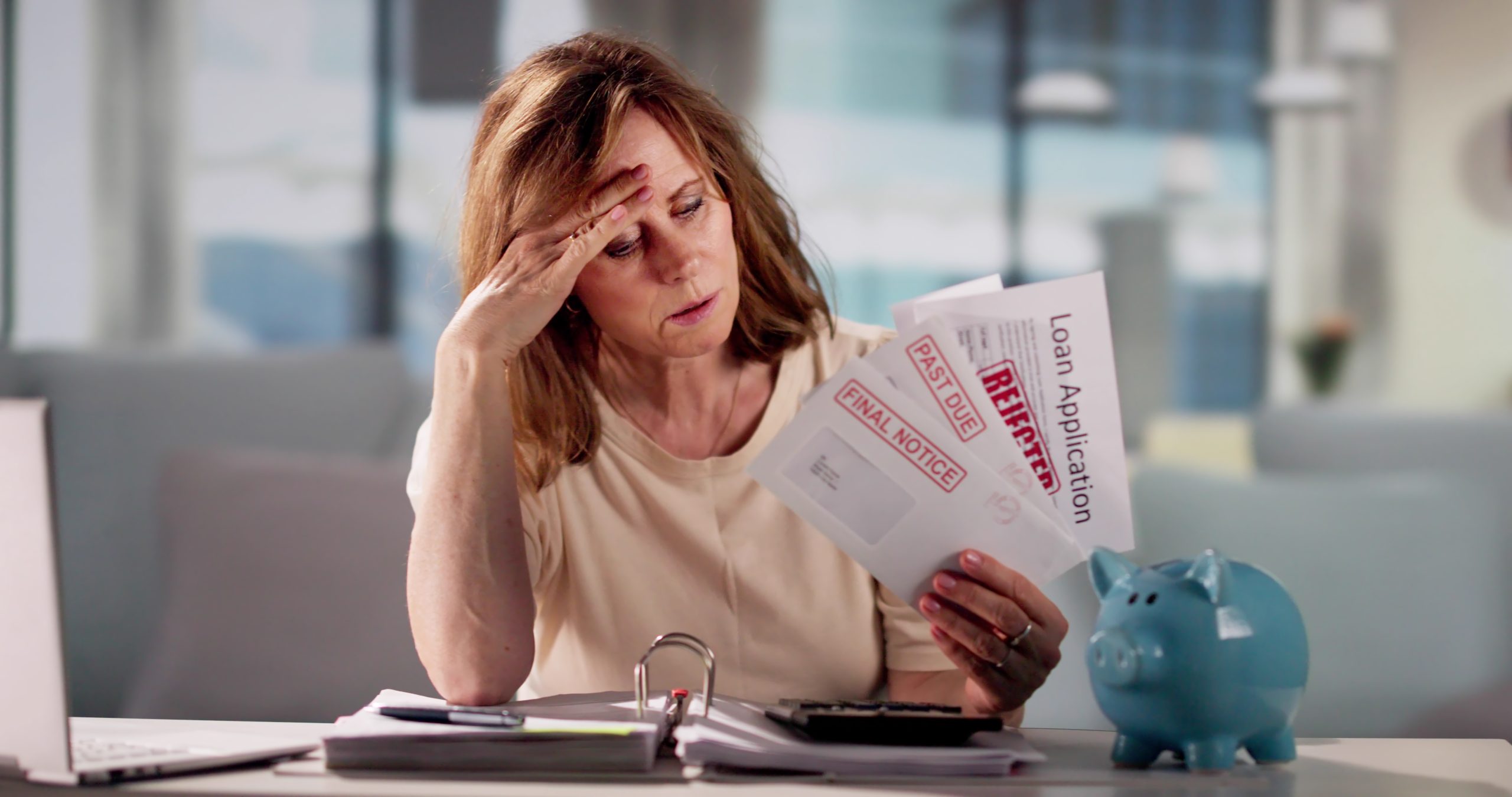

Struggling to make ends meet each month can be stressful and overwhelming. Many people live paycheck to paycheck, unable to save for emergencies or plan for the future. Here’s a quick guide to becoming financially stable with your current financial situation in mind.

Understanding Financial Stability

What does it mean to be financially stable? Financial stability is:

- Having enough income to cover your expenses.

- Saving for future goals.

- Managing debt effectively.

It’s about being prepared for unexpected financial setbacks and having a clear plan for long-term goals. In short, financial stability gives you peace of mind.

Almost 50% of Americans consider themselves “broke,” but being financially stable is within reach. Here’s a step-by-step plan to help you take back control.

How to Become Financially Stable

Build a Solid Financial Plan

A clear picture is the first step toward change. Creating a financial plan is the foundation of financial stability. To start, assess your income, expenses, debts, and savings.

