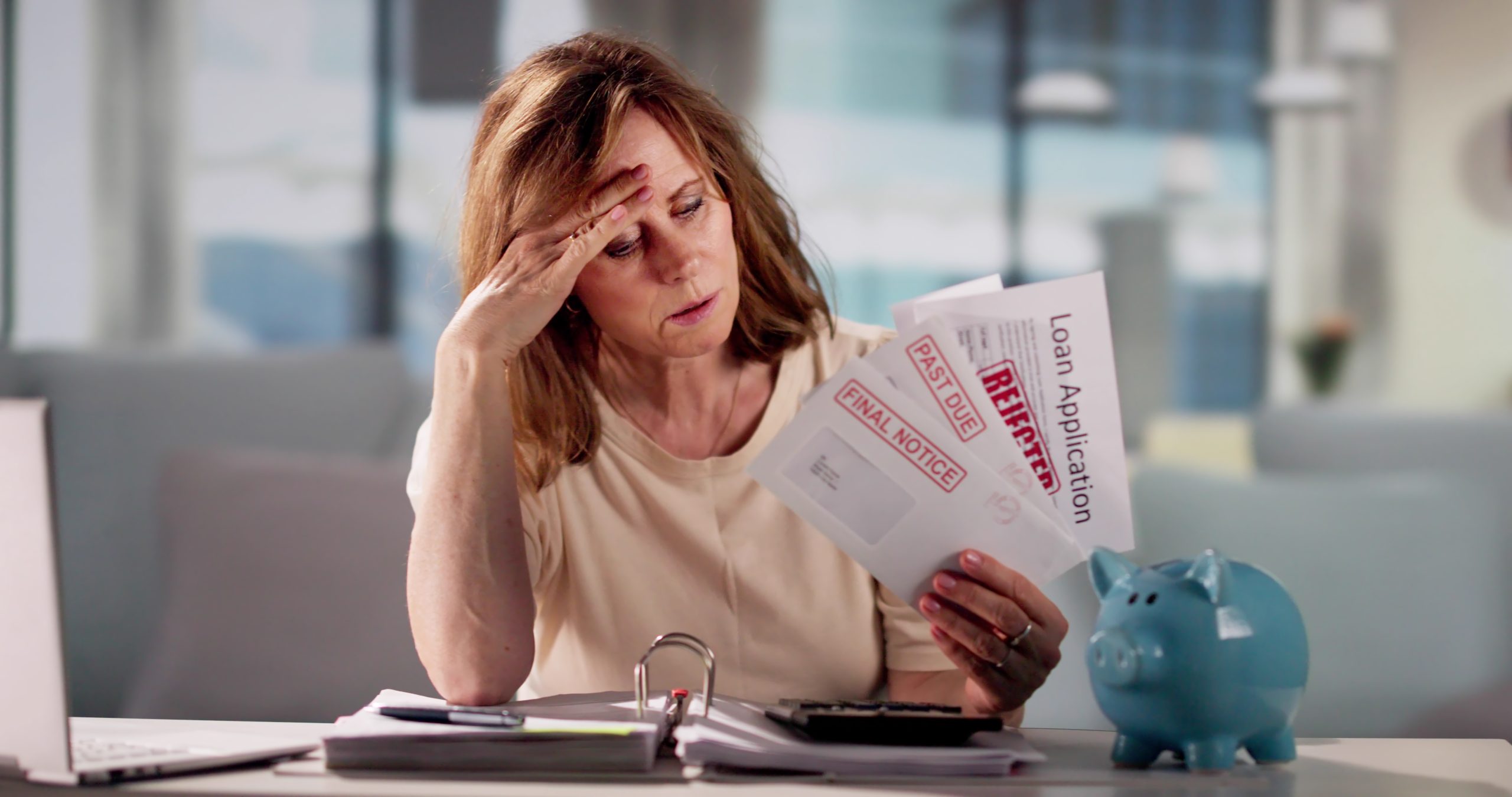

Balance Transfer

Have you tried transferring your credit card balance? A balance transfer can help you manage your finances and save money. It involves moving your debt to a new card with a lower interest rate. This means more of your monthly payment goes towards paying down the actual balance, not just interest. By taking advantage of this strategy, you can save money and get on your debt-free journey much faster.

What Is a Balance Transfer?

A balance transfer is a method of shifting debt from one credit card to another. Many people use balance transfers to make use of a card with a significantly lower promotional interest rate. It’s done by simply opening a new credit card account designed for the best balance credit. It’s important to keep in mind that a balance transfer fee is charged when you move your existing balance to a new credit card. Credit card companies can apply this fee even if you get a zero-percent rate offer.

How To Transfer Credit Card Balance?

Considering a credit card transfer? Here are the main steps to follow:

- Look at your current balance and interest rate: Before making any moves, take a minute to check how much you owe and what interest rate you’re paying. The goal is to find a new card with a lower rate that can cover your balance transfer.

- Find and apply for the right card: Look for a balance transfer card with a 0% intro APR. Some cards apply the 0% rate automatically, while others might require a credit check, so check the details before applying.

- Factor in the transfer fee: Most balance transfers come with a fee, usually between 3% and 5%. Make sure you calculate this upfront and check if there’s a limit on how much you can transfer. You don’t want to transfer more than your new card allows, including fees.

