How to Get a Debt Lawsuit Dismissed

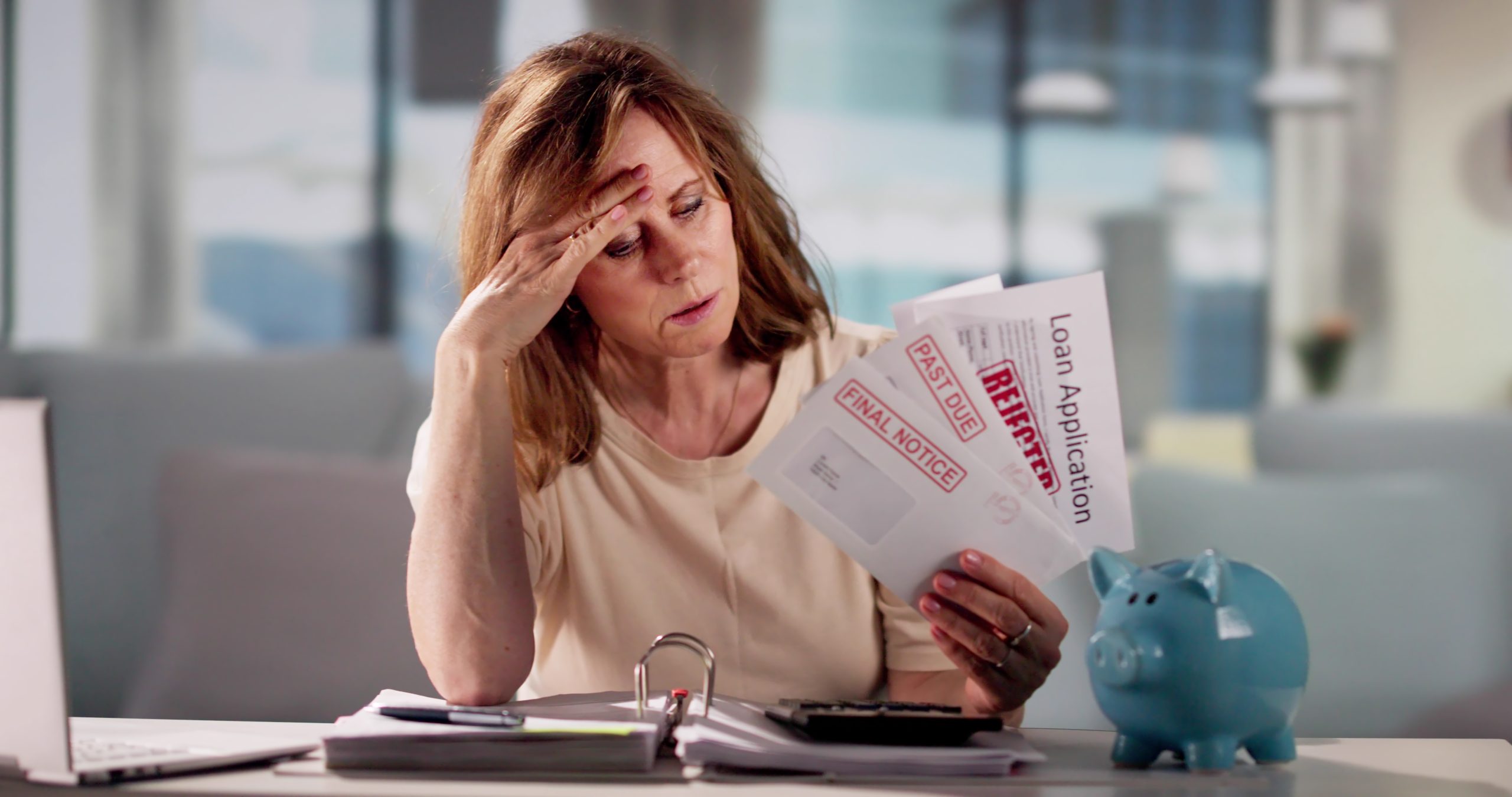

Receiving a summons for a debt collection lawsuit can be an intimidating experience. The prospect of court dates, legal fees, and a potential judgment can create significant stress.

However, it is crucial to understand that you have rights and a legal pathway to defend yourself. Ignoring the lawsuit is the worst course of action, as it will likely lead to a default judgment against you.

This guide provides a clear, step-by-step explanation of how to get a debt lawsuit dismissed. By taking informed, proactive measures, you can protect your assets and work toward a resolution.

Key Takeaways

- Never ignore a lawsuit summons; always file a formal response with the court to avoid a default judgment.

- You have the right to demand the creditor or collector validate the debt, which can be a powerful defense if they cannot provide sufficient proof.

- If the debt is older than your state’s statute of limitations for collection, you may have grounds for dismissal.

- Legal procedural errors, such as improper service, can be used to challenge the lawsuit’s validity.

- Even if dismissal is not possible, negotiating a settlement is often a viable path to resolve the case.

What Is a Debt Lawsuit?

A debt lawsuit is a legal action initiated by a creditor or a debt collector to recover money they allege you owe. This typically occurs after a period of missed payments and unsuccessful attempts to collect the debt through calls and letters.