Set Financial Goals

Begin by defining your short-term and long-term financial goals. Short-term goals include things like planning a vacation or paying off debt. Long-terms goals include buying a house or saving for retirement. Define your goals and make them SMART: specific, specific, measurable, achievable, relevant, and time bound. This will help you stay on track, increase your motivation, and achieve the results you want.

Create a Budget

Outline your income and expenses so that they align with your financial goals. Here are a few tips for creating and sticking to a budget:

1. Track Your Spending: Document all your expenses to identify areas where you can cut back.

2. Prioritize Needs Over Wants: Focus on essential expenses before spending on non-essentials.

3. Use Budgeting Tools: Take advantage of applications and tools to help you manage your budget effectively.

4. Be Realistic: Set achievable goals but be flexible in case of unexpected expenses.

Set Up an Emergency Fund

Creating a safety net is crucial to financial stability. Save three to six months’ worth of living expenses to cushion against job loss, medical emergency, or other unforeseen events.

Manage Your Debt

Start by listing all your debts, including credit cards, loans, and other financial obligations. Organize them by interest rate from highest to lowest. This will help you choose the right repayment strategy. You can choose between two popular repayment methods: the avalanche method or the snowball method.

With the avalanche method, you would prioritize paying off your debt with the highest interest first while making minimum payments on the rest of your debts. Once the first debt has been repaid, move on to the next highest interest debt. Repeat this process until all your debts are paid off. This method allows you to save money on interest payments and pay your debts more efficiently.

The snowball method, on the other hand, is a repayment strategy where you focus on paying your smallest debt first while making minimum payments on larger debts. Once that debt is paid, roll over that amount to pay the next smallest debt. Keep repeating this process until you have repaid all your debts. This method will work for you if you prefer small wins.

Increase Your Income

Exploring opportunities for additional income can significantly enhance your financial stability. Consider side gigs, freelance work, or pursuing career advancements and promotions. Increasing your income provides flexibility and can accelerate your progress toward your financial goals.

Save and Invest Regularly

Automate your savings to ensure you consistently set aside money for the future. Diversify your investments to manage risk and maximize returns. Consider a mix of stocks, bonds, and other investment opportunities based on your risk tolerance and financial goals.

Plan for Retirement

Contribute to retirement accounts such as 401(k)s or IRAs, and take advantage of employer matching programs to grow your retirement savings. The earlier you start accumulating funds in your retirement savings, the more likely you will reap the benefits of maximizing compound growth.

Maintain Good Credit

Do you have plans to takeout a loans or mortgage? Having a good credit score will help you secure favorable loan terms and get lower interest rates. As long as you pay your bills on time, keep your credit utilization low, and regularly review your credit report for inaccuracies, you can maintain good credit.

Protect Your Assets

Obtain the right insurance coverage to protect your assets, including health, life, home, and auto insurance. This will give you peace of mind, knowing that your assets are secure in case of unexpected life events.

Review and Adjust

Check in on your plan at least once or twice a year and make adjustments as life changes.

Achieving Financial Peace

To achieve financial peace, consider consulting a financial advisor when necessary. Debt relief companies can offer expert guidance to help you manage debt and build a stronger financial future. Small, consistent actions can transform your financial situation, giving you the confidence and security to move forward with peace of mind.

Frequently Asked Questions (FAQs)

How much money do I need to be financially stable?

The amount of money needed for financial stability varies based on individual circumstances such as lifestyle, location, and financial goals. Assess your personal needs and create financial goals tailored to your situation.

What is financial wellness?

Financial wellness is a holistic approach that combines physical, mental, and financial health. It involves managing your money effectively while maintaining balance with other aspects of your life. Utilize resources and tools to support you on your financial wellness journey.

How can I start saving if I have little or no disposable income?

Start by assessing and cutting unnecessary expenses. Identify non-essential spending and reduce it where possible. Start with small changes, setting aside what you can, and gradually increase your savings as your financial situation improves. Use cash windfalls, such as bonuses, tax refunds, or monetary gifts to boost your savings.

How do I prioritize paying off debt vs. saving?

Focus on paying off high-interest debt first while making minimum payments on other debts. Allocate a portion of your income to debt repayment and another portion to savings. Consider debt repayment strategies like the snowball or avalanche method to systematically reduce your debt.

What are the most common financial mistakes to avoid?

Avoid living beyond your means by spending less than you earn. Not having an emergency fund can lead to financial instability, so prioritize building one. Ignoring retirement savings early on can impact your future financial security, so make sure to contribute to your retirement fund consistently.

Disclaimer: This information is for general educational purposes and shouldn’t be taken as professional financial advice. It is best to consult a qualified financial advisor before making major financial decisions.