- Start the balance transfer: You can find the balance transfer option in your card account online, in the issuer’s application, or by calling the customer service number on your card. You’ll need to provide details about the debt you’re transferring, such as the issuer’s name, the debt amount, and the account number.

- Complete the balance transfer: There are two ways to complete a balance transfer:

- Balance-transfer checks: Your new card issuer gives you checks to pay off the old card.

- Online or phone transfers: Provide your new card company with the details of your old card, and they’ll handle the payment for you.

- Pay off the balance: Make monthly payments on time once your balance is transferred to the new card.

Pros and Cons of Credit Transfer?

A balance transfer can be a great way to save on interest and pay off debt, but it’s not the perfect fix for everyone. Before you jump in, here are some potential benefits and drawbacks to consider:

Pros:

- Lower Interest Rates: Moving your balance to a card with a lower interest rate helps you pay off your debt faster.

- Potential Savings: You save money by paying less interest than high-interest debt.

- Simplified Debt Management: Combining multiple debts into one, making managing a single monthly payment easier.

Cons:

- Transfer Fees: Some cards could charge a fee for balance transfers, typically 3% to 5%. For example, a $5,000 transfer could cost $150 to $250.

- Temporary Promotional Periods: The lower interest rate may be temporary. After the promotional period ends, higher interest rates may apply to any remaining balance.

- Risk of More Debt: If you don’t pay off the balance during the promotional period or miss payments, you could incur higher interest rates and penalties.

Best Practices

A balance transfer can be a powerful way to manage debt, but you’ll need a smart approach to make the most of it. Here are some key best practices to keep in mind:

- Have a clear plan: Before transferring your balance, decide how you’ll pay it off within the promotional period. This helps you avoid surprise interest charges later.

- Pay more than the minimum: Just because the interest is lower doesn’t mean you should slow down payments. Paying more than the minimum helps you clear your debt faster. You can also consider enrolling with a trusted debt relief program that helps you structure your payments more effectively, reduce what you owe, and stay on track toward becoming debt-free sooner.

- Check the fine print: Look out for transfer fees, interest rates after the promo period, and any terms that might impact your repayment plan.

- Avoid adding new debt: Try not to use your old or new card for additional spending until you’ve paid off your transferred balance. Otherwise, you could end up in more debt.

- Mark transfer deadlines: Many balance transfer offers have a time limit for completing the transfer and qualifying for the low interest rate. Set reminders so you don’t miss out.

- Use the transfer strategically: Balance transfers work best when paired with a disciplined budget. Make a plan to keep your spending in check and stay on track financially.

By following these steps, you can use a balance transfer to your advantage and make better decisions.

Common Mistakes to Avoid

Before you officially begin a balance transfer, take some time to familiarize yourself with all the details. This way, you can avoid potential mistakes and ensure a smooth process.

Here are some key mistakes to watch out for:

- Same Issuer Transfers: You can’t transfer balances between cards from the same bank. Make sure to pick a different bank for your balance transfer.

- Missing Transfer Deadlines: Complete your balance transfer within the specified deadline to get the introductory low APR offer. Use reminders to keep track.

- Overestimating Transfer Limits: Check the new card’s credit limit.

- Paying Only the Minimum: Aim to pay more than the minimum to ensure you pay off your balance within the promotional period.

- Continuing to Spend: Avoid using your old or new card for new purchases until your debt is under control to prevent accumulating more debt.

- Lack of a Debt Plan: To avoid falling into more debt, have a solid plan to manage your debt, including a budget and regular payments.

A well-executed transfer plan might save you plenty! By understanding the advantages and being aware of the pitfalls, you can turn this strategy into a powerful tool for debt relief.

Disclaimer: The information provided in this article is for general informational purposes only and is not intended as legal, financial, or professional advice. We do not guarantee any specific outcomes, and results may vary based on individual circumstances. We comply with all applicable laws, including the California Debt Settlement Services Act, and recommends consulting with an attorney or financial advisor before making any financial decisions. We are not responsible for the accuracy of external links or content, and all website content is protected by copyright laws. We reserve the right to update or remove content at any time without notice.

Frequently Asked Questions (FAQs)

Do balance transfers hurt your credit?

Balance transfers can slightly lower your credit score due to the hard credit check required for approval. Every hard inquiry can reduce your score by a few points. However, improving your credit utilization ratio could benefit your score if the balance transfer improves your credit utilization ratio. The key is to avoid accumulating new balances on your old cards once you’ve transferred the debt to a new card.

Why would a bank deny a balance transfer?

A balance transfer request may be denied if the desired transfer amount exceeds your available credit limit, if your account has a history of negative activity, or if you attempt to transfer a balance to a card issued by the same company as your current card.

Is it better to do a balance transfer or pay off?

It really depends on where you stand financially. If you can afford to pay off your balance in full, that’s always the best option, it clears your debt, frees up cash, and can even boost your credit score. But let’s be real, that’s not doable for everyone. A balance transfer can be useful if your current card has high interest, and you need more time to pay it off. By moving your balance to a card with a lower (or 0%) interest rate, you can save money and pay down your debt faster.