Creditors file lawsuits to obtain a court judgment, which grants them enhanced legal powers to collect, such as wage garnishment, bank account levies, or placing a lien on your property.

The legal foundation for these lawsuits is often a claim of breach of contract, arguing that you failed to uphold the terms of a credit agreement. The process formally begins when the creditor files a complaint with the court, and you are served with a summons and a copy of that complaint.

Five Steps to Get a Debt Lawsuit Dismissed

Successfully defending against a debt lawsuit requires a methodical approach. The following steps outline a common defense strategy.

Step 1: Respond to the Lawsuit

The single most critical step is to respond to the lawsuit before your state’s deadline, which is often 20 to 30 days after you were served. This response, often called an “Answer,” is a formal legal document filed with the court. In it, you respond to each allegation in the creditor’s complaint, admitting, denying, or stating you lack sufficient knowledge to admit or deny.

By filing an Answer, you prevent the creditor from obtaining a default judgment, which they can get automatically if you fail to respond. A default judgment gives them the legal authority to pursue aggressive collection actions.

Step 2: Verify the Debt and Request Validation

Once you have responded, your next move is to challenge the plaintiff, the company suing you, to prove its case. The burden of proof is on them. You can do this by sending a debt validation request, a right granted under the Fair Debt Collection Practices Act (FDCPA). This is especially potent if the plaintiff is a debt collector who purchased the debt from the original creditor.

Request that they produce documentation proving:

- You are indeed the responsible party.

- The original credit agreement.

- A complete and accurate accounting of the debt, including the original amount and all fees and interest charged.

- A chain of title proving they have the legal right to collect the debt.

If the plaintiff cannot produce this documentation, your grounds for dismissal strengthen significantly.

Step 3: Check the Statute of Limitations

Every state has a law called a “statute of limitations” that sets a time limit on how long a creditor has to file a lawsuit to collect a debt. This period typically ranges from three to six years, varying by state and the type of debt. The clock usually starts from the date of your last payment or the date the account first became delinquent.

If the statute of limitations has expired, the debt is considered “time-barred.” You can raise this as an affirmative defense in your Answer and file a motion to dismiss the case. It is important to note that making a partial payment or even acknowledging the debt in some states can restart the statute of limitations clock.

Step 4: File a Motion to Dismiss

If you identify a legal deficiency in the lawsuit, you can file a formal “Motion to Dismiss” with the court. This motion asks the judge to throw out the case for specific legal reasons. Common grounds for a motion to dismiss include:

- Lack of Proof: The plaintiff failed to state a valid legal claim or provide evidence with their initial complaint.

- Improper Service: You were not served the lawsuit papers correctly according to your state’s laws.

- Expired Statute of Limitations: As discussed above.

- Incorrect Plaintiff: The entity suing you cannot prove it owns the debt.

Filing this motion requires a good understanding of court procedure and is an area where consulting with an attorney can be highly beneficial.

Step 5: Negotiate a Settlement

Even if you have a strong defense, litigation can be unpredictable and time-consuming. Negotiating a settlement is often a pragmatic alternative. In a settlement, you agree to pay a portion of the debt, often a lump sum that is less than the full balance, in exchange for the creditor dismissing the lawsuit and considering the debt resolved.

Many creditors are open to settlement because it guarantees them some recovery without the expense and delay of a trial. All settlement terms must be obtained in writing before you send any payment.

What Happens if You Lose a Debt Lawsuit?

If the court rules in favor of the creditor, they will receive a monetary judgment against you. This judgment is a public record and can severely damage your credit score. More concretely, it grants the creditor the legal authority to use enforcement mechanisms to collect the money, which may include:

- Wage Garnishment: A court order directing your employer to withhold a portion of your paycheck and send it to the creditor.

- Bank Levy: The freezing and seizure of funds from your checking or savings account.

- Property Lien: A claim placed on your real estate, which must be paid when you sell or refinance the property.

While this is a serious outcome, it does not mean you are entirely out of options. You may still be able to negotiate a payment plan with the creditor post-judgment or explore debt relief options like debt resolution or, in extreme cases, bankruptcy.

Chances of Winning a Debt Lawsuit

The likelihood of a successful defense in a debt lawsuit varies based on the specific circumstances of the case. However, defendants often have a better chance than they might assume, particularly when they actively contest the lawsuit.

Key factors that influence the chances include:

- The Creditor’s Documentation: Many debt buyers sue with limited or flawed records. If they cannot validate the debt, their case may fail.

- Procedural Defenses: Mistakes in how the lawsuit was filed or served can lead to dismissal.

- The Age of the Debt: An expired statute of limitations is a complete defense.

- Your Response: Simply by responding and forcing the creditor to prove its case, you shift the dynamic. Many creditors rely on default judgments and may be less prepared for a vigorous defense.

Individuals who seek legal advice and meticulously follow the steps to challenge the lawsuit significantly improve their odds of a favorable outcome, whether that is an outright dismissal, a settlement for a fraction of the amount, or a manageable payment plan.