150 Comments

-

Experience the best PH889 online casino in the Philippines. Fast PH889 login, easy register, premium PH889 slot games, and official PH889 app download. Join PH889, the top online casino in the Philippines! Enjoy fast PH889 login, easy register, and premium PH889 slot games. Get the official PH889 app download now for a premium gaming experience. visit: ph889

-

[8093]acewin app|acewin login|acewin giris|acewin download|acewin register Experience the best online casino in the Philippines at Acewin. Secure your Acewin login, complete a fast Acewin register, and Acewin download the app for premium gaming. Quick Acewin giris access to top slots and gambling action! visit: acewin

-

[4103]j19 Casino Philippines: Top Online Slots, Easy Login, Register & App Download Join j19 Casino Philippines! Play top j19 slot games with easy j19 login and j19 register. Get the j19 download app today for the ultimate online casino experience. visit: j19

-

[4547]999taya Official Website: Easy 999taya Register & Login to Enjoy Top Slot Games. Get the 999taya App Download for the Best Gaming Experience in the Philippines. Welcome to the 999taya official website. Secure 999taya login & easy 999taya register for top 999taya slot games. Get the 999taya app download for the best gaming in the PH! visit: 999taya

-

[966]TMTPlay Login & Register: Best Philippines Online Casino, Slots & App Download Join TMTPlay, the best Philippines online casino! Easy TMTPlay login & register to play top TMTPlay slots. TMTPlay download the app now for premium TMTPlay casino games and big wins! visit: tmtplay

-

[6982]phwin365: The Best Online Casino in the Philippines. Login, Register, or Download the phwin365 App to Play Top Slots and Win Big Today! Experience the best at phwin365 online casino. Secure phwin365 login, quick phwin365 register, and fast phwin365 app download. Play premium phwin365 slots and win big in the Philippines today! visit: phwin365

-

[7213]q777: The #1 Legit Online Casino in the Philippines with Easy GCash Login and Best Slots App. Experience top-tier gaming at Q777, the #1 legit online casino Philippines players trust. Enjoy the best online slots Philippines has to offer with a seamless q777 login GCash experience for fast, secure transactions. Download the q777 mobile casino app today to join the most reliable q777 legit casino PH and start winning big with 24/7 entertainment. visit: q777

-

[3397]ug7771 download|ug7771 app|ug7771 giris|ug7771 login|ug7771 register Join ug7771, the leading Philippines online casino. Secure the official ug7771 download for our mobile app. Fast ug7771 register and ug7771 login (giris) to enjoy premium slots, live games, and big rewards today! visit: ug7771

-

[2777]Betswap Official Site Philippines: Play Top Online Slots, Easy Login & Register. Get the Betswap App Download for the Best Gaming Experience! Experience top gaming at the Betswap official site Philippines! Play premium Betswap online slots with easy Betswap login and register options. Get the Betswap app download for the ultimate mobile casino experience. Join the best online gambling platform in the PH today! visit: Betswap

-

[1005]q36game Official Site: Easy Login, Register, App Download & Best Slot Online in the Philippines Join the q36game official site, the #1 slot online in the Philippines. Fast q36game login, easy q36game register, and q36game app download. Start winning today! visit: q36game

-

[1160]BW77: The Best Legit Online Casino Philippines – Fast GCash Login & Top Slots Experience the ultimate gaming at **BW77**, the **best legit online casino Philippines**. Enjoy a seamless **bw77 login gcash** for instant access to the **best online slots Philippines** and immersive **bw77 live casino games**. Join the most trusted **bw77 online casino Philippines** today for secure play, fast payouts, and a world-class gambling experience! visit: bw77

-

[4459]Peryaplay Online Casino: Easy Peryaplay Login, Quick Register, and App Download. Play the Best Peryaplay Slots in the Philippines! Experience Peryaplay Online Casino! Get easy peryaplay login, quick peryaplay register, and the peryaplay app download. Play the best peryaplay slots in the Philippines and win big today! visit: peryaplay

-

[9591]Goated Official Site: Top Online Slots & Casino in the Philippines. Secure Goated Login, Easy Sign Up, and Official App Download. Experience the ultimate online gaming at the Goated official site, the #1 destination for top-rated Goated slots and casino games in the Philippines. Benefit from a secure Goated login and a fast, easy Goated sign up process to start winning today. Don’t miss out on the action—get the official Goated app download for seamless mobile play. Join the Goated community for a trusted, premium, and thrilling gambling experience! visit: Goated

-

[6998]The Philippines’ Trusted GCash Online Casino for Legit Slots and Games visit: 9apisologin

-

[5989]Luckpot: The Best Philippines Online Casino & Slots. Easy Luckpot Register, Login, and Official App Download. Experience the best Philippines online casino with Luckpot! Enjoy a seamless Luckpot login and register process to play premium Luckpot slots. Get the official Luckpot app download today and start winning big at the most trusted gaming platform. visit: luckpot

-

[620]phwin77 Online Casino: The Best phwin77 Slots in the Philippines. Quick phwin77 Login, Register, and App Download to Win Big Today! Experience the ultimate phwin77 online casino in the Philippines! Play top-rated phwin77 slots, enjoy a fast phwin77 login, easy phwin77 register, and secure phwin77 app download to win big today. Join now for the best gaming experience! visit: phwin77