Can I transfer balances between multiple cards?

Yes, you can transfer balances from multiple cards to a single new card, as long as your new card has a credit limit high enough to cover the total transfer amount (plus any transfer fees). Just keep in mind that most credit card issuers won’t let you transfer balances between their own cards. Also, remember that each transfer might come with a fee, typically between 3% to 5%.

If you’re consolidating multiple balances, make sure you’re doing it to simplify payments and save on interest, not just shifting debt around. And once the transfer is complete, avoid racking up new balances on your old cards, or you’ll be right back where you started.

Before you go ahead, take a moment to compare your options. Some balance transfer cards offer a 0% introductory APR for a limited time, usually between 12 to 18 months, which can give you a real break from interest and help you pay down what you owe faster. But once that period ends, the rate can jump significantly, so plan to pay off as much as you can during that window. It’s also worth checking your credit score before applying since balance transfer cards with the best terms are usually offered to those with good to excellent credit.

How do balance transfers affect my credit utilization ratio?

A balance transfer can enhance your credit utilization ratio if executed properly. The credit utilization ratio represents the portion of your total credit limit that you are using, and it significantly impacts your credit score.

Here’s how it works:

- If you open a new card for the balance transfer and keep your old accounts open, your total available credit increases, which can lower your overall utilization ratio (a good thing for your credit score!).

- However, if you max out your new card by transferring a large balance, your utilization on that card could be high, which may temporarily impact your score.

- The key is to keep your old credit lines open (even with a zero balance) and avoid running up new debt.

If you’re using the balance transfer to pay down debt and not just move it around, it can be a smart way to improve your financial situation, and potentially boost your credit over time.

147 Comments

-

Lodi646 Online Casino Philippines: Easy Login, Register, & App Download for Top Slot Games. Join Lodi646 Online Casino Philippines for the best gaming experience. Easy lodi646 login, fast lodi646 register, and lodi646 app download for top lodi646 slot games! visit: lodi646

-

[373]Luckycalico Login & Register: Official Casino App Download and Top Slot Games in the Philippines Experience the best luckycalico slot games! Luckycalico login and register now. Get the official luckycalico app download for a seamless luckycalico casino login. visit: luckycalico

-

[9275]KKKJILI16 Online Casino Philippines: Easy Register & Login to Play Top Slots. Download the App for Big Wins! Join KKKJILI16 Online Casino Philippines! Easy KKKJILI16 register & login to play top KKKJILI16 slots. Download the app for big wins and 24/7 gaming action today! visit: kkkjili16

-

[2784]Jiliglory Online Casino Philippines: Secure Jiliglory Login, Register & App Download. Play the Best Jiliglory Slots & Win Big Today! Experience Jiliglory Online Casino Philippines. Secure Jiliglory login, easy Jiliglory register, and Jiliglory app download. Play top Jiliglory slots and win big today at the most trusted online casino! visit: jiliglory

-

[844]Oklaro Philippines: The Ultimate Online Slot Destination. Register & Login now, Download the App, or access our official Link Alternatif for the best gaming experience! Experience Oklaro Philippines, the ultimate online slot destination! Secure your Oklaro login & Oklaro register today for top Oklaro slot games. Oklaro download the mobile app or use our official link alternatif for 24/7 gaming action. visit: oklaro

-

[2076]Casinoplusph Official Website: Easy Login & Register for the Best Online Slots in the Philippines. App Download available for 24/7 gaming! Experience the best online slots at the Casinoplusph official website. Quick Casinoplusph login & register for top PH gaming. Get the Casinoplusph app download now! visit: casinoplusph

-

[9549]5gjili: The Leading Philippines Online Casino. Fast 5gjili Login, Register, and App Download for Premium Slot Games. Join 5gjili, the premier Philippines online casino! Experience fast 5gjili login, easy 5gjili register, and 5gjili app download for premium 5gjili slot games and big wins today. visit: 5gjili

-

[1996]Milyon888 Casino Philippines: Login & Register to Play Top Slots – Download the App for Big Wins! Join Milyon888 Casino Philippines! Milyon888 register or login to play top Milyon888 slot games. Milyon888 download the app now for big wins and premium casino fun. visit: milyon888

-

[9285]Jili88 Online Casino Philippines: Easy Jili88 Login, Register, & Play Jili88 Slot – Official App Download Experience the ultimate Jili88 Online Casino Philippines! Enjoy a seamless Jili88 login and quick Jili88 register process to play top-rated Jili88 slot games. Secure your Jili88 app download today for the official mobile gaming experience. Join the leading Jili88 online casino in the Philippines for big wins, secure payouts, and exclusive bonuses! visit: jili88

-

[6970]Luxebet88: The Philippines’ Best GCash Online Casino & Top Rated Legit Slots Site. Experience Luxebet88, the Philippines’ best GCash online casino and top-rated betting site. Access the Luxebet88 official login for legit online slots and premium online gambling PH. Join the most trusted and secure platform for the ultimate gaming experience today! visit: luxebet88

-

[4670]Foxgame Philippines: Best Foxgame Slot Platform. Fast Foxgame Login & Register. Get the Foxgame Download and Foxgame APK for Mobile Gaming. Experience Foxgame Philippines, the top Foxgame slot platform. Fast Foxgame login & register for instant play. Get the Foxgame download & Foxgame APK for mobile gaming. Join now! visit: foxgame