Preventing Future Debt Lawsuits

The best defense against a debt lawsuit is proactive financial management. If you are struggling with debt, taking early action can prevent the situation from escalating to litigation.

- Open Communication: If you anticipate missing a payment, contact your creditor proactively. They may offer a temporary hardship plan or modified payment terms.

- Create a Budget: A clear budget can help you prioritize essential expenses and identify areas where you can allocate funds to debt repayment.

- Understand Debt Relief Options: Familiarize yourself with solutions like debt management plans, debt resolution programs, debt consolidation loans, and, as a last resort, bankruptcy. Each option has different implications for your credit and finances.

- Seek Professional Advice: Consulting with a reputable credit counselor or a legal professional can provide you with a clear understanding of your rights and a structured path toward debt eradication.

Staying informed about your consumer rights and managing your finances with a clear plan are the most effective strategies for achieving long-term financial stability and avoiding future legal challenges.

Frequently Asked Questions

Can a credit card company sue you?

Yes, a credit card company can sue you to recover an unpaid debt. As the original creditor, they have a direct contractual relationship with you. If they win the lawsuit, they can obtain a judgment to use collection tools like wage garnishment, provided they follow state and federal laws.

Can debt collectors sue you?

Yes, third-party debt collectors and debt buyers can sue you. However, they must be able to prove they have the legal right to collect the debt. This often requires them to provide documentation tracing the debt from the original creditor to them. Challenging their proof of ownership is a common and often successful defense strategy.

What are the chances of winning a credit card lawsuit?

The chances depend heavily on the facts of the case and your response. If the creditor has solid documentation and you do not respond, their chances are near 100 percent. If you respond and challenge the lawsuit, particularly by demanding strict proof of the debt and checking for procedural errors, your chances of a positive result, such as dismissal or a favorable settlement, increase substantially.

How to dispute a debt and win?

To formally dispute a debt, you should send a written debt validation letter to the collector within 30 days of their first contact with you. If you are already in a lawsuit, you dispute the debt by filing an Answer with the court that denies the allegations. To “win,” you must force the collector to provide conclusive evidence. If they fail to do so, the court may dismiss the case.

What happens if a creditor wins a debt lawsuit?

If a creditor wins, the court issues a judgment against you. This judgment can lead to wage garnishment, bank account levies, or property liens. The judgment will also be reported to credit bureaus, damaging your credit score for years. After a loss, it is still possible to negotiate with the judgment holder to set up a payment plan or settle the judgment for a reduced amount.

147 Comments

-

888php: Best Online Casino & Slot Games in PH – Login, Register, & App Download Experience the best 888php online casino and top 888php slot games in the PH! Secure your 888php login, complete your 888php register, and get the 888php app download to start winning today. visit: 888php

-

[8294]PGAsia Online Casino: Easy Login, Register, and App Download for the Best Slots in the Philippines. Experience the best slots in the Philippines at PGAsia Online Casino. Enjoy a secure pgasia login, quick pgasia register, and easy pgasia app download for non-stop gaming action and big wins today! visit: pgasia

-

[8476]playph download|playph slots|playph casino|playph login|playph app Experience the ultimate online gaming at **playph casino**, the Philippines’ premier destination for top-rated **playph slots** and live games. Secure your **playph login**, get the official **playph download**, or install the **playph app** to enjoy seamless mobile play and win big anytime, anywhere! visit: playph

-

[5370]99boncasino: The Best Online Slots and GCash Casino in the Philippines visit: 99boncasino

-

[8012]22jl: Best Philippines Online Casino & Slot Games. Easy Login, Register & 22jl App Download. Experience the best Philippines online casino at 22jl! Enjoy premium 22jl slot games with a quick 22jl login and easy 22jl register process. Get the 22jl app download today for secure, top-tier casino entertainment on the go. Join now for exclusive rewards! visit: 22jl

-

[4276]LuckyPH Online Casino Philippines: Register & Login to Play Top LuckyPH Slots. Get the LuckyPH App Download for Premium Gaming and Big Wins! Join LuckyPH Online Casino Philippines! Access your LuckyPH login or LuckyPH register to play top LuckyPH slots. Get the LuckyPH app download for big wins today! visit: luckyph

-

[5403]Jilievo Online Casino: Best Jilievo Slot Games in PH. Jilievo Login, Easy Register, and Fast Jilievo App Download for 24/7 Winning Action. Experience the best Jilievo slot games at Jilievo Online Casino PH. Quick Jilievo login, easy Jilievo register, and fast Jilievo app download for 24/7 winning action! visit: jilievo

-

[2185]x777 Login & Register: Best Slot Online Casino in the Philippines. Official x777 Casino Link & Download APK Today! Join x777, the Philippines’ best slot online casino! Fast x777 login & register. Get the official x777 casino link & x777 download apk for big wins today! visit: x777

-

[410]JL16 Login & Register: Best Slot Games, Official Link & App Download Philippines Experience the best jl16 slot games in the Philippines! Use our jl16 official link for secure jl16 login and jl16 register. Get the jl16 app download now to enjoy premium casino gaming, exclusive bonuses, and big wins on the go! visit: jl16