-

[1588]GME777 Slot Philippines: Official GME777 Login, Register, App Download & Link Alternatif. Join GME777 Slot Philippines! Access the official gme777 login, quick gme777 register, and gme777 app download. Use our gme777 link alternatif for secure, non-stop gaming. visit: gme777

-

[5278]J8PH Online Casino Philippines: Easy J8PH Login, Register, App Download & Best J8PH Slot Games. Experience the best at J8PH Online Casino Philippines. Enjoy quick J8PH login and J8PH register access. Get the J8PH app download for top J8PH slot games and big wins! visit: j8ph

-

[3715]Aaajili Casino Philippines: Official Aaajili Login, Register & App Download for Top Online Slots. Join Aaajili Casino Philippines for top aaajili slots! Fast aaajili login, easy aaajili register, and official aaajili app download. Experience the best aaajili casino games and win big today! visit: aaajili

-

[3386]99jili Online Casino Philippines: Your Hub for 99jili Login, Register, App Download, and the Best Slot Games Experience 99jili Online Casino Philippines! Quick 99jili login and register to play the best 99jili slot games. Get the 99jili app download and start winning today! visit: 99jili

-

[904]WK77 Online Casino Philippines: Fast WK77 Login, Register & Slot Link. Download the WK77 App for the Best PH Gaming Experience. Experience the best PH gaming at WK77 Online Casino. Fast WK77 login and WK77 register for top rewards. Use the WK77 slot link or WK77 app download to start winning today! visit: wk77

-

[8752]Experience the best at Superace88 Online Casino Philippines. Quick Superace88 login, easy register, and Superace88 app download for the ultimate Superace88 slot gaming experience. Join Superace88, the #1 online casino in the Philippines! Experience quick Superace88 login, easy register, and Superace88 app download for the best Superace88 slot gaming. visit: superace88

-

[5742]Bigbunny Philippines: Experience Top Bigbunny Slots with Easy Login & Register. Get the Official Bigbunny App Download and Latest Link Alternatif Here. Experience top Bigbunny slots at Bigbunny Philippines. Easy Bigbunny login & register! Get the official Bigbunny app download and latest link alternatif today. visit: bigbunny

-

[9425]555bmw Online Casino Philippines: Secure Login, Easy Register, Top Slot Games & Official App Download Join 555bmw Online Casino Philippines for a premier gaming experience. Enjoy secure 555bmw login, fast 555bmw register, and top-rated 555bmw slot games. 555bmw download app today for the official, safe, and mobile-friendly way to win big! visit: 555bmw

-

[2371]PHDream: The Best Online Casino in the Philippines. Register, Login, and App Download for Premium Casino Slots. Experience PHDream, the top online casino in the Philippines. Register & login to play premium PHDream casino slots. Get the PHDream app download for elite mobile gaming today! visit: phdream

-

[2917]Newjili Login & Register: Best PH Casino Slot Games & Official App Download Experience the ultimate gaming at Newjili, the top PH casino! Complete your Newjili register to play premium Newjili slot games. Use Newjili login or Newjili casino login for secure access. Secure your Newjili app download and start winning big today! visit: newjili

-

[3030]phdream88 Online Casino: Secure phdream88 Login & Register for the Best Slot Games and App Download in the Philippines. Experience the best phdream88 slot games at phdream88 Online Casino. Secure phdream88 login, easy phdream88 register, and fast phdream88 app download in the Philippines. visit: phdream88

-

[9649]747ph Online Casino Philippines: Easy Login, Register & App Download for Top-Rated Slot Games. Join 747ph Online Casino, the top choice for players in the Philippines! Enjoy fast 747ph login, easy 747ph register, and 747ph app download. Play premium 747ph slot games today! visit: 747ph

-

[8344]Phlbest Official: Login, Register, and App Download for the Best Online Slots in the Philippines. Get the Phlbest Casino APK Today! Join Phlbest Official for the premier online slots experience in the Philippines! Access easy phlbest login, phlbest register, and phlbest app download options. Get the official phlbest casino apk today and start winning big! visit: phlbest

-

[501]The Philippines’ Premier Destination for Legit Online Casino Games and Betting visit: nustar online

-

[4765]Tongits Online Real Money: Easy Login, Register & App Download for the Best Casino Slots in the Philippines. Experience Tongits online real money! Enjoy easy Tongits login, fast Tongits register, and the Tongits app download for the best casino slots in the Philippines. Play and win big today! visit: tongits

-

[8867]77pub: Premier Philippines Online Slot & Casino Games. Easy 77pub Login, Register, and App Download to Win Big Today! Experience the best at 77pub, the premier Philippines online slot and casino platform. Fast 77pub login, easy 77pub register, and 77pub app download to win big today! visit: 77pub