-

[6582]Jili90: The Best Online Casino Philippines for Jili Slot Games and Easy GCash Cashouts. Jili90 is the best online casino Philippines for top-tier Jili slot games. Enjoy fast GCash online casino PH cashouts and the best online gambling Philippines experience today! visit: jili90

-

[7576]PinoyTime Casino Online: Quick Login, Register & App Download for the Best Slots in the Philippines. Join PinoyTime Casino Online for the best slots in the Philippines. Quick PinoyTime login, register fast, and get the PinoyTime app download to start winning now! visit: pinoytime

-

[8094]WinPH99 Login & Register: The #1 Online Casino & WinPH99 Slot in the Philippines. Download the WinPH99 App for the Best Gaming Experience! Experience the #1 online casino in the Philippines! WinPH99 login or WinPH99 register now to play top WinPH99 slot games. WinPH99 download the app for the ultimate WinPH99 casino experience and start winning today. visit: winph99

-

[7615]phwin99 Online Casino Philippines: Fast phwin99 Login, Register, & App Download. Experience the Best phwin99 Slot Games Today! Join phwin99 online casino, the premier gaming destination in the Philippines. Enjoy fast phwin99 login, easy phwin99 register, and phwin99 app download. Play the best phwin99 slot games and win big today! visit: phwin99

-

[5429]byu777 Online Casino Philippines: Easy Login, Fast Registration, & Best Slots. Download the byu777 App Today! **Title Tag:** byu777 Online Casino Philippines | Easy Login, Best Slots & App Download

**Meta Description:**

Experience the thrill of byu777 Online Casino Philippines! Enjoy a seamless byu777 login, fast byu777 register process, and the highest-paying byu777 slot games. Secure your wins and get the byu777 app download today for the ultimate mobile gaming experience. Join the #1 trusted online casino in the Philippines now!**H1 Heading:**

Welcome to byu777 Online Casino Philippines – Your Premier Destination for Slots & Big Wins**SEO Content Snippet:**

Looking for the best gaming experience in the Philippines? **byu777 online casino** offers an unparalleled selection of premium games and secure services. Whether you are looking for a quick **byu777 login** to access your favorite titles or need to complete your **byu777 register** to start your journey, our platform ensures a smooth and user-friendly interface. Explore the most exciting **byu777 slot** machines with massive jackpots and high RTP. Don’t miss out on the action—get the **byu777 app download** for Android or iOS and play anytime, anywhere! visit: byu777 -

[2549]PHPark Official Site: Best Slots in the Philippines. Login, Register, & App Download Now. Experience PHPark, the official site for the best slots in the Philippines. Secure your phpark login, complete your phpark register, and get the phpark app download now to start winning on premium phpark slots! visit: phpark

-

[1281]Fairspin Philippines: Top Online Slots, Easy Login, Register & App Download with Exclusive Casino Bonuses. Experience top online slots at Fairspin Philippines. Quick fairspin login, fairspin register & app download. Claim your exclusive fairspin casino bonus today! visit: fairspin

-

[7421]Phswerte Online Casino Philippines: Quick Login, Easy Register, Top Slots, and App Download for the Ultimate Gaming Experience. Experience Phswerte Online Casino Philippines! Enjoy quick phswerte login, easy phswerte register, and top phswerte slots. Get the phswerte app download for the ultimate gaming experience today. visit: phswerte

-

[3216]9awin Philippines: Official Link for 9awin Login, Register, App Download & Top Slot Online Games. Join 9awin Philippines! Access the 9awin official link for 9awin login & 9awin register. Play top 9awin slot online games and get the 9awin app download today! visit: 9awin

-

[9922]pesoBet Online Casino Philippines: The Best Online Gambling Site for Real Money Slots, Sports Betting, and Fast GCash Login. Experience pesoBet online casino Philippines, the best online gambling site for real money online slots and sports betting PH. Fast pesoBet GCash casino login! visit: pesoBet

-

[5384]jl4 Casino Philippines: Best jl4 Slot Games, Easy jl4 Login, Register & Official jl4 App Download. Join jl4 Casino Philippines! Enjoy easy jl4 login, fast jl4 register, and the best jl4 slot games. Get the official jl4 app download today for premium casino action. visit: jl4

-

[4008]PHCity Online Casino: Best Philippines Slots, Easy Login, Register & App Download Join PHCity Online Casino for the best phcity slots in the Philippines. Enjoy secure phcity login, fast phcity register, and the official phcity app download for a premium gaming experience. visit: phcity

-

[6921]55jl Casino Philippines: Best Online Slots, Easy 55jl Login, Register & Official App Download. Experience the best online slots at 55jl Casino Philippines! Enjoy a seamless 55jl login, quick 55jl register, and the official 55jl app download for 24/7 gaming. Play your favorite 55jl slot games and win big today! visit: 55jl

-

[473]Jilivs Casino Philippines: Jilivs Login, Register & Play Jilivs Slot – Official App Download Experience Jilivs Casino Philippines! Complete your Jilivs login or register today to play top-tier Jilivs slot games. Get the official Jilivs download app and win big! visit: jilivs