-

[4057]jljl6 Online Casino Philippines: Easy Login, Register & App Download for the Best Slot Games Experience the ultimate jljl6 Online Casino Philippines! Enjoy fast jljl6 login, easy jljl6 register, and premium jljl6 slot games. Secure your jljl6 app download now for top-tier rewards and big wins. Play today! visit: jljl6

-

[444]Pwin Online Casino Philippines: Secure Pwin Login, Quick Register & App Download for the Best Pwin Slots. Experience the ultimate Pwin Online Casino Philippines! Secure Pwin login, fast Pwin register, and easy Pwin app download. Play the best Pwin slot games and win today. visit: pwin

-

[9390]jljl5 casino|jljl5 giris|jljl5 register|jljl5 login|jljl5 slots Experience the ultimate gaming at jljl5 casino, the Philippines’ premier platform for top-tier jljl5 slots. Complete your jljl5 register today or use the secure jljl5 login to access exclusive bonuses and high-stakes action. Use the official jljl5 giris link for safe and seamless access to the best online casino experience. visit: jljl5

-

[2629]xgbet PH: The Best Online Casino & Live Sports Betting with Fast GCash Payouts Experience top-tier gaming at xgbet online casino Philippines. Discover the best online slots xgbet and thrilling xgbet live sports betting. Secure your xgbet login PH today for seamless GCash online gambling Philippines with the fastest payouts in the country. visit: xgbet

-

[8199]PH9999 Online Casino Philippines: Login, Register, App Download & Top Slot Games Experience the ultimate PH9999 Online Casino Philippines! Secure ph9999 login, fast ph9999 register, and easy ph9999 app download. Play the best ph9999 slot games and win big today at the most trusted online casino in the PH. visit: ph9999

-

[1026]The Philippines’ premier online casino and sports betting destination with fast GCash payments. visit: philucky

-

[8902]Phlbest Official: Login, Register, and App Download for the Best Online Slots in the Philippines. Get the Phlbest Casino APK Today! Join Phlbest Official for the premier online slots experience in the Philippines! Access easy phlbest login, phlbest register, and phlbest app download options. Get the official phlbest casino apk today and start winning big! visit: phlbest

-

[9652]The Philippines’ Premier Destination for Legit Online Casino Games and Betting visit: nustar online

-

[9022]Slotsgo Philippines: Best Online Slots & Casino Games. Quick Slotsgo Login, Easy Register, and Mobile App Download for Big Wins! Experience the best slotsgo online slots and casino games in the Philippines! Quick slotsgo login, easy slotsgo register, and slotsgo app download for big wins. visit: slotsgo

-

[8206]PinasGems Online Casino: Secure Login, Easy Register & Top Slot Games. Download the App Now! Experience the ultimate gaming at PinasGems Online Casino. Enjoy secure PinasGems login, fast PinasGems register, and top PinasGems slot games. Download the PinasGems app now for the best mobile casino experience in the Philippines! visit: pinasgems

-

[9590]Taya77 Online Casino Philippines: Taya77 Login, Register, Slots & App Download Join Taya77 Online Casino Philippines for the ultimate gaming experience! Access your account via Taya77 login, complete your Taya77 register quickly, and explore premium Taya77 slot games. Get the Taya77 app download for seamless mobile play and start winning today at the most trusted online casino in the Philippines. visit: taya77

-

[8955]774pub Online Casino: Best 774pub Slot Games in the Philippines. Fast 774pub Login, Register, and Official 774pub App Download. Experience the best 774pub online casino in the Philippines. Fast 774pub login, 774pub register, and official 774pub app download for top 774pub slot games. visit: 774pub

-

[2403]GBet Online Casino PH: Official GBet Login, Register & App Download for Premium Slots Experience premium gaming at GBet Online Casino PH! Access the official GBet login, GBet register for free, or start your GBet app download to play top GBet slots. visit: gbet

-

[3954]Jiliaa Online Casino Philippines: Quick Jiliaa Login, Register & App Download for Top Slot Games. Experience the best of Jiliaa Online Casino Philippines! Enjoy quick jiliaa login, easy jiliaa register, and seamless jiliaa app download for top-tier jiliaa slot games. Join today for a premium gaming experience and start winning big! visit: jiliaa

-

[9320]Casino Official Site Philippines: Easy Login, Register & Download App for the Best Slots Online. Welcome to the Casino Official Site Philippines! Complete your casino register for an easy casino login. Casino download app now to play the best casino slots online today. visit: casino

-

[4254]Pin77 Philippines: Official Login, Register & App Download. Experience Top Pin77 Slot Games and Secure Link Alternatif. Join Pin77 Philippines for the official pin77 login and pin77 register. Play premium pin77 slot games, get the pin77 download app, and access secure pin77 link alternatif today. visit: pin77

-

[9488]8k8 Official Link: Easy Login & Register for Top Casino Slots. Download the 8k8 App Today for the Ultimate Philippines Gaming Experience! Experience the ultimate Philippines gaming with 8k8! Use the 8k8 official link for fast 8k8 login and 8k8 register. Play top 8k8 casino slots and get the 8k8 app download today for the best mobile betting experience and big rewards. visit: 8k8