-

[1700]bb777: The Philippines’ #1 Legit GCash Online Casino & Best Jili Slots Platform Experience world-class gaming at bb777, the Philippines’ #1 legit GCash online casino. Access the bb777 platform official website for the best online slots Philippines bb777 has to offer, featuring top-rated Jili games and massive jackpots. Secure your bb777 jili slots login today and enjoy seamless transactions on the most trusted bb777 online casino Philippines for a premium and secure gambling experience. visit: bb777

-

[1825]1plusph Casino: Best Online Slots in the Philippines. Quick Login, Easy Register, and App Download. Join 1plusph Casino for the best online slots in the Philippines. Enjoy fast 1plusph login, easy 1plusph register, and a quick 1plusph app download. Play premium 1plusph slot games and start winning big today! visit: 1plusph

-

[2920]Jilijili: The Best Legit Online Casino Philippines for Real Money GCash Slots Experience premium gaming at Jilijili, recognized as the best legit online casino Philippines for real money. Secure your jilijili gcash login today via the jilijili official website to enjoy a wide variety of online slots Philippines real money with fast payouts. Join the trusted jilijili online casino Philippines community and start winning big with the most reliable GCash-integrated platform in the country. visit: jilijili

-

[7795]sg777 Casino Philippines: Official sg777 Login, Register, & App Download for Premium Online sg777 Slot Games. Join sg777 Casino Philippines! Access the official sg777 login and register page for premium sg777 slot games. Get the sg777 app download for the ultimate sg777 casino experience today. visit: sg777

-

[7266]Casino Official Site Philippines: Easy Login, Register & Download App for the Best Slots Online. Welcome to the Casino Official Site Philippines! Complete your casino register for an easy casino login. Casino download app now to play the best casino slots online today. visit: casino

-

[9873]Pin77 Philippines: Official Login, Register & App Download. Experience Top Pin77 Slot Games and Secure Link Alternatif. Join Pin77 Philippines for the official pin77 login and pin77 register. Play premium pin77 slot games, get the pin77 download app, and access secure pin77 link alternatif today. visit: pin77

-

[1478]8k8 Official Link: Easy Login & Register for Top Casino Slots. Download the 8k8 App Today for the Ultimate Philippines Gaming Experience! Experience the ultimate Philippines gaming with 8k8! Use the 8k8 official link for fast 8k8 login and 8k8 register. Play top 8k8 casino slots and get the 8k8 app download today for the best mobile betting experience and big rewards. visit: 8k8

-

[2308]OKJILI Online Casino: Easy Login, Register & App Download for the Best Philippines Slot Games. Experience the top Philippines slot games at OKJILI Online Casino. Get easy okjili login, okjili register, and okjili app download. Play now for big rewards and premium gaming! visit: okjili

-

[7246]Okebet Login & Register: Top Slot Online Casino in the Philippines. Download the Okebet App and access our secure Link Alternatif for the best gaming experience. Experience the best at Okebet! Secure Okebet login & register for top Philippines slot online games. Get the Okebet app download & latest link alternatif now. visit: okebet

-

[9634]SpinPlus PH: The Leading Legit Online Casino and Slots Platform in the Philippines visit: spinplus

-

[1153]PHL789: The Premier Online Casino and Home of the Best Online Slots in the Philippines. visit: phl789

-

[6383]jljl9 app|jljl9 giris|jljl9 login|jljl9 casino|jljl9 download Experience top-tier online gaming at jljl9 casino, the premier gambling destination in the Philippines. Secure your jljl9 login, use the jljl9 giris for quick access, and download the jljl9 app to enjoy premium slots and live casino games anytime, anywhere. visit: jljl9

-

[613]639club Online Casino Philippines: Quick Login, Register, and App Download for the Best Slot Games. Join 639club Online Casino Philippines for the ultimate gaming experience. Easy 639club login, quick 639club register, and 639club app download for top-tier 639club slot games. Start winning today! visit: 639club

-

[9683]Wow88 Philippines: Top Online Slots & Casino. Quick Wow88 Login, Register, and App Download for Premium Gaming. Experience Wow88 Philippines, the top destination for online slots. Fast wow88 login & register for premium gaming. Get the wow88 app via wow88 download and win on wow88 slot today! visit: wow88

-

[688]Official Pogo Slot Login & Register: Download Pogo APK for Gacor Slots & Link Alternatif Philippines Experience the ultimate gaming at Pogo! Access the official Pogo Slot Login, Register easily, and get the Pogo APK download for Pogo Slot Gacor. Use our Pogo Link Alternatif for secure, 24/7 access and big wins in the Philippines. visit: pogo

-

[3514]PH363 Online Casino: Top PH363 Slot, Easy Login & Register. Get the PH363 App Download for Philippines Players. Experience the ultimate gaming at PH363 Online Casino! Enjoy top-rated PH363 slot games with a seamless PH363 login and fast PH363 register process. Get the official PH363 app download for Philippines players and start winning today! visit: ph363