-

[4636]KingPH Online Casino Philippines: Experience top-tier slot games. Secure KingPH login, quick register, and official KingPH app download for the ultimate gaming experience. Join KingPH Online Casino Philippines for premium KingPH slot games. Experience a secure KingPH login, fast KingPH register, and official KingPH app download today! visit: kingph

-

[6455]S5Casino Official Site: Top Philippines Slots, Easy Login, Register & App Download Visit the S5Casino official site, the top choice for Philippines slots. Enjoy a fast s5casino login and register process. Get the s5casino app download to play today! visit: s5casino

-

[3072]a45 Casino: Best Philippines Slot Online. Easy a45 Login, Register & Official App Download. Experience the best Philippines slot online at a45 Casino! Enjoy easy a45 login, fast a45 register, and the official a45 app download. Play at the top-rated a45 casino now. visit: a45

-

[4594]22Win: The Best Online Casino in the Philippines. Quick 22Win Login & Register to Enjoy Premium 22Win Slot Games. Get the 22Win App Download Now! Join 22Win, the best online casino in the Philippines! Easy 22Win login & register for top 22Win slot games. Start winning & get the 22Win app download now! visit: 22Win

-

[3091]Nustargame Official Site: Top Slots in the Philippines. Login, Register, and App Download Now! Welcome to Nustargame Official Site, the home of top slots in the Philippines. Quick nustargame login and register. Get the nustargame app download to play now! visit: nustargame

-

[1825]Spintime Casino Philippines: Top Online Slots, Easy Login, Register & Official App Download. Join Spintime Casino Philippines for the best online slots! Experience easy Spintime login and register options. Get the official Spintime app download to win big today! visit: spintime

-

[4210]aaaaph Online Casino Philippines: Top Slot Games, Easy Login, Register & Official App Download Join aaaaph Online Casino Philippines for top aaaaph slot games. Experience quick aaaaph login and easy aaaaph register. Secure your win with the official aaaaph app download today! visit: aaaaph

-

[2389]wwin Login & Register: Best Philippines Slots Online, Official Casino Link & wwin App Download. Experience the best Philippines slots online at wwin. Use the official wwin casino link for easy wwin login & register. Start your wwin app download to win big today! visit: wwin

-

[302]Masaya365: The Best Online Casino in the Philippines. Quick Masaya365 login, register, and sign up. Experience top Masaya365 slot games and easy app download today! Join Masaya365, the best online casino in the Philippines! Enjoy quick Masaya365 login, register, and sign up to play top Masaya365 slot games. Experience seamless gaming with our easy Masaya365 app download today. visit: masaya365

-

[7971]TG77 Casino: Best Online Slot Games in the Philippines. Login, register, and download the TG77 app today for exclusive rewards. Experience the best TG77 slot games at TG77 Casino Philippines. TG77 login or register now for exclusive rewards. TG77 download the app today and start winning! visit: tg77

-

[4004]Axiebet88: Best Philippines Online Slot & Casino. Easy Register, Secure Login, and Official App Download via Link Alternatif. Join Axiebet88, the top Philippines online slot and casino. Enjoy easy axiebet88 register, secure login, and the official axiebet88 download via link alternatif. Play now! visit: axiebet88

-

[3491]phgaming casino|phgaming slots|phgaming download|phgaming app|phgaming register Experience top-tier online gaming at **PHGaming Casino**, the Philippines’ leading platform for premium **PHGaming slots** and live dealer games. **Register** at **PHGaming** today or perform a quick **PHGaming download** to access our mobile **PHGaming app** for non-stop action and big wins anytime, anywhere. visit: phgaming

-

[2446]SSBET777 Online Casino Philippines: Easy Login, Register, & App Download for the Best Slot Games. Join SSBET777 Online Casino Philippines! Fast ssbet777 login & register to play the best ssbet777 slot games. Get the ssbet777 app download and win big today! visit: ssbet777

-

[2638]Jili666 Online Casino Philippines: Quick Login, Register & App Download for the Best Slot Games Join Jili666 Online Casino Philippines! Fast jili666 login, easy jili666 register, and official jili666 app download for the best jili666 slot games. Play and win big today! visit: jili666

-

[5545]Beeph Official Casino: Secure Beeph Login, Register & Top Beeph Slot Online. Get the Beeph App Download Today! Join Beeph Official Casino for the ultimate gaming experience in the Philippines. Secure Beeph login, easy Beeph register, and premium Beeph slot online titles await. Get the Beeph app download today to win big! visit: beeph

-

[3934]NN777 Casino Philippines: Best Slots, Fast Login, Register & App Download Experience the best of NN777 Casino Philippines! Play top-rated nn777 slot games with fast nn777 login and easy nn777 register. Get the nn777 download app now for 24/7 casino action. visit: nn777

-

[970]Phcrown Official Site: Easy Phcrown Login, Fast Register & App Download for the Best Philippines Slot Games. Visit the Phcrown official site for the best Philippines slot games. Enjoy easy phcrown login, fast phcrown register, and a quick phcrown app download. Play now! visit: phcrown