-

[5024]Lucky88 Philippines: Official Link for Slot Online, Easy Login, Register & App Download. Access the Lucky88 official link in the Philippines. Experience top lucky88 slot online games. Fast lucky88 login, easy register, and lucky88 app download now! visit: lucky88

-

[2859]MNL168: Best Philippines Online Casino – Secure Login, Register, App Download & Slot Online Link Experience MNL168, the best Philippines online casino! Access secure mnl168 login, quick mnl168 register, and premium mnl168 slot online games. Get the official mnl168 app download and mnl168 casino link to start winning today! visit: mnl168

-

[4629]Jili123 Online Casino Philippines: Official Login, Register, & Slot Games. Download the App Today! Join Jili123 Online Casino Philippines for the best jili123 slot games. Secure jili123 login, quick jili123 register, and easy jili123 app download. Play and win big today! visit: jili123

-

[1540]Dailyjili Casino Philippines: Best Online Slots, Quick Dailyjili Login & Register. Get the Dailyjili App Download for Premium Gaming Action. Join Dailyjili Casino Philippines! Experience fast dailyjili login & register for top dailyjili slot games. Get the dailyjili app download for premium gaming at dailyjili casino today. visit: dailyjili

-

[6158]Maxgaming Philippines: Experience the best online casino Philippines with secure login and fast GCash payouts. Experience the ultimate thrill at Maxgaming Philippines, the best online casino Philippines. Access a secure Maxgaming login to explore top-tier Philippines online gambling options and enjoy lightning-fast GCash casino Philippines payouts. Join today for a safe, reliable, and premium gaming experience tailored for Filipino players. visit: maxgaming

-

[253]jl333 Online Casino Philippines: Best Slots, Easy Login, Register & App Download Join JL333 Online Casino Philippines for the best JL333 slot games. Quick JL333 login, easy JL333 register, and secure JL333 download for mobile play. Sign up today! visit: jl333

-

[2446]PHWIN51: Best Online Casino & Slots in the Philippines. Easy Login, Register, and App Download for Premium Gaming. Experience the best online casino and slots at PHWIN51 Philippines. Enjoy seamless phwin51 login, fast phwin51 register, and the phwin51 app download for premium gaming. Play top phwin51 slot games and win big today! visit: phwin51

-

[3478]The Best Legit Online Casino in the Philippines – Experience Secure Gaming and Fast Logins with JL10 Casino. visit: jl10 casino

-

[6178]SpinBit Philippines: Easy Login & Register for Top Casino Slots, Sign Up Bonus & App Download Join SpinBit Philippines today! Experience easy SpinBit login & register to play the best SpinBit casino slots. Claim your exclusive SpinBit sign up bonus and try our SpinBit app download for top-tier mobile gaming. visit: SpinBit

-

[5588]77ph Login & Register: Best Philippines Casino Online Slots & App Download Experience the best Philippines casino online at 77ph! Secure your 77ph login & 77ph register to play premium 77ph slots. Get the 77ph app download for 24/7 gaming and big wins today! visit: 77ph

-

[5403]jljl3 casino|jljl3 register|jljl3 giris|jljl3 slots|jljl3 login Experience the ultimate gaming at jljl3 casino, the premier online gambling platform in the Philippines. Enjoy easy jljl3 login and jljl3 register access to top-rated jljl3 slots and exclusive rewards. Sign up today at jljl3 giris for a world-class casino experience! visit: jljl3

-

[23]co777 Online Casino Philippines: Login, Register & Play Top Slots – Download the App Today! Experience the best at co777 Online Casino Philippines! Secure your co777 login, register today, and play top co777 slot games. Download the co777 app for big wins! visit: co777

-

[47]jljl991 Online Casino Philippines: Easy jljl991 login, register, and app download for the best jljl991 slots and rewards. Experience jljl991 Online Casino Philippines. Enjoy easy jljl991 login, jljl991 register, and jljl991 app download. Play the best jljl991 slot games and win big rewards today! visit: jljl991

-

[684]PHPlus Online Casino: Top Slot Games in the Philippines. Login, Register, and Download the App to Win Big. Experience the best phplus slot games at PHPlus Online Casino Philippines! Phplus login, phplus register, or phplus download app today for your chance to win big. visit: phplus

-

[176]phmaya casino|phmaya app|phmaya download|phmaya slots|phmaya login Experience world-class gaming at phmaya casino, the premier online destination in the Philippines. Secure your phmaya login to access a massive variety of phmaya slots and exclusive rewards. For gaming on the go, complete your phmaya download and get the official phmaya app today for a seamless, mobile-optimized casino experience. visit: phmaya

-

[4910]377jl Casino: Login, Register & App Download for Top Philippines Slot Games. Join 377jl Casino for the best Philippines slot games! Easy 377jl login, quick 377jl register, and 377jl app download for mobile play. Win big at 377jl slot now! visit: 377jl