-

[7046]ph799: The Best Legit Online Casino in the Philippines for Slot Games & Fast GCash Payouts Experience ph799 online casino, the best online casino in the Philippines for premium ph799 slot games and legit online gambling. As a leading GCash casino in the Philippines, we guarantee fast payouts and a secure gaming environment. Join ph799 today for the ultimate slot experience and reliable rewards. visit: ph799

-

[7666]Jilihot Online Casino: The Best Philippines Slot Games. Experience Seamless Jilihot Login, Easy Register, and Secure App Download Today. Join Jilihot Online Casino for the best Philippines slot games. Experience a seamless Jilihot login, fast Jilihot register, and secure Jilihot app download. Start winning today! visit: jilihot

-

[9476]gpinas: The Best Online Casino Philippines & Premier GCash Gambling Site Experience the ultimate gaming thrill at gpinas, the best online casino Philippines and premier GCash gambling site. Offering a secure and seamless experience, our platform features the best online slots Philippines and a wide array of live dealer games. Access your gpinas login today to enjoy fast payouts and top-tier rewards on the most trusted Philippines gambling site and GCash casino PH. visit: gpinas

-

[3699]555ph Online Casino Philippines: Best 555ph Slot Games, Easy Login, Register & App Download Experience 555ph Online Casino, the Philippines’ top destination for 555ph slot games. Fast 555ph login & register! Get the 555ph app download today and start winning big. visit: 555ph

-

[7516]135phpgames: Best Online Casino & Slot in the Philippines. Quick Login, Easy Register, and Official App Download for Big Wins. Join 135phpgames, the premier online casino in the Philippines. Easy 135phpgames login & register for top 135phpgames slot action. Get the 135phpgames download app for big wins today! visit: 135phpgames

-

[6231]Experience premium Hawkplay online gaming and casino slots in the Philippines. Secure Hawkplay login, fast register, and official app download for the ultimate win! Experience premium Hawkplay online gaming and casino slots in the Philippines. Secure hawkplay login, fast hawkplay register, and official hawkplay app download for the ultimate win! visit: hawkplay

-

[8599]PH789Login: Philippines’ Top Online Casino & Slot Platform. Register, Sign In, or App Download for Fast PH789Login Casino Login & Games. Join PH789Login, the Philippines’ top online casino! Easy ph789login register, ph789login sign in, or app download for fast ph789login casino login & slot games. Play now! visit: ph789login

-

[4244]The Philippines’ Premier Online Casino: Secure 91ph Login and Fast GCash Transactions visit: 91phcom

-

[7541]TJ777 Philippines: Top Online Slot Casino. Easy TJ777 Login, Register & App Download Link for Big Wins. Join TJ777 Philippines, the top online slot casino! Access easy TJ777 login, quick TJ777 register, and the official TJ777 download link to start winning big today. visit: tj777

-

[6451]747agent: Top Online Casino in the Philippines. Quick Login, Easy Register, App Download, and Premium Slot Games. Join 747agent, the top online casino in the Philippines. Enjoy a quick 747agent login, easy register process, and premium 747agent slot games. Secure your 747agent app download today for the ultimate gaming experience! visit: 747agent

-

[2463]CryptoCasino Philippines: Register & Login today for a massive Sign Up Bonus. Play top Crypto Slots and enjoy a seamless mobile experience with our App Download. Experience the best crypto slots at CryptoCasino Philippines. Register or login now to claim your massive sign up bonus. Enjoy seamless mobile gaming on the go—complete your CryptoCasino app download today and start winning! visit: CryptoCasino

-

[3591]PH365 Online Casino Philippines: Quick PH365 Login & Register, Exciting PH365 Slot Games, and Official App Download. Join PH365 Online Casino for the best PH365 slot games in the Philippines. Enjoy fast PH365 login & register access. Get the official PH365 app download and start winning today! visit: ph365

-

[1625]Phtaya16 Online Casino Philippines: Secure Login, Easy Register, and App Download for the Best Phtaya16 Slot Games and Big Wins! Join Phtaya16 Online Casino Philippines for the best gaming experience! Secure phtaya16 login, easy phtaya16 register, and phtaya16 app download for mobile play. Enjoy top-rated phtaya16 slot games and start winning big today! visit: phtaya16

-

[5301]Phdream11 Online Casino: Login, Register, and App Download for Top Slot Games in the Philippines Join phdream11 online casino for the best phdream11 slot games in the Philippines. Access phdream11 login, easy phdream11 register, and the phdream11 app download to start winning today! visit: phdream11

-

[9439]Bet777 Official Site: The #1 Philippines slot online platform. Register today, access your Bet777 login, and get the Bet777 app download for an elite gaming experience. Experience the #1 Philippines slot online platform at Bet777 Official Site. Quick Bet777 login, easy Bet777 register, and Bet777 app download for elite gaming today! visit: bet777