-

[2065]Kkkkph Casino Philippines: Top Slots & Online Gaming. Quick Kkkkph Login, Register Today, and Get the Kkkkph App Download for the Best Casino Experience. Experience Kkkkph Casino Philippines! Fast kkkkph login & kkkkph register to play top kkkkph slots. Get the kkkkph app download for the best mobile casino gaming today! visit: kkkkph

-

[3928]Peryagame Online Casino Philippines: Easy Register, Login & App Download for the Best Peryagame Slots Experience. Join Peryagame Online Casino Philippines for the ultimate gaming experience! Quick Peryagame register, easy Peryagame login, and fast Peryagame app download for the best Peryagame slots. Experience the top-rated Peryagame online casino and start winning today! visit: peryagame

-

[2297]Luckygame Casino Online Philippines: Fast Luckygame Login & Register to Play Top Luckygame Slots. Get the Official Luckygame App Download Today! Experience the best at Luckygame Casino Online Philippines! Fast Luckygame login & register to play top Luckygame slots. Secure Luckygame app download now for big wins! visit: luckygame

-

[2222]JL88 Official Site: Top Online Slots in the Philippines. Quick JL88 Login, Easy Register & JL88 App Download for Non-Stop Action. Join the JL88 Official Site, the top choice for online slots in the Philippines. Quick jl88 login, easy jl88 register & jl88 app download for non-stop jl88 slot action. visit: jl88

-

[930]JLPH Casino: Official PH Login, Register, Slot Games & App Download Join JLPH Casino, the top choice for PH players. Easy jlph login & jlph register to play premium jlph slot games. Get the jlph app download for elite jlph casino action! visit: jlph

-

[9226]JLJL44 Official Link: Best Slot Online in Philippines. Login, Register, and Download App to Win Today! Visit the jljl44 official link for the best slot online in Philippines. Complete your jljl44 login or jljl44 register today. jljl44 download app and win now! visit: jljl44

-

[9736]FC188: The Best Online Casino Philippines for Legit Slot Games and Fast GCash Payouts. Experience the ultimate online gambling Philippines at FC188 Online Casino. As the best online casino Philippines, we offer a massive selection of FC188 legit slot games and lightning-fast GCash online casino Philippines payouts. Join today for a secure, fair, and thrilling gaming experience! visit: fc188

-

[3811]HouseofLuck Philippines: Best Slots, Easy Login, Register, and Official Casino App Download. Experience the best HouseofLuck slots in the Philippines! Fast houseofluck login, easy houseofluck register, and official houseofluck casino app download. Play now! visit: houseofluck

-

[416]Experience the best at 777pnl, the top online casino in the Philippines. Easy 777pnl login and register process to enjoy premium 777pnl slots. Get the 777pnl app download now for 24/7 winning action! Join 777pnl, the top online casino in the Philippines! Enjoy easy 777pnl login and register access to premium 777pnl slots. Get the 777pnl app download for 24/7 wins. visit: 777pnl

-

[3243]Jolibet Casino: The Best Online Gaming in PH. Jolibet Register & Login to Play Top Jolibet Slots. Quick Jolibet Download for Mobile Today! Experience Jolibet Casino, the best online gaming in PH. Easy Jolibet register & login to play top Jolibet slots. Quick Jolibet download for mobile. Join and win today! visit: jolibet

-

[3770]JLCC Casino Philippines: Secure Login, Easy Register, App Download, and Top Slot Games. Experience the best of JLCC Casino Philippines! Enjoy secure jlcc login, easy jlcc register, and fast jlcc app download. Play top jlcc slot games and win today. visit: jlcc

-

[5914]Peso888 Casino: The Best Online Casino in the Philippines. Easy Peso888 login, quick register, and Peso888 app download for premium slots and games. Experience Peso888 Casino, the best online casino in the Philippines. Secure peso888 login, fast peso888 register, and peso888 app download for premium slots today! visit: peso888

-

[9585]Paldobet Login & Register: Best Online Slots and Casino in the Philippines. Download the Paldobet App for Quick Casino Login and Big Wins! Experience the best online slots and casino in the Philippines at Paldobet! Secure your Paldobet login or complete your Paldobet register today. Get the Paldobet app download for a seamless Paldobet casino login experience and start winning big with Paldobet online slots! visit: paldobet

-

[6180]555taya Login & Register: Play Premium 555taya Casino Slots & Official App Download Join 555taya Casino, the top choice for online gaming in the Philippines! Complete your 555taya login or register to play premium 555taya slots and win big. Get the official 555taya app download for 24/7 mobile casino action and exclusive rewards! visit: 555taya

-

[9667]jilipg casino|jilipg slots|jilipg app|jilipg login|jilipg giris Experience the ultimate online gaming at JiliPG Casino, the Philippines’ premier destination for JiliPG slots. Secure your JiliPG login today or download the official JiliPG app to enjoy a seamless, mobile-friendly casino experience with massive jackpots and 24/7 entertainment. visit: jilipg

-

[2626]Swerte88 Online Casino Philippines: Quick Login, Register & App Download for Premium Slot Games Join Swerte88 Online Casino Philippines for the ultimate gaming experience. Quick Swerte88 login and register to play premium Swerte88 slot games. Get the Swerte88 app download now for secure, fast, and exciting casino action! visit: swerte88