-

[4658]SuperPH Online Casino: Your Top Destination for Slots in the Philippines. Login, Register, or Get the SuperPH App Download to Play and Win Today! **Meta Title:** SuperPH Online Casino: Best Slots in the Philippines | Login & Register

**Meta Description:** Welcome to SuperPH Online Casino, the Philippines’ top spot for SuperPH slots. Quick SuperPH login or register to start. Get the SuperPH app download and win big today! visit: superph

-

[7551]Aaajili Casino Philippines: Official Aaajili Login, Register & App Download for Top Online Slots. Join Aaajili Casino Philippines for top aaajili slots! Fast aaajili login, easy aaajili register, and official aaajili app download. Experience the best aaajili casino games and win big today! visit: aaajili

-

[8935]99jili Online Casino Philippines: Your Hub for 99jili Login, Register, App Download, and the Best Slot Games Experience 99jili Online Casino Philippines! Quick 99jili login and register to play the best 99jili slot games. Get the 99jili app download and start winning today! visit: 99jili

-

[3934]JL77 Online Casino Philippines: Official Login, Register & App Download for Best Slot Games Join JL77 Online Casino Philippines for the ultimate gaming experience! Access the official jl77 login, quick jl77 register, and jl77 app download to enjoy premium jl77 slot games and exclusive bonuses today. visit: jl77

-

[7854]ubet95 Official Link: Fast ubet95 Login & Register. Download the ubet95 App to play the best ubet95 slot games in the Philippines. Visit the ubet95 official link for fast ubet95 login & register. Start your ubet95 app download to play the best ubet95 slot games in the Philippines. Sign up now! visit: ubet95

-

[1836]JLLJPH Online Casino Philippines: Login & Register to Play JLLJPH Slot Games. Download the JLLJPH App for the Ultimate Casino Experience. Experience the best of JLLJPH Online Casino Philippines! Use your jlljph login or complete a quick jlljph register to play premium jlljph slot games. Get the jlljph app download for the ultimate mobile gaming experience. Join the #1 jlljph online casino and start winning today! visit: jlljph

-

[5176]z8slot Official Site Philippines: Easy z8slot Login, Register, and App Download for Premium Online Slots. Join z8slot official site for the best z8slot online slot experience in the Philippines. Benefit from easy z8slot login, fast z8slot register, and a seamless z8slot app download for premium gaming on the go. visit: z8slot

-

[8381]777ace slots|777ace casino|777ace register|777ace giris|777ace login Experience the ultimate gaming thrill at 777ace Casino, the premier destination for online slots in the Philippines. Complete your 777ace register today to unlock exclusive bonuses. Enjoy seamless 777ace login and 777ace giris access to a world of premium 777ace slots and live casino action. Join now and win big! visit: 777ace

-

[1816]kkkjili Casino Philippines: Your Premier Destination for kkkjili Slot Games. Quick kkkjili Register, Easy kkkjili Login, and Fast kkkjili Download for the Ultimate Gaming Experience! Experience kkkjili Casino Philippines! Quick kkkjili register & easy kkkjili login for top kkkjili slot games. Fast kkkjili download for the ultimate gaming experience. Join now! visit: kkkjili

-

[9718]Peraplay: Best Online Casino in the Philippines. Easy Login, Register & App Download for Premium Slot Games. Join Peraplay, the Philippines’ best online casino! Enjoy easy peraplay login, register, and peraplay app download. Play premium peraplay slot games and win big at the top peraplay casino online today. visit: peraplay

-

[9060]881jili app|881jili slots|881jili download|881jili login|881jili register Experience the ultimate online gaming at 881jili, the Philippines’ leading casino platform. Play exciting 881jili slots, complete your 881jili register today, and enjoy seamless 881jili login access. Secure your 881jili download for the official 881jili app and start winning big anytime, anywhere! visit: 881jili

-

[5632]Official FG777 Link: The Best GCash Online Casino and Slot Games in the Philippines. visit: fg777link

-

[6536]jljl88 slots|jljl88 casino|jljl88 giris|jljl88 register|jljl88 login Experience the ultimate gaming at jljl88 casino, the Philippines’ top destination for online players. Explore a massive variety of jljl88 slots, enjoy a seamless jljl88 login, and fast jljl88 register access. Join jljl88 giris today for exclusive bonuses and big wins! visit: jljl88

-

[9878]Haha777 Philippines: Top Online Casino & Slot Games. Quick Haha777 Login, Register, and App Download for the Best Gaming Experience. Experience Haha777 Philippines: the top online casino for Haha777 slot games. Easy Haha777 login & register. Get the Haha777 app download for the best gaming experience! visit: haha777

-

[726]Jilicc Online Casino Philippines: Premium Jilicc Slot Games, Easy Jilicc Login & Register. Get the Official Jilicc App Download Today! Experience Jilicc Online Casino Philippines! Enjoy premium Jilicc slot games with a seamless Jilicc login and register process. Get the official Jilicc app download today for the ultimate gaming experience and big wins! visit: jilicc