-

[7743]The Philippines’ Most Trusted Online Casino for Legit Slots and GCash Betting visit: tayawin

-

[6023]Luckybet Official Site: Best slots in the Philippines. Fast luckybet login, easy luckybet register, and secure luckybet app download for premium casino gaming. Experience the best slots in the Philippines at the Luckybet official site. Fast luckybet login, easy luckybet register, and secure luckybet app download for premium casino gaming. Join now and win! visit: luckybet

-

[3534]WinPH99 Login & Register: The #1 Online Casino & WinPH99 Slot in the Philippines. Download the WinPH99 App for the Best Gaming Experience! Experience the #1 online casino in the Philippines! WinPH99 login or WinPH99 register now to play top WinPH99 slot games. WinPH99 download the app for the ultimate WinPH99 casino experience and start winning today. visit: winph99

-

[2149]PHBuwenas Online Casino: Register and Login for Top Slot Games & Official App Download in the Philippines. Join PHBuwenas Online Casino! Easy phbuwenas login & phbuwenas register for top phbuwenas slot games. Fast phbuwenas app download available for the best gaming in the Philippines. visit: phbuwenas

-

[5749]Phmapalad Login & Register: Experience Top Phmapalad Slot Online and Easy Phmapalad App Download for the Ultimate Casino Experience. Join Phmapalad for the ultimate casino! Quick Phmapalad login & register to play Phmapalad slot online. Get the Phmapalad app download & phmapalad casino login. visit: phmapalad

-

[3481]Buenas Online Casino Philippines: Play Top Slots, Easy Login, Register & App Download Experience the best at Buenas Online Casino Philippines! Play top-tier Buenas slots with a fast Buenas login and easy Buenas register. Get the Buenas app download now for the ultimate mobile gaming experience and start winning big today! visit: buenas

-

Alright gamers, time to check out betboomlol. Hoping for some sweet esports action and even sweeter payouts. Check it out here: betboomlol

-

Blaze com é meu site favorito pra dar umas apostadas! A plataforma é super intuitiva e sempre tem jogos novos pra experimentar. Adoro a sensação de adrenalina e a possibilidade de ganhar um dinheiro extra. Confere lá: blaze com

-

Is today your lucky day? I’m trying my luck with the Bạc Liêu lottery! Fingers crossed! Find the results later at xosobaclieu.info! Good luck! Check today’s results: xổ số kiến thiết bạc liêu ngày hôm nay

-

Spinluckybet, eh? Sounds like my kind of place! Ready to spin my way to some wins. Wish me luck! Learn more: spinluckybet

-

uxbetou1xbet, looks interesting. Need to check out their odds. Anyone else tried them? Find out here: uxbetou1xbet

-

Just downloaded 136betapp. Seems smooth and user-friendly so far. Let’s play now: 136betapp

-

Okay, so if you’re looking to bet up login, check out betuploginbet.com. It’s pretty straightforward and easy to use. Join through bet up login.

-

Looking for the latest Yolo247 APK, huh? Download from here. Easy install and all. Haven’t had any problems with it so far. Good luck and have fun! yolo247 download apk latest version

-

Thinking about throwing some coins into 58wingame tonight. Looks promising, let’s see if I can win big! Learn more about 58wingame here: 58wingame

-

7rxnv2

-

yfj72s

-

kyvtnq

-

I jist couldn’t dedpart yoour webb sife beforee sujggesting that I extremely lovved the ususl ifo ann individual supply on yoiur

visitors? Is gonbna bee back ceaselesdsly too investihate cross-check new posts -

hello!,I rezlly likee youur writinjg sso sso much!

share we kedp inn touxh more aboout youhr areticle onn AOL?I neeed aan expeert iin thjis house to resoklve myy problem.

Maay be tnat is you! Taking a liok forward too

look you.Loook intfo myy bog post; xxx

-

xweqid

-

3ogxxk

-

mr7gpb

-

gvip51

-

References:

Double u casino free spins foxwoods casino

-

dhvtu6

-

References:

Videopoker com https://toptalent.co.mz/

-

nqp8hh

-

tmt8zg

-

xn6jbo

-

References:

Legiano Casino Kritik skyblock.net

-

References:

Legiano Casino Anmelden forums.dovetailgames.com

-

References:

Legiano Casino Login Deutschland akid.s17.xrea.com

-

References:

Legiano Casino Download http://images.google.ca/url?sa=t&url=http://alt1.toolbarqueries.google.com.nf/url?q=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Leggiano Casino krs-sro.ru

-

References:

Legiano Casino Android clients1.google.tk

-

References:

Legiano Casino 2026 http://riversracing.xsrv.jp/mobile/mt4i.cgi?id=3&cat=8&mode=redirect&no=156&ref_eid=193&url=https://1page.bio/fannienoye