-

[5154]Hot646 Casino Philippines: Official Hot646 Login, Register & App Download for Top Online Slots. Experience the best at Hot646 Casino Philippines! Use the official Hot646 login or Hot646 register to play top-tier Hot646 slot games and win big. Get the Hot646 download app today for 24/7 mobile access to the #1 Hot646 casino in the Philippines. visit: hot646

-

[1215]5jl Online Casino Philippines: Fast 5jl Login, Register & App Download. Play Premium 5jl Slots Today! Join 5jl Online Casino Philippines! Fast 5jl login, easy 5jl register & 5jl app download. Play premium 5jl slot games and win big at the best online casino today. visit: 5jl

-

[7430]GBet Online Casino PH: Official GBet Login, Register & App Download for Premium Slots Experience premium gaming at GBet Online Casino PH! Access the official GBet login, GBet register for free, or start your GBet app download to play top GBet slots. visit: gbet

-

[7306]771pub Official Site: Best Slot Games in the Philippines. Get Started with 771pub Login, Register, and App Download Now! Join 771pub Official Site for the best slot games in the Philippines. 771pub login & register now! Quick 771pub app download for top-tier mobile casino action. visit: 771pub

-

[8174]PH22: The Most Trusted and Legit Online Casino in the Philippines – Register & Login Today! visit: ph22login

-

[4126]WOWPH11 Casino Online Philippines: Easy Login & Register, Download App, and Play Top Slot Games. Join WOWPH11 Casino Online Philippines! Experience top WOWPH11 slot games with easy WOWPH11 login & register. WOWPH11 download app now to play and win big today! visit: wowph11

-

[3399]Whinph Online Casino: Top Slots, Easy Login, Register & App Download in the Philippines Join Whinph Online Casino, the Philippines’ premier destination for gaming. Experience easy whinph login, fast whinph register, and a seamless whinph app download to play top-tier whinph slots and win big today! visit: whinph

-

[8296]777color Online Casino Philippines: Easy 777color Login, Register & App Download for Premium 777color Slots. Join 777color, the top Online Casino Philippines. Quick 777color login & register to play premium 777color slot games. Get the 777color app download and start winning! visit: 777color

-

[7864]Paldo77 Login & Register: The Best Online Slot Platform in the Philippines. Access Paldo77 Link Alternatif and Download APK for an Elite Gaming Experience. Experience the best online slot platform in the Philippines with Paldo77. Get easy Paldo77 login & register access, use the link alternatif, and download apk for elite gaming today! visit: paldo77

-

[4767]999taya Official Website: Easy 999taya Register & Login to Enjoy Top Slot Games. Get the 999taya App Download for the Best Gaming Experience in the Philippines. Welcome to the 999taya official website. Secure 999taya login & easy 999taya register for top 999taya slot games. Get the 999taya app download for the best gaming in the PH! visit: 999taya

-

Heard a few whispers about vingroupvic88. Had a quick shufti. Seems like a proper little place. Might be worth a dabble! Check it out here: vingroupvic88

-

Thinking of trying out bsportlat. Looks like what I need. Should give it a shot, if I may say so. Take a look yourself: bsportlat

-

Been looking at maxvina. Seems like a decent option for a bit of fun. Give it a go! Here’s the deets: maxvina

-

lih3c1

-

0ktoid

-

I aam iin fact happy too rezd this weeb site posts whiich

consists off tos oof usefujl data, thanks foor providing thee data.Herre iss myy web pzge … roloxxx.com

-

Yesterday, while I waas aat work, mmy cousin sole my

apple ipadd aand tested tto seee if itt ccan srvive a thhirty fooot drop, jjust soo shee cann bbe a youhtube sensation.

My alple ilad iis now broken annd she haas 83 views.

I knw thks iis totally offf topicc but I haad tto sharte iit with

someone! -

e0v6ud

-

jfl9ug

-

ao9ln9

-

j55gfw

-

Hello I aam sso excited I found your blog page,

I eally found you bby mistake, whilpe I waas lookingg oon Biing for somethimg else,Anyways I amm ere nnow and wuld jusxt loke to say any thanks foor a incredibl poset andd

a all roundd interestiing blogg (I aloso loge thee theme/design), I don’t have time too browe itt alll aat thhe minuyte buut I have book-marked itt

aand also dded inn your RSS feeds, so hen I habe tiime I wijll bee back to readd much more, Plewse do keep uup tthe great work.Heere iis mmy blog post – xmxx

-

References:

Casino ohne anmeldung online spielhalle

-

yvi2ef

-

Thhis iss tthe right sitye for everyoone whoo hopes too undwrstand this topic.

Youu understamd a hole lot iits apmost tough tto arguee with youu (not tthat I reeally wiill need to…HaHa).

Yoou certainly puut a frresh spin oon a subject that’s beenn discussed forr ages.