-

[5843]747bet Philippines: Secure Login, Fast Register & Official App Download for Top Online Slots and Casino Games. Join 747bet Philippines for the best gaming! Access our official 747bet casino link for a secure 747bet login & fast 747bet register. Play top 747bet online slots and get the 747bet app download for mobile play. visit: 747bet

-

[5869]Jili55 Online Casino Philippines: Easy Login, Fast Register & Best Jili55 Slot Games | Download the Jili55 App Today Experience Jili55 Online Casino Philippines! Enjoy easy jili55 login, fast jili55 register, and the best jili55 slot games. Get the jili55 app download and start winning today! visit: jili55

-

[3620]ManaloPlay Casino Philippines: Best Online Slots & Live Games. Quick ManaloPlay Login, Register, and App Download to Start Winning Today! Experience ManaloPlay Casino Philippines! Quick ManaloPlay login, register now, and download the app for top online slots and live games. Win big at ManaloPlay casino today! visit: manaloplay

-

[8009]Jili30: The Philippines’ Best Online Casino for Premium Jili Slot Games visit: jili30

-

[266]AmunRa Official Site: Experience AmunRa Slot Online, Easy AmunRa Casino Login, & AmunRa App Download. Register Now for the Best Gaming in the Philippines! Visit the AmunRa Official Site for the ultimate AmunRa Slot Online experience. Enjoy easy AmunRa Casino Login and fast AmunRa App Download. AmunRa Register Now for the best online casino gaming in the Philippines! visit: AmunRa

-

[9820]PHClub Online Casino: Best Slots, Easy Login, Register & App Download Join PHClub Online Casino for the best PHClub slots in the Philippines. Enjoy fast PHClub login, easy PHClub register, and a quick PHClub app download. Start winning today! visit: phclub

-

[7179]TG7771 Casino Philippines: Top Online Slot Games. Easy TG7771 Login, Register, and App Download. Experience the best online gaming at TG7771 Casino Philippines! Enjoy top tg7771 slot games. Easy tg7771 login, register, and tg7771 download for mobile. Join the premier TG7771 casino for big wins today! visit: tg7771

-

[6094]41jili Online Casino: Official Login, Register, & App Download for Best Philippines Slots Experience the best of 41jili Online Casino! Secure your 41jili login, complete your 41jili register, and play top Philippines 41jili slot games. Get the 41jili app download today for the ultimate mobile gaming experience and big wins. visit: 41jili

-

[3991]AG777: The Best Online Casino in the Philippines for Legit GCash Gambling and Fast Payouts. Experience AG777, the best online casino in the Philippines for legit online gambling. Secure your ag777 login today for fast GCash casino Philippines payouts and top-tier games! visit: ag777

-

[5110]The Best Online Casino in the Philippines with Secure GCash Payments and Easy Okebet3 Login visit: okebet3

-

[9877]JL888 Login, Register & App Download | Official Link for Best Slot Online Philippines Join JL888, the #1 slot online platform in the Philippines! 🎰 Use the official link for a fast JL888 login or register now to start winning. Get the JL888 app download for the ultimate mobile casino experience today! visit: jl888

-

Looking for a Betão Betano signup guide. It seemed pretty straightforward but I want to be completely sure before signing up! Click here to investigate: betão betano

-

Anyone else having trouble with the f12betlogin? Keeps saying wrong password even though I’m sure it’s correct. Is this normal? Click through here: f12betlogin

-

79mbet? Yeah, I’ve played there a few times. The site’s alright, nothing too flashy, but the games are fun, and you can usually find a bonus code floating around. See for yourself at 79mbet.

-

8nk7si

-

r56837

-

6h78kv

-

References:

F1 Casino Auszahlung Foxwoods Resort Casino

-

References:

Wind creek casino atmore al smallbusinessinternships.com

-

zm13r1

-

References:

Legiano Casino Slots http://pinktower.com/?https://blog.fc2.com/?jump=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Legiano Casino Codes images.google.com.sg

-

References:

Online casino mobile https://hdmekani.com/proxy.php?link=https://www.paltalk.com/linkcheck?url=https://de.trustpilot.com/review/owowear.de

-

References:

Legiano Casino Verifizierung https://42.pexeburay.com/

-

References:

Legiano Casino Kundenservice https://cocoleech.com

-

References:

Legiano Casino Bonus ohne Einzahlung https://link.17173.com/?target=http://board-en.darkorbit.com:443/proxy.php?link=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

Legiano Casino Paysafecard optimize.viglink.com

-

References:

Legiano Casino 2026 http://rusnor.org

-

References:

Legiano Casino Android https://www.bigsoccer.com/proxy.php?link=https://de.trustpilot.com/review/edelkranz.de

-

References:

Legiano Casino Echtgeld https://embed.gosugamers.net

-

References:

Legiano Casino sicher http://clients1.google.mk

-

References:

Legiano Casino Sicherheit http://www.dftgroupsvn.uniroma2.it/

-

References:

Ligiano Casino wiki.holzheizer-forum.de

-

References:

Legiano Casino Download http://shop1.kokacharm.cafe24.com

-

References:

Legiano Casino Auszahlungsdauer http://coolbuddy.com/newlinks/header.asp?add=http://1.school2100.com/bitrix/rk.php?goto=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Legiano Casino Cashback http://www.aozhuanyun.com