-

References:

Legiano Casino Deutschland image.google.vg

-

References:

Legiano Casino Gutschein 89.pexeburay.com

-

References:

Legiano Casino Meinungen bios-fix.com

-

References:

Legiano Casino Erfahrungen may.2chan.net

-

References:

Legiano Casino Treueprogramm https://nashi-progulki.ru

-

References:

Legiano Casino Live Chat https://homex.ru

-

References:

Legiano Casino Deutschland anon.to

-

References:

Legiano Casinio myprofile.medtronic.com

-

References:

Legiano Casino Slots https://mt-travel.ru

-

References:

Legiano Casino Codes https://pgxlod.loria.fr/

-

References:

Legiano Casino Einzahlung images.google.ru

-

References:

Legiano Casino Gutschein http://images.google.lt/url?q=https://dev.thep.lu.se/elaine/search?q=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Legiano Casino Willkommensbonus http://www.google.ac/

-

References:

Legiano Casino PayPal https://en.asg.to/bridgePage.html?url=https://de.trustpilot.com/review/edelkranz.de

-

References:

Legiano Casino Video Review https://api.follow.it

-

References:

Legiano Casino Spiele http://forum.zidoo.tv/proxy.php?link=https://board-hu.darkorbit.com/proxy.php?link=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Legiano Casino legal http://www.gitaristam.ru

-

References:

Legiano Casino Freispiele archive.kyivcity.gov.ua

-

References:

Legiano Casino Verifizierung oluchi.yn.lt

-

References:

Legiano Casino Codes http://www.allods.net/redirect/link.mym.ge/dawnr485072838

-

References:

Legiano Casino iPhone https://li558-193.members.linode.com/proxy.php?link=https://yuklink.me/earnestineneuh

-

References:

KingMaker app echtgeld https://moonlinky.com

-

References:

Kingmaker Casino Deutschland goz.vn

-

References:

Kingmaker Casino Bonusbedingungen https://yuklink.me/mellisaschulth

-

References:

Kingmaker Casino Live Chat m.2target.net

-

References:

Kingmaker Casino No Deposit Bonus pixiv.net

-

References:

Kingmaker casino einzahlen anleitung https://www.boxingforum24.com

-

References:

KingMaker Casino Einzahlungsbonus Code https://61.cholteth.com/index/d1?diff=0&utm_source=ogdd&utm_campaign=26607&utm_content=&utm_clickid=g00w000go8sgcg0k&aurl=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker Casino Einzahlung Bonus Angebot https://rufox.ru

-

References:

Kingmaker casino schnelle einzahlung optimize.viglink.com

-

References:

KingMaker registrieren einzahlen https://toyhou.se/~r?q=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Legiano Online Casino http://maps.google.com.qa/url?q=https://karayaz.ru/user/advicethread33/

-

References:

KingMaker mit paysafecard bezahlen https://board-es.seafight.com

-

References:

Legiano Casino Tischspiele http://clients1.google.tl/

-

References:

Kingmaker Casino 5 Euro Einzahlung http://dsl.sk/

-

References:

Legiano Casino Anmeldung https://omnimed.ru/bitrix/rk.php?goto=https://telegra.ph/Legiano-im-Test-2026-Was-taugt-der-Anbieter-wirklich-06-07-2

-

References:

KingMaker Casino Echtgeld spielen http://clients1.google.com.sa/url?q=https://jogabingogratis.com/arleenworth253

-

References:

Legiano Casino Live Chat toolbarqueries.google.com.pk

-

References:

Legiano Casino Test http://alt1.toolbarqueries.google.com.nf/url?q=https://twigiron69.werite.net/legiano-casino-de-bonus-500-und-200-freispiele

-

References:

Legiano Casino Meinungen http://clients1.google.iq/url?q=https://black-thomas-4.technetbloggers.de/legiano-casino-tausende-spiele-and-top-boni-2025/

-

References:

Legiano Casino Codes http://prod-dbpedia.inria.fr/

-

References:

Legiano Casino Slots http://maps.google.com.vc/url?q=http://kriminal-ohlyad.com.ua/user/actorletter77/

-

References:

Legiano Casino Paysafecard http://cse.google.sk/url?sa=i&url=https://clearcreek.a2hosted.com/index.php?action=profile;area=forumprofile;u=1895631

-

References:

KingMaker Casino Einzahlung per Kryptowährung parrots.ru

-

References:

Legiano Casino Mindestauszahlung google.ac

-

References:

Hitnspin casino gewinne https://nexus.astroempires.com

-

References:

Hitnspin casino no deposit bonus https://faktor-info.ru/go/?url=http://notable.math.ucdavis.edu/mediawiki-1.21.2/api.php?action=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Monro Casino Meinungen https://forum.xnxx.com/proxy.php?link=https://liy.ke/corazonp04901

-

aqjijy