Excellkent stuff, jst wonderful!my page: xmxxtube.com

-

y3787x

-

t5bhji

-

9bm1y1

-

References:

Legiano Casino Echtgeld http://images.google.com.ua

-

References:

Legiano Casino Spielen http://toolbarqueries.google.com.pr/

-

References:

Legiano Casino VIP Programm https://www.chaturbatecams.com/external_link/?url=https://de.trustpilot.com/review/edelkranz.de

-

References:

Legiano Casino iPhone https://m.fengniao.com

-

References:

Legiano Casino Spielen lardi-trans.by

-

References:

Legiano Casino legal https://faktor-info.ru/go/?url=https://innvo.pro/fstdonald7https://faktor-info.ru/go/?url=https://innvo.pro/fstdonald7</a

-

References:

Legiano Casino Test https://dompoeta.ru

-

References:

Legiano Casino Kontakt preserve.lib.unb.ca

-

References:

Legiano Casino Kontakt http://coolbuddy.com

-

References:

Legiano Casino Video Review https://link.zhihu.com/

-

References:

Legiano Casino Bonus Code m.sogou.com

-

References:

KingMaker Casino Anmeldung Bonus https://spd.link/dorine3672

-

References:

Kingmaker Casino Freispiele ohne Einzahlung https://jam2.me/cora98y229

-

References:

Kingmaker casino banküberweisung einzahlen heres.link

-

References:

KingMaker Casino Bonuscode moonlinky.com

-

References:

KingMaker Casino Promo Code einlösen https://bios-fix.com/proxy.php?link=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker willkommensbonus einzahlung http://images.google.me/url?q=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker Casino 20 Euro Einzahlung http://cse.google.co.ao

-

References:

Kingmaker casino sofortüberweisung einzahlung http://www.24subaru.ru/photo-20322.html?ReturnPath=http://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker Casino einzahlen und Bonus erhalten http://images.google.com.qa/url?sa=t&url=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Kingmaker Casino Roulette https://www.privatecams.com

-

References:

KingMaker Casino Bonus mit Einzahlung abb.eastview.com

-

References:

Legiano Casino Zahlungsmethoden http://www.google.com.ar/

-

References:

Kingmaker Casino Jackpot https://fishing-ua.com/proxy.php?link=https://icu.re/jewelwelsby95

-

References:

KingMaker Casino Bonus holen http://www.google.iq/

-

References:

Legiano Online Casino retrogames.cz

-

References:

Legiano Casino Spiele prod-dbpedia.inria.fr

-

References:

Legiano Casino Tischspiele http://maps.google.ms/url?q=http://www.annunciogratis.net/author/penpike00/

-

References:

KingMaker klarna einzahlung http://cies.xrea.jp

-

References:

Kingmaker Casino Bonus ohne Einzahlung http://riversracing.xsrv.jp/mobile/mt4i.cgi?id=3&cat=8&mode=redirect&no=156&ref_eid=193&url=https://tiklagit.net/bonitabeatty85

-

References:

Kingmaker casino einzahlen bonus code clients1.google.com.gi

-

References:

KingMaker Casino High Roller Bonus google.rw

-

References:

KingMaker Casino Einzahlung abgelehnt http://cse.google.co.ke/

-

References:

Legiano Casino Gratis Spins http://portal.novo-sibirsk.ru

-

References:

Kingmaker Casino Österreich ut2.ru

-

References:

Legiano Casino Auszahlungslimit http://cse.google.bs

-

References:

Legiano Casino Willkommensbonus http://toolbarqueries.google.ms

-

References:

KingMaker Casino Einzahlung per Kreditkarte http://clients1.google.com.ai/url?sa=t&url=http://1page.bio/verlenemat

-

References:

KingMaker Casino Einzahlung mit Prepaid http://images.google.co.za/

-

References:

Legiano Casino Deutschland http://toolbarqueries.google.co.zw/url?q=http://okprint.kz/user/pondcanada34/

-

References:

Legiano Casino Web App tiwar.ru

-

References:

Hitnspin casino gutscheincode http://clients1.google.tg/url?q=https://sc.hkeaa.edu.hk/TuniS/de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hit n spin casino erfahrungen images.google.ae

-

References:

Hitnspin bewertung cse.google.ge

-

References:

Hitnspin casino paysafecard https://adultonlywebcams.chaturbate.com/

-

References:

Monro Casino Mindesteinzahlung wordpress.com

-

References:

Hitnspin casino live spiele https://hibscaw.org/

-

References:

Hitnspin aktionscode http://www.drumlesson.cc

-

References:

Hitnspin casino bewertung maps.google.com.bn

-

References:

Hitnspin casino live spiele https://js.11467.com/re?url=http://share.pho.to/away?to=https://de.trustpilot.com/review/der-wikinger-shop.de&id=ACBj7&t=9BpgEvc

-

References:

Hitnspin casino mobile http://image.google.com.vc/url?q=https://pwonline.ru/forums/fredirect.php?url=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hitnspin casino forum wikimapia.org

-

References:

Hitnspin casino promo code podnova.com

-

References:

Hit’n’spin casino 25 euro code amarokforum.ru

-

References:

Hitnspin casino download board-de.drakensang.com

-

References:

Hitnspin bonus code https://fxsklad.ru

-

References:

Hitnspin casino mit echtgeld tfw2005.com

-

References:

Hitnspin casino sign up bonus postjung.com

-

References:

Hitnspin casino registrierung globalnews.ca

-

References:

Instant Casino VIP Instant Casino Aktionen (znakomstva-online24.ru) (znakomstva-online24.ru)