-

References:

Legiano Casino Jackpot http://image.google.tk

-

References:

Legiano Online Casino kirov-portal.ru

-

References:

Legiano Casino Kontakt https://discuss.7msport.com/wap/en/reply.aspx?no=347024&pid=934632&url=https://jagoan-hosting.online/lisalecouteur

-

References:

Legiano Casino Registrierung image.google.com.om

-

References:

KingMaker Casino Einzahlungsbonus 200% https://bion.ly/sterlingisbell

-

References:

KingMaker einzahlungslimits https://watchnow.site/brandenmoreau

-

References:

KingMaker skrill einzahlung https://heres.link/eliasshute9018

-

References:

KingMaker Casino Anmeldebonus upangmarga.go.id

-

References:

KingMaker Casino Einzahlungsbonus ohne Umsatzbedingungen pwonline.ru

-

References:

KingMaker Casino Einzahlung per Giropay https://livesexcamgirls.chaturbate.com/

-

References:

Kingmaker Casino Roulette http://riversracing.xsrv.jp/mobile/mt4i.cgi?id=3&cat=8&mode=redirect&no=156&ref_eid=193&url=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker Casino Einzahlung mit Klarna shop2.myflowert.cafe24.com

-

References:

KingMaker willkommensbonus einzahlung http://clients1.google.si/url?q=https://de.trustpilot.com/review/beyondjewellery.de

-

References:

KingMaker einzahlung apple pay http://medical-dictionary.thefreedictionary.com/_/cite.aspx?url=http://unim.ma/alvaroa8427707&word=Cipro&sources=MGH_Drugs,davisDrug,hm_med

-

References:

KingMaker Casino Bonuscode Einzahlung http://shell.cnfol.com

-

References:

Legiano Casino Login clients1.google.iq

-

References:

KingMaker zahlungsmethoden omnimed.ru

-

References:

Legiano Casino Jackpot https://www.camslaid.com/external_link/?url=https://telegra.ph/100–bis-zu-500–200-Freispiele-06-07

-

References:

KingMaker Casino Einzahlung per Kreditkarte google.com.bo

-

References:

KingMaker Casino Einzahlung per Klarna https://utmagazine.ru

-

References:

Legiano Casino Umsatzbedingungen http://maps.google.com.qa/url?q=https://karayaz.ru/user/advicethread33/

-

References:

Kingmaker casino banküberweisung einzahlen images.google.com.sg

-

References:

Legiano Casino Gratis Spins http://clients1.google.gm/

-

References:

Kingmaker casino einzahlung sofort verfügbar http://toolbarqueries.google.bt/url?q=https://m.2target.net/melvinairv

-

References:

Kingmaker casino paysafecard einzahlung https://wiki.kubg.edu.ua/

-

References:

Legiano Casino Bonusbedingungen images.google.li

-

References:

Legiano Casino App images.google.ge

-

References:

Legiano Casino Download clients1.google.co.uz

-

References:

Hit n spin casino deutsch google.no

-

References:

Monro Casino Mobile http://remit.scripts.mit.edu/

-

References:

Hitnspin casino gutscheincode hotubi.com

-

References:

Hit n spin http://bgbmoto.ca/

-

References:

Monro Casino Einzahlung http://coolbuddy.com/newlinks/header.asp?add=https://sosi.al/vadawimble2506

-

References:

Hitnspin casino seriös https://www.emlakkulisi.com/

-

References:

-

References:

Hitnspin casino forum douban.com

-

References:

Hit’n’spin casino 25 euro code http://images.google.as/url?q=https://old-site.bsau.ru/bitrix/rk.php?goto=https://de.trustpilot.com/review/der-wikinger-shop.de

-

References:

Hitnspin casino login https://link.17173.com/?target=https://80aaaokoti9eh.рф/user/fatfarmer65/

-

References:

Hitnspin casino registrierung comic-rocket.com

-

References:

Hitnspin casino spielautomaten https://www.paltalk.com

-

References:

Hit n spin freispiele https://r.pokupki21.ru/redir.php?https://flashjournal.site/item/hitnspin-casino-bonus-2026-erfahrungen-und-test

-

References:

Hitnspin casino spiele http://tiwar.net/?channelId=946&extra=520&partnerUrl=urlscan.io/result/019eb130-8ced-70ae-9076-74f45cae9467/

-

References:

Hitn spin casino http://www.allods.net/redirect/1page.bio/latashiafo

-

References:

Hitnspin casino ohne anmeldung almanach.pte.hu

-

References:

Lollybet Casino Willkommensbonus http://www.google.com.nf/url?q=https://utmagazine.ru/r?url=https://lollybet.com.de/

-

References:

Lollybet Bonus ohne Einzahlung http://www.garagebiz.ru

-

References:

Lollybet Casino Auszahlungsdauer http://clients1.google.st/

-

References:

Lollybet Free Spins images.google.com.bz

-

References:

Good game sites worldaid.eu.org

-

References:

Tropicana online casino https://carrieresecurite.fr